- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Size and Style Biases in Popular Stock-Market Indices

Despite the discovery of additional factors in subsequent years, market, size and value are the genuine risk factors in real-world equity portfolios.

By Peter Mladina, Executive Director of Portfolio Research, Wealth Management

Andrew Gauthier, Senior Investment Research Analyst, Wealth Management

David Moore, CFA, CAIA, Director of Manager Research, Wealth Management

Fama and French (1993) showed that market, size and value factors explain the return and risk of diversified equity portfolios. Despite the discovery of additional factors in subsequent years, Mladina and Germani (2022)1 showed empirically that these three factors are the genuine systematic risk factors in real-world equity portfolios.

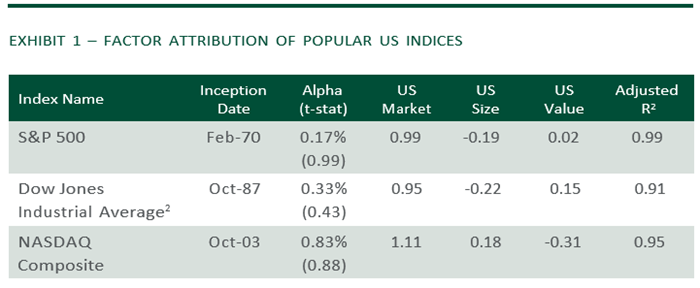

The S&P 500, Dow Jones Industrial Average and NASDAQ Composite are the three most commonly cited US stock market indices in the financial media. We demonstrate each is simply a unique mix of the three factors, with varying sensitivities to market risk, small vs. large size biases, and value vs. growth style tilts. Exhibit 1 provides the results of regressions of each index’s returns since inception through March 2024 on US market, size and value factors.

The alphas for each index are statistically insignificant (t-stat < 1.96), meaning there are no unexplained return premiums (i.e., no true, non-random alphas). And the high adjusted R2 indicates the risk (variance) of each index is well-explained by its unique exposure to the three systematic risk factors. The factor betas (exposures) tell us the S&P 500 has a large cap bias (-0.19 size beta) with no meaningful style tilt (0.02 value beta). The Dow Jones Industrial Average also has a large cap bias (-0.22 size beta) but with a moderate value tilt (0.15 value beta). The NASDAQ Composite has higher sensitivity to market risk (1.11 market beta), along with a moderate small-cap bias (0.18 size beta) and material growth tilt (-0.31 value beta). When interpreting the reported returns of these popular indices, investors should be aware that they are explained by simple differences in the underlying factor mix.

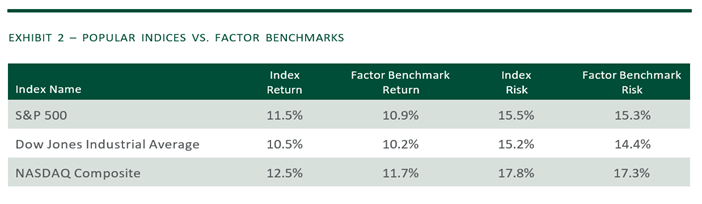

To make these results more intuitive, we construct factor return benchmarks for each index from their respective mixes of factor betas. Exhibit 2 compares the annualized return and risk (standard deviation) of each index to those of its factor benchmark.

The returns of the three indices are nearly identical to the returns of their respective factor benchmarks. The small observed return differences in Exhibit 2 are random because the alphas are random in Exhibit 1. The standard deviations of the three indices are also nearly identical to those of their respective factor benchmarks (though the risk of the Dow is a bit higher than its benchmark because it is less diversified). Factor exposures almost entirely explain the return and risk of these popular stock market indices over the long run.

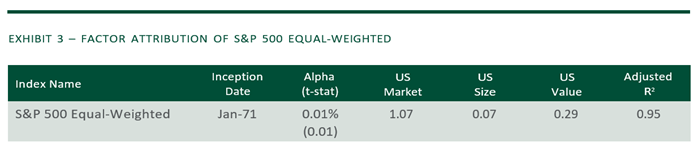

The factor betas for each index have been remarkably consistent over any lookback period of the past twenty years, which is noteworthy given the rise of the so-called “Magnificent 7” stocks during the last decade. The “Magnificent 7” now comprise nearly one-third of the market value of the S&P 500, leading some to consider use of the S&P 500 Equal Weighted index in an attempt to capture broader breadth of the US equity market than the capitalization-weighted S&P 500. Exhibit 3 shows the results of our regression of S&P 500 Equal Weighted index returns on US market, size and value factors since index inception through March 2024.

Again we find that the alpha is statistically random, so there is no unexplained return premium. And the high adjusted R2 indicates risk is well-explained by its underlying factor mix. The equal-weighted index has a more neutral size bias (0.07 size beta) than the standard S&P 500 (-0.19 size beta), but perhaps, surprisingly, it has a meaningful value tilt (0.29 value beta). In other words, there is nothing unique or different about the S&P 500 Equal-Weighted index; it is just another permutation of factors.

In fact we can closely replicate the return and risk of the S&P 500 Equal-Weighted index with a blend of the S&P 500 and Russell 2000 Value (small cap value) indices. For example, over the trailing ten-year period ending March 2024, the S&P Equal-Weighted index returned 10.9% (annualized) with 16.6% standard deviation, while a 70/30 blend of the S&P 500 and Russell 2000 Value returned 11.3% with 16.1% standard deviation — the return and risk are nearly identical.3 However, the S&P 500 Equal-Weighted index requires far more turnover to rebalance, generally resulting in higher transaction costs and taxes for taxable investors.

International versions of the three factors also explain the return and risk of international stocks. The MSCI EAFE is perhaps the most popular international equity index. Exhibit 4 shows the regression results of the MSCI EAFE against international market, size and value factors from the 1990 inception of the international factors through March 2024.

The alpha is random and the mix of factor betas well explains the return and risk of international stocks. The MSCI EAFE index has a large cap bias (-0.19 size beta) and neutral style orientation (0.02 value beta) when factors are constructed from international stocks only.

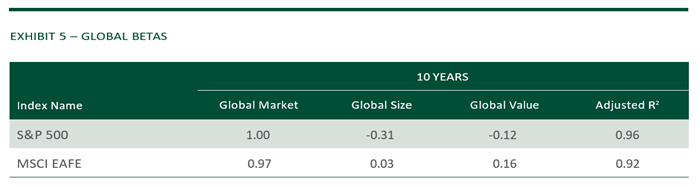

Global investors seek the diversification benefit of owning both US and international equities. Therefore, it is worth evaluating size and style biases of US vs. international indices when factors are constructed from global (i.e., US plus international) stocks. Exhibit 5 provides the factor betas for the S&P 500 and MSCI EAFE over the last ten years (ending March 2024) using global factors.

The S&P 500 has a mega-cap bias (-0.31 size beta) and modest growth tilt (-0.12 value beta), while the MSCI EAFE has a neutral size bias (0.03 size beta) and modest value tilt (0.16 value beta). An investor seeking broad diversification can eliminate latent size and style biases by owning global equity instead of having a heavy US bias.

Systematic risk factors almost entirely explain the returns of widely-referenced stock indices, as well as the returns of diversified mutual funds, exchange-traded funds, and separately-managed accounts. Investors should be aware of these exposures in their portfolios, as they are the fundamental drivers of equity return and risk.

1 Mladina and Germani, “Stock-Market Risk Factors and Manager Performance,” The Journal of Portfolio Management (2022).

2 Total Returns for the Dow Jones Industrial Average in Morningstar Direct are first available in October 1987.

3 A blend of 70% S&P 500 and 30% Russell 2000 Value minimizes tracking error to the index.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S.

This document is a general communication being provided for informational and educational purposes only. The opinions and conclusions expressed herein are those of the authors and are not meant to be taken as investment advice or a recommendation for any specific investment product or strategy and does not take your financial situation, investment objective or risk tolerance into consideration. Performance examples are hypothetical and for illustration purposes only and actual results may be lower or higher than a portfolio that may be more or less diversified and/or managed in a different manner. In performing its services, Northern Trust will take into account other relevant facts and circumstances such that positions and transactions for any particular client account may differ with the investments described herein. Northern Trust provides fiduciary and investment management services to various types of accounts, including but not limited to, separately managed accounts, registered and unregistered funds. The investment advice given to one client account may differ from the investment advice given to another client account. Northern Trust and its affiliates may have positions in, and may effect transactions in, the markets, contracts and related investments described herein, which positions and transactions may be in addition to, or different from, those taken in connection with the investments described herein. All information discussed herein is current only as of the date of publication and is subject to change at any time without notice. This material has been obtained from sources believed to be reliable, but its accuracy, completeness and interpretation cannot be guaranteed. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining specific legal, accounting or tax advice from their own counsel.

All investments involve risk and can lose value. The market value and income from investments may fluctuate in amounts greater than the market. Forecasts may not be realized due to a multitude of factors, including but not limited to, changes in economic conditions, corporate profitability, geopolitical conditions or inflation.

LEGAL, INVESTMENT AND TAX NOTICE. This information is not intended to be and should not be treated as legal, investment, accounting or tax advice.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS. Periods greater than one year are annualized except where indicated. Returns of the indexes also do not typically reflect the deduction of investment management fees, trading costs or other expenses. It is not possible to invest directly in an index. Indexes are the property of their respective owners, all rights reserved.