- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Global Economic Research

Global Economic Outlook: That '70s Show

The Northern Trust Economics team shares its outlook for key markets in the month ahead.

The world is experiencing immense disruption to supplies of commodities. Prices of essentials from food to consumer goods have risen to multi-year highs, putting pressure on household wallets and corporate profits. In their efforts to tame inflation, hawkish central banks are willing to risk recession.

If this storyline sounds familiar, it’s because we’ve seen the movie before…more than four decades ago. The risk of repeating the stagflation of the 1970s is more real than ever, particularly for Europe. But we think the major markets can avoid this fate.

Here are perspectives on how major economies are poised to perform this year and next.

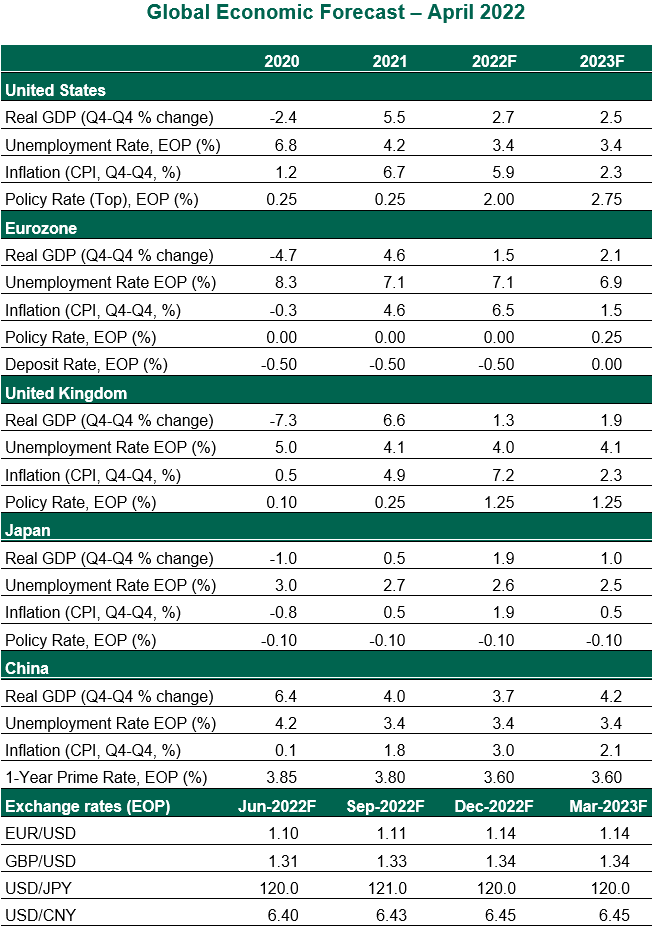

United States

- Economic growth likely slowed in the first quarter, hindered by COVID-19 infections at the start of the year. But with restrictions eased and offices reopened, the second quarter is poised to witness buoyant consumer spending despite elevated prices. What distinguishes the United States from some other markets is the degree of pent-up demand and unspent pandemic stimulus. These tailwinds should allow growth to continue, even amid policy normalization.

- Prices remain a headache for consumers, businesses and policymakers. Inflation climbed 8.5% in March from a year before, led by increases in food and energy costs. The deflator on core personal consumption expenditures grew 5.4% in February, far ahead of the Fed’s 2% target, affirming the case for rapid hikes. We expect the Fed to hike interest rates by 50 basis points in May. Tightening will continue through the first quarter of 2023, leading to a terminal rate range of 2.50-2.75%.

Eurozone

- Sustained economic reopening is a key driver of eurozone growth, but the war in Ukraine has cast a long shadow over the outlook. Pressure on member states to cut their dependence on Russian energy will add to supply chain and inflation woes. European consumers will bear the brunt of higher costs. In a worst-case scenario, cutting off supplies from Moscow will deliver a major blow to Germany, the bloc’s largest economy.

- Price gains have become more widespread in the eurozone, although the bulk of recent increases in European inflation have come from surging energy costs. Because these are unlikely to persist over the medium term and the risk of stagflation in Europe is rising, the European Central Bank (ECB) took a dovish stance at its March meeting. The ECB has kept the door open to an interest rate hike later this year, but economic and financial conditions are unlikely to offer room for tightening of monetary policy in 2022.

United Kingdom

- The rebound phase of Britain’s post-pandemic recovery is over, with recent economic measurements showing that growth is cooling. The household saving ratio is now lower than the average of the decade before the pandemic, implying limited room to cushion the blow of falling real incomes. The U.K. economy is staring at the risk of stagflation.

- Inflation stood at a three decade high of 7.0% year over year in March. It is poised to increase further with the hike in the energy price cap and the expiration of a hospitality tax break. The Bank of England raised the policy rate for the third successive meeting in March, to 0.75%. But the minutes revealed a clear change in tone amid growing concerns about the downside risks to growth. We are maintaining our call of two more hikes of 25 basis points each in May and June, followed by a long pause.

Japan

- Consumption, led by the release of pent-up demand after the Omicron wave, will be Japan’s key driver of growth in the near term. However, rising input prices and supply bottlenecks caused by the severe COVID-19 outbreak in China are posing a threat to the recovery. A resurgence of logistical disruptions hindered exports in the first two months of the year.

- With few signs of wage increases and households’ real incomes getting squeezed, we are unlikely to see sustained 2% inflation in Japan. Against this backdrop, the Bank of Japan will be the only major central bank to maintain its extremely accommodative monetary policy stance throughout our forecast horizon.

China

- COVID-19 has emerged as a key headwind for the Chinese economy. Lockdowns and highway restrictions are causing major disruption to the flow of goods and services. Consumption has been hindered by anti-virus measures; retail sales contracted 3.5% year over year in March. Income and job prospects are deteriorating. All of this led us to downgrade this year’s growth estimates for China.

- Stronger macro policy responses are expected to shore up activity and prevent a surge in defaults. These measures could come in the form of policy rate cuts, reductions in the reserve requirement ratio and higher infrastructure investment. That said, rolling out policy measures alone won’t be enough to underpin activity. Activity restrictions will prevent the easing from trickling down to the needed areas of the economy. China will have to learn to live with the virus to prevent further disruptions at home and abroad.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.