The Weekender

My weekly perspective on global market developments and their potential broader implications

Gary Paulin

Head of International Enterprise Client Solutions

JUNE 24, 2023

Complex problems need comprehensive solutions

As I travel to different regions I sense a growing unease, almost frustration, around the issue of ESG, particularly around the “E”. There are still issues with standardised metrics, fragmented rules, data quality, a lack of resources, and limited investment options. It’s being challenged as demand collides with pressures for legitimacy and performance. ESG mentions on earnings calls have plummeted and according to Moody’s, only 18 states in the US are actively encouraging ESG investing, whereas 27 states have opposed it. What’s interesting however, is that not all the opposition is based on ideology or self-interest. Some of it is very thoughtful, balanced, and logical. “Why should we reward carbon divestment if that asset just falls in the hands of another, possibly less efficient owner? Should we applaud countries for meeting emission targets through de-industrialisation and outsourcing? They haven’t fixed the problem, just moved it somewhere else. And if you want to travel to this promised land of zero carbon, who is going to pay the miners (of copper, lithium, and silica) to get you there?” These questions must be addressed, for the enormity and complexity of this issue can only be answered with holistic and comprehensive solutions. We’re in this together.

Don’t shoot the messenger

Now, it’s not for me to judge, nor is it helpful to do so, as to how others think about climate investing. What might help is highlighting the arguments. It’s better to be informed than opinionated, especially when accepted narratives are being challenged. Many now agree Exclusion vs Engagement is a false dichotomy. It’s more nuanced than that. Those who have resources/governance structures will exercise their shareholder rights and actively engage with management, either alone or in concert. Some will even divest if they feel a lack of alignment with their values (for example, see The Church of England’s recent divestment of National Grid and Shell). That said, it helps to frame the approaches. “Exclusion” attracts most of the attention (and capital), since it’s driven in part by regulatory prescription. But after listening to ExxonMobil’s CEO explain the importance of having a wider perspective and more balanced debate (see Tangen’s interview here), I decided to explore “Engagement,” for it seems logical that getting to net zero can’t be achieved just by rewarding the clean to get cleaner: there must be incentives for the dirty to get cleaner more quickly. Moreover, broadening our perspectives to include a wider consideration of the full life-cycle and value chain for service (i.e., “green”) businesses, one will find a reality that should not be ignored if seeking better climate outcomes. What follows therefore is not my view, but an attempt to add a perspective, balance, and logic to what is often a narrow, binary, and emotive topic. Please, don’t shoot the messenger.

Why now?

So why now? What’s changed? Well, it’s not the hose-pipe bans (which are coming) but three things have emerged to shift the conversation: we now have evidence, a story, and powerful incentives. The evidence comes from Yale, the story from a new book called “Material World,” and the incentive from the Inflation Reduction Act (IRA).

Kill emotion with logic

Let’s start with the evidence; the logic by which we might diffuse some of the emotion that exists. A recent research paper from two Yale academics called Counterproductive Sustainable Investing: The Impact Elasticity of Brown and Green Firms argues that the current ESG investment framework, despite its good intentions, is counterproductive. The authors, Hartzmark and Shue, point to a potential blind-spot in the ESG investing movement: the belief that excluding brown firms will fix the climate problem. In contrast, the study finds, it could exacerbate it. In other words, the $50 or so trillion dollars likely to be invested in ESG over the coming year or two (per Bloomberg) could be making the situation worse.

An inconvenient truth

Shue and Hartzmark show that directing capital to firms that are already green leads to only small improvements in impact “at best.” These firms are unlikely to spend on new green technology, and more likely to expand their normal activities. Conversely, withdrawing capital and increasing financing costs for brown firms not only removes incentives to go green, but it also encourages them to make short-term decisions and possibly pollute even more! In other words, “sustainable investing” may be counterproductive in that it “makes brown firms more brown without making green firms more green.” Effectively the authors are saying that if you ignore brown firms, you are ignoring those most likely to save the world. After all it’s the brown firms that own most of the green-technology patents. They suggest sustainable investing flows and engagement that targets the incentives of green firms would be more effective if it targeted at Brown firms. They would prefer a regime that rewards brown firms to go green, not just one for green firms to get (a little) greener. Yes, these might make a profit, but purpose is the priority here. Or so I thought (another talk show, perhaps?)

A wider perspective

Now, the accepted narrative is that service companies are good: they don’t burn much fossil fuels nor do they destroy the earth’s crust. That’s true. They don’t. But this ignores the reality that for them to exist at all, they are critically dependent on the material world. For example, neither Apple nor Nvidia could function without sand. Without sand there are no silicon chips. No chips, no cars. No salt, no purified city water. No glass, no cities. McDonald’s would be out of business without natural gas. Alphabet, Microsoft, Tesla, and Amazon need a functioning energy and communication network, one built using untold (and unaccountable) amounts of copper, lithium, and steel. And oil. Now we all know this implicitly. But it’s never really been brought to our attention and regulators seem more focused on downstream impacts (think scope 3) than upstream ones. But perhaps that’s about to change. Perhaps we’re about to experience an awakening of sorts. One catalysed by a story. A story about our material world, how dependent we are on it, and how much more dependent we’ll become if we hope to transition to a greener future.

Storytelling

Storytellers play a pivotal role in driving change by capturing the hearts and minds of audiences. They have the power to transform complex ideas into compelling narratives that resonate with people on an emotional level. Storytellers can inspire action, shift perspectives, and mobilize individuals and communities towards meaningful change. Well, one such storyteller could be Sky News editor Ed Conway. He’s just written Material World: A Substantial Story Of Our Past and Future. I have a feeling this could be one of those books. Perhaps without the impact of “The Wealth of Nations,” “The Innovator’s Dilemma,” or “Thinking, Fast and Slow,” but a book that nonetheless shatters perceptions and forces a universal rethink, or at least starts a conversation.

The ephemeral vs material world: a false dichotomy

Conway’s idea is that most of us live in an ephemeral world of apps, ideas, and services. The producers of such are deemed “green” and are judged as “good” by both society and investors (see ESG ratings/portfolios.) However, this world is only made possible by the material world, which we conveniently ignore. Take the silicon chips in your iPhone. A silicon chip must be smelted, often with coal, shipped around the world multiple times, with over half the journey occurring before getting to the Fab, much less your pocket. And yet ESG frameworks ignore this reality. They also reward divestment and outsourcing of energy-intensive processes, overlooking the fact we haven’t improved the overall outcome for the planet. Some countries have been successful in lowering carbon emissions by de-industrialisation. But arguably they have just put the problem somewhere else like China or Russia. To paraphrase ExxonMobil CEO Darren Woods, you make things worse if an asset moves from an efficient to a less efficient producer. So, from a system perspective and a climate perspective, we shouldn’t separate the material and ephemeral: they are linked and the incentives we create need to acknowledge this. For if we want to transition to a less efficient energy (the first time in history) we need everyone rowing the same way. And we need a lot more sand, salt, iron, copper, lithium, and yes, oil.

Incentives are everything

There is a great episode on Freakonomics Radio (here) that interviews Tony Will, CEO of CF Industries (listen from 36 minutes.) He highlights the importance of having the right incentives to drive behaviour. CF Industries is the largest ammonia producer in the world and accounts for about 7% of nitrogen fertiliser production. They matter. Without them, we go hungry. The problem is, they produce huge amounts of CO2 which gets vented into the atmosphere (brown = bad.) They had a plan to reduce emissions, but it was costly and would take time. But things got expedited thanks to the commercialisation of ExxonMobil’s carbon capture technology (see above: brown firms have the green patents), where they will sequester 2 million tonnes a year of CO2, equivalent to about 400,000 cars. But what’s made this all possible? The Inflation Reduction Act. That’s because what would otherwise have been a cost to them (and to ExxonMobil) can now generate an ROI and do good. Few things talk like money (just ask the PGA.) This explains the capex super-cycle that’s underway, pivoting around renewable energy, electric vehicles, batteries/charging stations, and semiconductors. It’s why manufacturing construction spending nearly doubled year over year in April (per the U.S. Census Bureau.) It helps explain why construction firms are hoarding staff and why job openings are still elevated (see JOLTS) despite extreme policy tightening. Contrast this to the UK and Canada, which use carbon taxes to limit emissions. Mr. Will suggests this “stick” approach may prove counterproductive. Companies might simply shift production to a region with higher emission standards if the economic incentives no longer make sense. While I’m sure it’s harder than it sounds, it pays being mindful of the law of unintended consequences. I refer again to New Zealand – one of the greenest countries on the planet – yet forced to import record amounts of thermal coal in 2021. And while I’m on that topic…

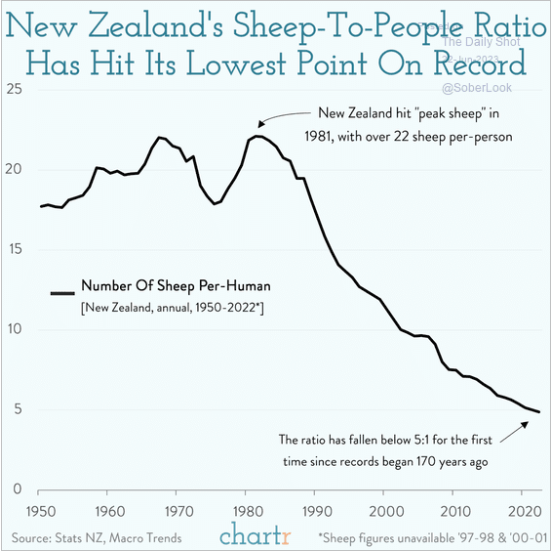

New Zealand, not the country I left

See previous missive: Demography is destiny. I have another idea for an app.

Predictions

So, my only dog in this race is the climate. I’m not taking sides but there does seem to be a counter-narrative emerging: one we need to be conversant with and one that stands in contrast to how markets are positioned. If Conway is right, getting to the promised land will involve more digging, blasting, and burning than ever before. And so, we might need to think about the incentives to ensure those doing the digging, blasting, and burning do it in the most efficient way. That and incentives to decarbonise both their own and their customers’ operations, faster. That seems to be working in the US at least (the IRA). So, as we have seen with MiFID (where I expect unbundling gets re-bundled) we may see regulators start to rethink the rules of ESG. And with the evidence and narrative described above, I wouldn’t be surprised to see more Impact Funds emerge to benefit from the value transfer from green to brown, or in other words, from exclusion to engagement. These funds will no doubt champion the idea that the climate challenge is so great that we must provide incentives to all players, especially those with green technology (think scale-carbon capture,) expertise, business skills, transferrable knowledge, and spot welders! Punishing them could, as the Yale paper says, be counterproductive.

Mean reversion and trade of the decade

So, let’s assume:

i. The counter-narrative (from ephemeral to real, bytes to atoms, ideas to things) gains traction and we see more engagement (and capital) to turn brown firms green, faster;

ii. That this transition occurs at a time when the cost of capital (and talent) for brown firms is very high thus increasing the value of installed capacity; and

iii. That mean reversion is still a thing.

Then, isn’t there a good possibility that value will transfer to regions of the world stacked full of firms operating in this more material world (UK, Japan, Brazil)? Consider that at today’s market value, the market cap of Apple would buy all the FTSE (UK) and most of the IBOV (Brazil). The S&P, the epicentre for ethereal dog-walking apps, trades on 28x CAPE. In contrast, the UK trades on 14x and the Atlantic Declaration suggests closer alignment on all the growth-tech stuff. Does that seem right? Brazil is cheaper still at 10x (and probably has even more spot-welders!) This coming at a time of more domestic focus from allocators and, in the case of the UK and Japan, multiple catalysts up ahead (see previous missives.) These remain the trades of the decade.

If you would like to receive future editions of The Weekender, please do email me at gdp2@ntrs.com.

NEITHER THE INFORMATION NOR ANY VIEWS EXPRESSED CONSTITUTES INVESTMENT ADVICE AND IT DOES NOT TAKE INTO ACCOUNT THE SPECIFIC INVESTMENT OBJECTIVES, FINANCIAL SITUATION AND THE PARTICULAR NEEDS OF ANY SPECIFIC PERSON WHO MAY VIEW THIS MATERIAL.

These are my own personal views, not those of my employer. This report is not intended for retail customers. Any further disclosure, use, distribution, dissemination or copying of this report or any of the information herein is strictly prohibited. The information in this report has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Any opinions expressed herein are subject to change at any time without notice. Any person relying upon information in this report shall be solely responsible for the consequences of such reliance. This report is provided for informational purposes only and does not constitute legal, tax or other advice nor does it constitute an offer or solicitation to purchase or sell any security, commodity, currency or other product. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining advice from their own advisors. Internet communications are susceptible to alteration and Northern Trust shall not be liable for the message if it has been altered, changed or falsified.

Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Receive The Weekender

Register your interest in receiving Gary's commentary direct to your inbox.