The Weekender

My weekly perspective on global market developments and their potential broader implications

Gary Paulin

Head of International Enterprise Client Solutions

AUGUST 26, 2023

Fighting in the gaps, still

With reference to a previous edition of The Weekender: 'Fighting in the Gaps', I’ll offer little value opining on the investment merits of Nvidia. If you wanted to pick holes, you might argue Chinese demand, a surprise, may have been brought forward to avoid potential future export restrictions. Yet until the masses work out there are limits in both use and value of generative AI the excitement will likely continue. That is, unless, price gets in the way. As Scott Galloway is fond of saying, few things are ever as good (or as bad) as they seem; “this too shall pass”. That’s markets. That’s mean reversion. Scarcity premiums apply until supply catches up, demand falters, or both. That and even great businesses can be made bad investments, by price. It’s interesting to see the sell-offs in supply chain stocks like ASML (-6% reversal), Tokyo Electron (-5%), Advantest (-10%). Perhaps the promise of future AI cashflows are being eroded as the 10Y reprices ‘no-landing’, full employment and large fiscal deficits under the auspices of ‘National Security’, or old money ‘Military Keynesianism’. Whatever the outcome, we still suspect de-risking continues out of long-duration (debt and Tech) into shorter duration (value), offshore (Japan, UK, Brazil) and more scarce assets in the material world, especially those geared into the Fiscal Put of state largesse. For clues, see US Steel.

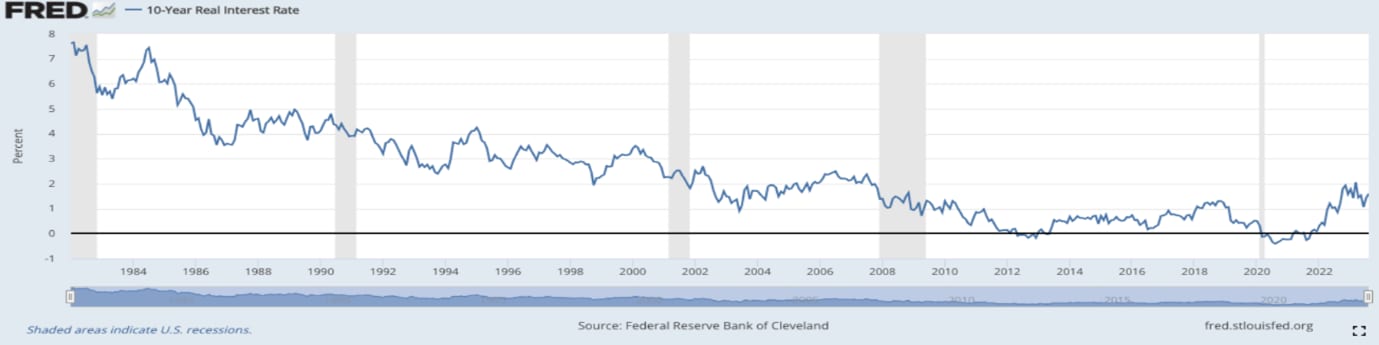

Real interest rates

Real interest rates—nominal rates minus the rate of inflation— may finally be normalising to levels above the near-zero that has prevailed since the financial crisis. As the chart below shows, real rates prior to the 2008/09 crisis were routinely above 2%. Let’s assume that’s an average and that inflation settles around 3% (as target rates look a stretch). In that scenario, you could easily expect to see nominal 10-year yields above 5%. How might that alter your allocations? There’s still time to check your bearings

Source: Federal Reserve Bank of Cleveland

There's no alpha in single decision markets

If looking for alpha, you probably won’t find much in the US. The larger indices are single decision markets, such is the concentration of the Mag7. The only decision an active investor must get right, is how much of the Mag 7 to own? Some simply avoid making that decision, and own the index instead. Others may even seek alpha in markets where more inefficiencies exist, and less indexation/crowding occur. But that means being different. Something few are comfortable with, although over time, more may need to learn how to live in the out of consensus square.

Tech's dirty little secret (and its hidden value)

My basic premise is that the scarcity, and therefore value for the technology sector may not solely lie in the IP (the thing we see and interface with) but in the supply chain, the material world, that remains hidden, forgotten and overlooked (conveniently so when calculating the tech-sector’s carbon intensity). As Ed Conway illustrates, this world is mission-critical to our promised future, perhaps more now than ever, and to enabling this bounty. And yet I can find exposures on single digit PE’s and huge dividend yields. This at a time investors seem to be questioning whether their intuitive desires to disassociate from "dirty" industries is having the desired effect on decarbonistaion. A zero carbon portfolio may not produce a zero carbon world. It could in fact, according to Shue and Hartzmark, make it worse. Another question being asked: is it right to ignore the carbon intensity of silicon before it gets to the fab, or indeed the carbon used to produce that fab itself? This is for another time perhaps. For now, and for those focusing on the picks and shovel makers in the gold rush (Nvidia), I ask, why not also focus on the materials that make them. Without which, no picks. No shovels. No eye-watering valuations.

Bias and Diversity

Ever noticed yourself saying ‘let’s drill down into that’ when wanting to go deeper on a topic? I do it all the time, yet I’ve noticed younger people say ‘let’s double click on that’ instead. I reminder of how different generations are conditioned by different things, different trends. Even different industries. This may be why younger investors will struggle with my logic above – it’s simply not part of their thinking, their conditioning. But perhaps communication solves this. I hear a lot about reverse mentoring, where young workers teach the old about the new. But are we making efforts the other way? There is so much potential for intergenerational learning and the evidence is pretty clear; the more diverse the inputs, the better the decision outcomes. We’re getting better at promoting ethic, gender, economic and sexual diversity in leadership. But what about age?

Avoiding stupidity

“Stupidity well-packaged can sound like wisdom” is how one reader once described my writing. In order to not feign wisdom (or sound stupid) I’ll refer to experts on things I know little about or always get wrong. Like China. One such person is our Chief Economist, Carl Tannenbaum, who was not only a cool head throughout the SVB issue, but a lonely voice cautioning against excitement around the so-called Chinese reopening trade. In his team's latest note here, his colleague Vaibhav Tandon quips, “interestingly, if one started digging in Beijing and burrowed 12,000 kilometres to the other side of the earth, you would emerge in Argentina. As China stares into its economic hole, that is not a destination it wants to reach”. Quite.

Don’t pick a fight with price

The other economist I will refer to, lest observe, is the market. Here the picture is less clear. Despite western media calling this ‘China’s Lehman moment’, the prices of some Chinese proxies seem less bothered. Yes the property sector has been hit, with defaults a real concern, sharply higher CDS and weaker Yuan. But if there was a risk to collateral, shouldn’t the highly exposed banks be hit? Most are up 5% YTD. And what about construction materials? They should suffer. Yet, Dalian iron-ore futures are up 17%? And big trading partners like Brazil and Germany are up 17% and 13% respectively. Yes, this could be a crisis moment. But if it was, it would be the first to occur with US treasuries selling off. It’s all very confusing, save to say that of all the markets to have done quite well of late, they share one thing in common. They’re undervalued. A reminder, that starting valuation is still the most powerful determinant of future returns. And price is not something you want to pick a fight with.

Japan – still good value

Despite the rally, Japanese stocks still look potentially undervalued. While a number of the more expensive global technology names have been hit for reasons discussed (see Advantest, Tokyo Electron etc.) others have quietly consolidated, in anticipation of the next move higher. The Low PB and Cash Rich ETF (MSAPJPBL) we first discussed in February is up 30%, interestingly led by Steel (see above: Material World). It’s 1% away from multi-year highs, still trades on 8x prospective, with +3% dividend in a country that yields 0.6%. Nearly half (45%) of the stocks in the Topix still trade below BV, which itself could be understated given assets are held on balance sheets at their purchase price or market value, whatever is lower. And 40% have net cash of > 20% of their equity. So, when/if further restructuring occurs, cash proceeds can be used for buy-backs without impacting balance sheet liquidity. Good news for eps. This all within a context of reforms, be it government support for domestic equity ownership (tax free NISAs), efforts to improve governance, female board participation and inflation. Something few CEOs will have ever dealt with in their careers. Nor those writing the accounting rules. Japan could become even better value than it currently looks. For anyone interested, see this from River and Mercantile: Not Just a Flash in Japan.

Following fashion

I’ve followed Pippa Malmgren for years. She’s convinced everyday signs can tell us a lot about the economy, which she wrote about in her book “Signals” (available at all good book shops). To this end, she’s a keen observer of fashion and has argued the runways of Milan tell us a lot about the fortunes of Wall Street. To this end, and with reference to last week’s missive, I wonder what she’d make of superstars Bella Hadid, Julia Fox and Rihanna wearing football jerseys, and Balenciaga and 3.PARADIS featuring them in recent runway shows. A tell, perhaps, to the future of sport, and in particular elite women sports which looks extraordinarily good value, at ~1/10th its closest comp (men’s sport) and where advertisers get 7x returns on their sponsorship dollars. Where else can you combine profit with purpose (think equality) and expose yourself to market where very soon there will be more female millionaires, than male ones? If only there were a thematic fund or ETF set up to capitalise on such opportunities. If only.

NEITHER THE INFORMATION NOR ANY VIEWS EXPRESSED CONSTITUTES INVESTMENT ADVICE AND IT DOES NOT TAKE INTO ACCOUNT THE SPECIFIC INVESTMENT OBJECTIVES, FINANCIAL SITUATION AND THE PARTICULAR NEEDS OF ANY SPECIFIC PERSON WHO MAY VIEW THIS MATERIAL.

These are my own personal views, not those of my employer. This report is not intended for retail customers. Any further disclosure, use, distribution, dissemination or copying of this report or any of the information herein is strictly prohibited. The information in this report has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Any opinions expressed herein are subject to change at any time without notice. Any person relying upon information in this report shall be solely responsible for the consequences of such reliance. This report is provided for informational purposes only and does not constitute legal, tax or other advice nor does it constitute an offer or solicitation to purchase or sell any security, commodity, currency or other product. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining advice from their own advisors. Internet communications are susceptible to alteration and Northern Trust shall not be liable for the message if it has been altered, changed or falsified.

Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.