- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Compensated Portfolio Risk

We identify the compensated risks that multi-asset investors bear in real-world portfolios.

By Peter Mladina, Executive Director of Portfolio Research, Wealth Management

Charles Grant, CFA, Director of Asset Allocation Research, Wealth Management

Steven Germani, CFA, CFP, Director of Investment Analytics, Wealth Management

Investors often say “risk and return are related.” But not all risks are compensated with an expected return premium. For example, the risk of owning just one stock is far higher than the risk of owning all stocks, though they both have about the same expected return. The compensated risk in this example is the risk and associated return of owning all stocks, while the lack of any diversification from owning just one stock results in uncompensated risk. Compensated risks are systematic risks that investors intentionally bear to earn a reliable return premium. In contrast, uncompensated risks tend to be idiosyncratic (unsystematic) and easily diversifiable.

There are several systematic risk factors that have been shown to explain asset returns. But only two primary risk factors – term and market – almost entirely explain the compensated risk of multi-asset class portfolios owned by most investors. The term factor represents the return for bearing maturity or duration risk (i.e., interest rate risk excluding default risk). It is commonly defined as the return of Treasury bonds minus the return of Treasury bills (the risk-free asset). The market factor represents the return for bearing equity and equity-like market risks. It is commonly defined as the return of equities minus the return of Treasury bills.

Term and market factors are the basis for the Intertemporal Capital Asset Pricing Model (ICAPM) asset allocation framework we use at Northern Trust, where the term factor represents risk-control or goal-hedging assets and the market factor represents return-seeking risk assets. The ICAPM modifies term and market factor definitions so that Treasury bonds replace Treasury bills as the multi-year risk-free (hedging) asset and the ICAPM market factor is redefined as the return of equities minus the return of Treasury bonds. We find that this ICAPM framework explains more portfolio return and risk than standard term and market factor definitions.

The global market portfolio of all capitalization-weighted stocks and bonds represents the average asset allocation of all investors. It is perhaps the most diversified portfolio and composed entirely of systematic risks. In our research article, “A Benchmark for Efficient Asset Allocation,” we found that the global market portfolio outperformed more than two-thirds of discretionary asset allocation funds before fees.1 This result suggests it is a good benchmark for asset allocation.

Instead of evaluating the performance of asset allocation funds against the global market portfolio, here we evaluate them against two portfolio factor models: the ICAPM (as defined above) and the ICAPM plus a “factor zoo” that adds to the ICAPM all of the other generally accepted systematic risk factors: default and prepayment factors for bonds and size, value, momentum, profitability and investment factors (i.e., quality) for stocks.2 Our sample includes all active asset allocation funds and ETFs in the Morningstar database with at least 24 months of returns from 1990 to December 2023, including live and dead funds to reduce survivorship bias.3 We evaluate each fund’s asset allocation performance – both gross and net of fees – by regressing each fund’s excess returns against each of the two portfolio factor models.4 Our purpose is to show empirically that term and market factors, as represented in the ICAPM framework, are almost entirely the compensated risks that multi-asset investors bear in real-world portfolios.

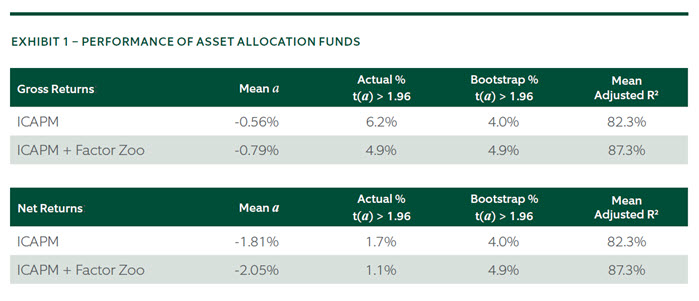

Our primary test statistic is alpha (a), or risk-adjusted excess return. If all fund alphas are random, then return premiums are all fully captured by the systematic risk factors in the factor model – i.e., there is no residual return premium attributable to either missing factors or manager skill. Our secondary test statistic is the adjusted R2, which tells us how much systematic risk the factor model explains. Exhibit 1 shows the results of our tests.

We first discuss the ICAPM results using gross returns (top panel of Exhibit 1) to better isolate asset allocation performance. The average alpha is -0.56% for the ICAPM, indicating that the average asset allocation fund does not generate a return premium above the returns attributed to their generic exposure to systematic term and market risk. We dig deeper than the average result by evaluating the highest performing asset allocation funds (the right tail of the distribution), which are those with statistically significant positive alphas (t-stat > 1.96). We compare the percentage of funds with significant positive alphas (Actual %) with the percentage of funds with significant alphas we expect to find by random chance (Bootstrap %).5 Only 6.2% of asset allocation funds generated statistically significant positive alphas according to the ICAPM, which compares to 4.0% expected by chance. This result indicates that true non-random alpha before fees is exceedingly rare according to the ICAPM – only 2.2% of asset allocation funds (the difference between actual and bootstrap results).

Is this rare alpha attributable to manager skill or missing systematic risk factors? The addition of the factor zoo to the ICAPM reduces the percentage of funds with statistically significant alphas by just 1.3 percentage points (from 6.2% to 4.9% of funds), but it is enough to explain away the rare alpha observed under the ICAPM. Only 4.9% of asset allocation funds generated statistically significant positive alphas according to the ICAPM plus the factor zoo, which precisely equals the 4.9% expected by random chance. The rare alpha we found under the ICAPM is fully explained by the other systematic risk factors in the factor zoo. This means that there is no evidence of manager skill to tactically allocate (i.e., time markets, asset classes or factors) or select securities.

The ICAPM explains 82.3% of total portfolio risk (variance) on average while the ICAPM plus factor zoo explains 87.3%, which is just five percentage points more. The remaining 12.7% is idiosyncratic. Because that idiosyncratic risk is not compensated with a reliable return premium (a true non-random alpha), it is uncompensated risk that is diversifiable. This suggests that most asset allocation funds are under-diversified.

Finally, for completeness, the bottom panel of Exhibit 1 shows the net-of-fee results. Alphas all across the distribution drop considerably due to the weight of fees.6

Term and market factors are almost entirely the compensated risks that multi-asset class investors bear in real-world portfolios. Our overall empirical results strongly support Northern Trust’s ICAPM asset allocation framework, where high-grade bonds (term) serve as hedging assets while risk assets (market) are priced in excess of hedging assets. Zoo factors have only a minor effect on multi-asset class portfolio return and risk, and they can be pursued (if desired) through implementation preferences within the ICAPM framework. A custom, goals-based investment process can help determine optimal exposures to goal-hedging assets and return-seeking risk assets based on an investor’s unique goals and risk preferences. Then sound portfolio construction can efficiently capture those exposures without any uncompensated risks, or undue expense and tax.

1. Performance was based on risk-adjusted return (Sharpe ratios). The global market portfolio outperformed more than 80% of discretionary global asset allocation funds after fees.

2. See Mladina and Germani, “Bond-Market Risk Factors and Manager Performance,” The Journal of Portfolio Management (2019) and Mladina and Germani, “Stock-Market Risk Factors and Manager Performance,” The Journal of Portfolio Management (2022) for factor definitions and sources.

3. The final sample size is 1,429 mutual funds and ETFs, which excludes passive and target-date asset allocation funds with pre-determined allocations. Inception is November 1990 when the global momentum factor becomes available.

4. We use either U.S. or global equity factors depending on which set has higher explanatory power (adjusted R2) for each strategy.

5. Because the distribution of alpha t-statistics might not follow a normal distribution, we use empirical bootstrap distributions following the method of Fama and French, “Luck versus Skill in the Cross Section of Mutual Fund Returns ,” The Journal of Finance (2010).

6. The average expense ratio in the sample is 1.05%. We use the lowest expense share class for mutual funds with multiple share classes.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S.

This document is a general communication being provided for informational and educational purposes only. The opinions and conclusions expressed herein are those of the authors and are not meant to be taken as investment advice or a recommendation for any specific investment product or strategy and does not take your financial situation, investment objective or risk tolerance into consideration. Performance examples are hypothetical and for illustration purposes only and actual results may be lower or higher than a portfolio that may be more or less diversified and/or managed in a different manner. In performing its services, Northern Trust will take into account other relevant facts and circumstances such that positions and transactions for any particular client account may differ with the investments described herein. Northern Trust provides fiduciary and investment management services to various types of accounts, including but not limited to, separately managed accounts, registered and unregistered funds. The investment advice given to one client account may differ from the investment advice given to another client account. Northern Trust and its affiliates may have positions in, and may effect transactions in, the markets, contracts and related investments described herein, which positions and transactions may be in addition to, or different from, those taken in connection with the investments described herein. All information discussed herein is current only as of the date of publication and is subject to change at any time without notice. This material has been obtained from sources believed to be reliable, but its accuracy, completeness and interpretation cannot be guaranteed. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining specific legal, accounting or tax advice from their own counsel.

All investments involve risk and can lose value. The market value and income from investments may fluctuate in amounts greater than the market. Forecasts may not be realized due to a multitude of factors, including but not limited to, changes in economic conditions, corporate profitability, geopolitical conditions or inflation.

LEGAL, INVESTMENT AND TAX NOTICE. This information is not intended to be and should not be treated as legal, investment, accounting or tax advice.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS. Periods greater than one year are annualized except where indicated. Returns of the indexes also do not typically reflect the deduction of investment management fees, trading costs or other expenses. It is not possible to invest directly in an index. Indexes are the property of their respective owners, all rights reserved.