- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

A Destination for Asset Allocators

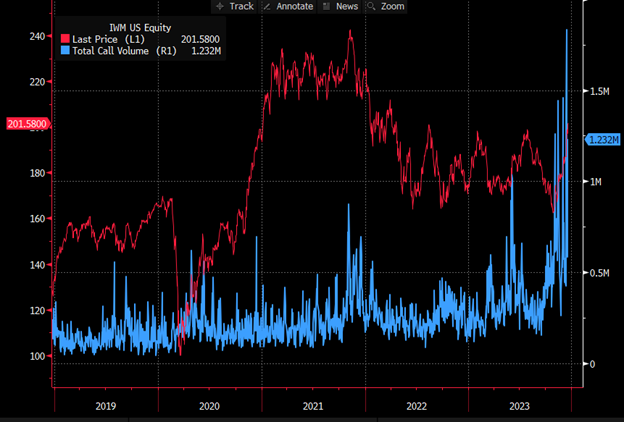

Fueled by an in-line CPI print on December 12th and a market perceived Fed “pivot” at the December 13th FOMC meeting, an end of year “everything rally” ensued with a notable exuberance for US small cap equities. The options market in particular has seen aggressive buying of IWM (iShares Russell 2000 ETF) call options. The volume of IWM call options traded hit all-time highs this month as investors piled in, speculating on further upside in US small cap equities. Most notably, on December 14th, 1.833 million calls were traded, the most IWM call options ever traded in a single day. The 5-year chart of IWM ETF price (red) is plotted vs. the IWM total call volume below, showcasing how drastic the increase in call volumes has been towards the end of this year.

Source: Bloomberg

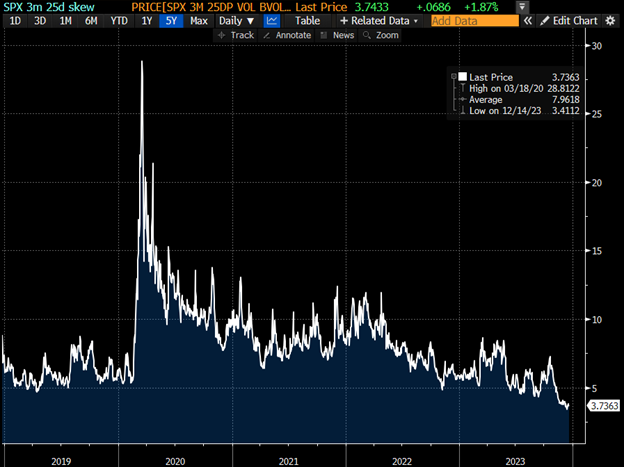

Moreover, there is relatively very little interest in downside protection as evidenced by the put/call skew for S&P 500 options. Put/call skew compares how the implied volatility (and therefore expensiveness) of put options compares to the implied volatility of call options. In general, there is almost always a larger demand for put options compared to calls and that demand drives the implied volatility higher for puts than it does calls.

Below is the SPX (S&P 500 Index) 3-month 25delta skew charted over the previous 5 years, defined as the price difference between SPX 3-month 25delta put versus SPX 3-month 25delta call. For example, when this index peaked in March 2020 investors were paying $28.81 more per contract for puts versus the equivalent 25 delta call. That put/call skew bottomed at just $3.41 on Dec. 14th which is the lowest the demand for S&P 500 puts vs. calls has been in over 5 years.

Source: Bloomberg

The speculative fervor in the market is very sentiment driven at present. There has been very broad participation in the rally, which contrasts with the heavy buying of the Magnificent 7 (AAPL, MSFT, GOOG, AMZN, NVDA, META, TSLA) during much of the year. Based on an American Association of Individual Investors (AAII) sentiment survey, sentiment is also on the higher end of the range, with 32% of survey respondents more bullish than bearish.1 These survey responses contrast to the -26% result in late October before the rally.

Signs point to a moderation of the recent rally or perhaps even a pullback in Q1, 2024, as this level of market exuberance is likely not sustainable over the medium to long term.

1 AAII Investor Sentiment Survey | AAII

Northern Trust Securities, Inc.(NTSI), Member FINRA, SIPC and a subsidiary of Northern Trust Corporation. Products and services offered through NTSI are not FDIC insured, not guaranteed by any bank, and are subject to investment risk including loss of principal amount invested.

NTSI does not accept time sensitive, action-oriented messages or securities transaction orders, including purchase and/or sell instructions, via e-mail. Additional disclosures are included in the link, see http://www.northerntrust.com/ntsidisclosure.

Links to third-party Web sites are provided for your convenience and informational purposes only. NTSI is not responsible for the information contained on third-party Web site(s).

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. This material is directed to professional clients only and is not intended for retail clients. For Asia-Pacific markets, it is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author's employer, organization, committee or other group or individual. The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 7th floor, Claude Debussylaan 18 A, 1082 MD Amsterdam; Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE Norway Branch, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651)/Northern Trust Fiduciary Services (Guernsey) Limited (29806)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) are licensed by the Guernsey Financial Services Commission. Registered Office: Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386), Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.