- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

A Frenzied Week for Tariffs

Trade policy clarity is a long way off.

By Carl Tannenbaum

British Prime Minister Keir Starmer had a productive visit with President Trump last month. Observers attributed Starmer’s success to an affable style, but it may have had more to with the trade surplus the United States runs with Britain. That puts the U.K. well down the list of regions attracting the administration’s attention under the new American trade policy.

One little-known export that the U.S. received from England some years ago was the term “stagflation.” This elision of “stagnation” and “inflation” became the single best descriptor of the American economy of the 1970s. During that era, sluggish growth and rising prices proved a toxic combination for households and the Federal Reserve.

In the past few weeks, economists have been using the word stagflation to describe what might lie ahead for the U.S. The size and scale of tariffs confirmed this week, along with retaliatory measures announced by China and Canada, will depress economic activity and place upward pressure on inflation.

To say that tariff policy is fluid at present is an understatement. Charges on Canadian and Mexican imports had been deferred for a month; as we approached last Monday’s deadline, most expected the deferral to be extended. The President surprised by forging ahead, prompting retaliatory measures from America’s trading partners.

U.S. trade policy, and financial markets, have been volatile.

In the wake of a market correction, the Commerce Secretary announced thirty-day reprieves: first for domestic automakers, and then to a slightly broader range of imports from Mexico and Canada. Still to come are potential measures against the European Union, and selected emerging markets.

Tariffs act like taxes, paid largely by households. They depress consumption and economic growth. Tariffs add to inflation by raising the prices of imports; domestic producers in affected sectors often increase their prices, as well. (The case of washing machines is illustrative here.)

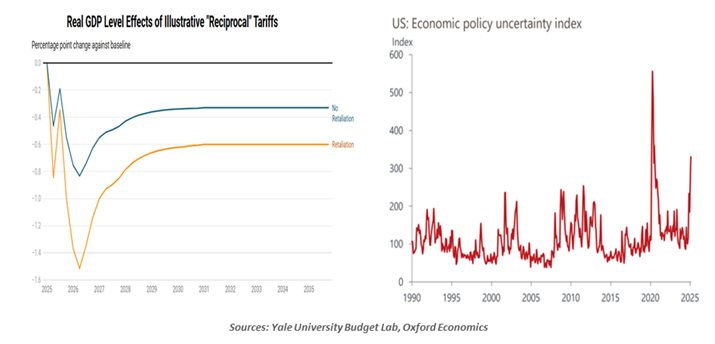

The magnitudes of these impacts depend on many things, including the presence of substitutes for imported goods and the ability of households to defer spending on them. For tariffs as widely ranging as those proposed in the last six weeks, the modeling can be very complex. But several sources have estimated declines of U.S. real growth in excess of 1% next year, and increases in inflation of more than 0.5%. The consequences for Canada and Mexico are much more severe.

The uncertainty surrounding process and policy has put businesses in a difficult position. When the rules of commerce are in flux, it is hard to commit to productive investment. The manner in which measures are forwarded has created considerable day-to-day drama, which hasn’t helped. There are those who suggest that being hard to read will provide an advantage as negotiations progress. Others worry that recent tactics will cause trading partners to lose interest in bargaining, and encourage them to deepen alliances that don’t include the United States.

After remaining somewhat sanguine through the month of February, investors are recalibrating. Equity indices and long-term interest rates have returned to their standings on Election Day. Daily volatility in both arenas has jumped. Markets now expect the Federal Reserve to reduce rates more aggressively this year, betting that diminished growth will take precedence over higher inflation in the Fed’s deliberations.

We have been frequently asked to identify the end-game sought by the new administration. There is certainly a wish to see more production performed in the United States, and to ensure that trade terms create a level playing field for American exporters. Tariffs are also being used as a lever to open deeper discussions on issues like migration and drug interdiction. What remains unknown is when these efforts will be seen as reaching their goals; measures of policy success have not yet been defined.

By the early 1980s, the combination of inflation and unemployment, also known as the “misery index,” exceeded 20%. Today’s misery index is only 7%, so increases from here would have to be classified as “mini-stagflation.” But misery is something that we shouldn’t welcome, or export.

Related Articles

Read Past Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.