- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Overcoming the Fear of Market Entry

Key findings on reducing market entry anxiety and optimizing for long-term goals.

By Peter Mladina, Executive Director of Portfolio Research, Wealth Management

Steven Germani, CFA, CFP®, Director of Investment Analytics, Wealth Management

For investors holding cash on the sidelines, the fear of market entry is pervasive. In bull markets, they fear an imminent correction. In bear markets, they fear the correction will worsen. But market entry must be considered in the context of the investor’s financial goals and the opportunity cost of remaining un-invested. When investors consider their financial goals and the real returns required to fund them, the optimal place to be is invested in their long-term strategy.

Capital markets are highly competitive pricing engines. The best evidence for this is the fact that alpha, or risk-adjusted excess return from manager skill, is extremely rare.1 Capital markets attempt to price a positive forward-looking return as compensation for bearing risk such that stocks have a higher expected return than bonds, and bonds have a higher expected return than cash (at least over longer holding periods).

Investors should focus on what they can control and finding the opportune time to enter the market is not likely one of them. Equity returns are highly unpredictable in the short-term. When testing equity returns since 1926, we find no relationship between the previous and subsequent quarter’s returns, or between the previous and subsequent year’s returns.2 In other words, the return over the next year has no relationship to the return of the past year. Similarly, valuations show no meaningful ability to predict one-year returns (though return predictability increases somewhat over much longer time horizons).3 Investors should not consider recent returns or rely too heavily on current valuations when investing excess cash into their long-term strategy.

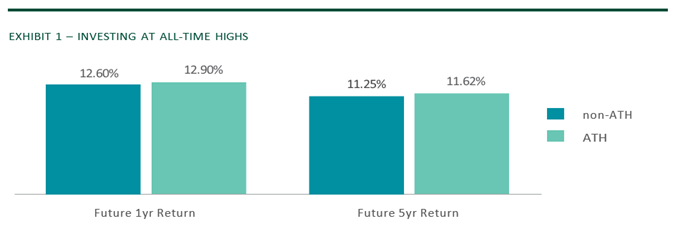

INVESTING AT ALL-TIME HIGHS

Investors are often apprehensive to invest excess cash into equities when the market achieves all-time highs. But the occurrence of all-time highs is surprisingly common, with the S&P 500 making a new all-time high about 30 times per year on average.4

Exhibit 1 shows the average subsequent one-year and five-year annualized return of the S&P 500 after investing at an all-time-high (ATH) compared to investing on any other day since 1950. The average annualized returns are about the same (actually slightly higher) when investing at all-time highs. These results are robust to more contemporary time frames (e.g., since 1990). Investors should not fear all-time highs when investing excess cash into their long-term strategy. Nor should investors fear stock-market drawdowns (lows), which are also followed by higher average one-year and five-year returns.

DOLLAR-COST AVERAGING

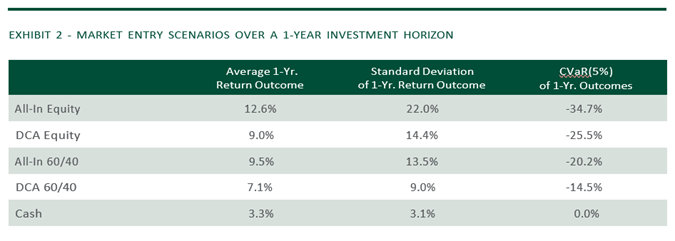

Dollar-cost averaging (DCA) is one common approach to mitigate the risk of market entry. But even DCA can be boiled down to a risk/return trade-off. Exhibit 2 compares the risk and return of four market entry scenarios over one-year investment horizons formed from rolling quarterly returns since 1926.5 The All-In Equity scenario represents an immediate investment in the S&P 500 that is held for one year. The DCA Equity scenario represents an initial cash position that is incrementally invested 25% each quarter in equities over one year. The All-In 60/40 scenario assumes an immediate investment in a balanced portfolio of 60% equities and 40% intermediate-term government bonds, a position held for one year. The DCA 60/40 scenario assumes an initial cash position that is incrementally invested 25% each quarter into the 60/40 portfolio over one year.

Exhibit 2 shows that over a one-year period – a realistic DCA timeframe in practice – DCA does indeed reduce risk. Both the standard deviation (the uncertainty or dispersion around future one-year return outcomes) and the conditional value at risk (CVaR, or the weighted average of the worst 5% of one-year return outcomes) show reduced risk when employing DCA to enter either an equity or a balanced 60/40 portfolio. However, this reduced risk comes at the cost of a reduced average one-year return. All-In Equity produces 3.6% more return on average over the one-year period than DCA Equity. All-In 60/40 generates 2.4% more return than DCA 60/40. The results are directionally the same when we limit the analysis to a more contemporary timeframe (e.g., since 1990). The decision to invest all-in or to dollar-cost-average over a one- year investment horizon is a risk/return trade-off that depends on the investor’s personal risk preference.

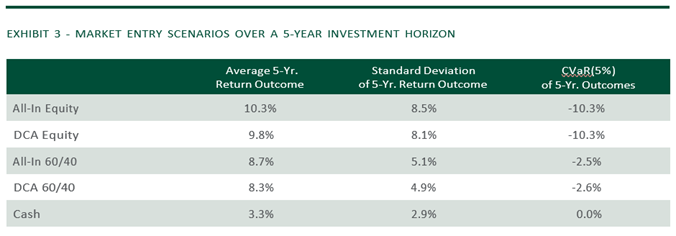

Exhibit 3 reproduces the same market entry scenarios as Exhibit 2 but compares annualized risk and return outcomes after five years. Over the longer holding period, the risk of the All-In scenarios more closely resembles the risk of the DCA scenarios, while All-In still maintains a higher average annualized return outcome. Investors fearing market entry today should consider this longer-term view, which is likely to be more aligned with their financial goals.

The risks to market entry are closely related to the same risk/return trade-off that dominates the investment landscape. Returns are largely unpredictable in the short run and only partly predictable over the long run, so the decision to deploy excess cash into a long-term investment portfolio should not weigh recent returns. DCA can help mitigate the risks of market entry but at the expense of giving up a higher average expected return. And the risk-reducing benefit of DCA diminishes with longer investment horizons. When investors consider their financial goals and the real returns required to fund them, the optimal place to be right now – and always – is in a diversified, long-term strategy aligned with those goals.

- See Mladina and Germani, “Manager Performance and Persistence,” Northern Trust Research (2022).

- We tested the serial correlation of the IA SBBI US Large Stock quarterly and annual returns from 1926 to Q1 2024. The R-squared (explained relationship) between the sequential returns is 0%.

- We tested this by running predictive regressions on the inverse of initial valuation ratios (price- to-earnings, Shiller cyclically-adjusted price-to-earnings, and price-to-cash flow) from common inception of the valuation data (January 1970) versus subsequent returns on the MSCI USA Index through April 2024.

- Based on S&P 500 daily price data from Jan. 1950 through May 2024. Subsequent one-year and five-year returns use S&P 500 daily total return data over the same period.

- The DCA analysis uses IA SBBI US Large Stock and IA SBBI US Intermediate-Term Government indices.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S.

This document is a general communication being provided for informational and educational purposes only. The opinions and conclusions expressed herein are those of the authors and are not meant to be taken as investment advice or a recommendation for any specific investment product or strategy and does not take your financial situation, investment objective or risk tolerance into consideration. Performance examples are hypothetical and for illustration purposes only and actual results may be lower or higher than a portfolio that may be more or less diversified and/or managed in a different manner. In performing its services, Northern Trust will take into account other relevant facts and circumstances such that positions and transactions for any particular client account may differ with the investments described herein. Northern Trust provides fiduciary and investment management services to various types of accounts, including but not limited to, separately managed accounts, registered and unregistered funds. The investment advice given to one client account may differ from the investment advice given to another client account. Northern Trust and its affiliates may have positions in, and may effect transactions in, the markets, contracts and related investments described herein, which positions and transactions may be in addition to, or different from, those taken in connection with the investments described herein. All information discussed herein is current only as of the date of publication and is subject to change at any time without notice. This material has been obtained from sources believed to be reliable, but its accuracy, completeness and interpretation cannot be guaranteed. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining specific legal, accounting or tax advice from their own counsel.

All investments involve risk and can lose value. The market value and income from investments may fluctuate in amounts greater than the market. Forecasts may not be realized due to a multitude of factors, including but not limited to, changes in economic conditions, corporate profitability, geopolitical conditions or inflation.

LEGAL, INVESTMENT AND TAX NOTICE. This information is not intended to be and should not be treated as legal, investment, accounting or tax advice.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS. Periods greater than one year are annualized except where indicated. Returns of the indexes also do not typically reflect the deduction of investment management fees, trading costs or other expenses. It is not possible to invest directly in an index. Indexes are the property of their respective owners, all rights reserved.