- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

December S&P 500 Index Rebalance: Market Sentiment High and Technology Trends Continue

The S&P 500 quarterly rebalance adds Apollo Global Management, Workday, and Lennox International and removes Catalent, Amentum Holdings, and Qorvo.

KEY POINTS

What it is

We analyze the impact of company additions and other weighting changes from the S&P 500’s quarterly rebalance in December.

Why it matters

Quarterly changes in indexes over time can impact the composition and performance.

Where it's going

Going forward, a careful review of liquidity conditions, expected trade flows, and optimal strategies is essential.

Every quarter, S&P-Dow Jones rebalances its flagship market-capitalization index series, including the S&P 500 Index. Changes to the index related to the rebalance may appear small but they drive significant trade volumes in the market from the announcement date (December 6, 2024, by S&P-Dow Jones) and leading up to the effective date of the changes, which is the market close on December 20, 2024. According to S&P estimates, about $16 trillion in assets are benchmarked to the flagship S&P 500, with a large portion of that in passively managed assets1 All investors should be aware of these changes but they are particularly important for index managers, who are tasked with tracking indexes with a high level of precision.

Rebalance periods at Northern Trust, one of the world’s leading managers of index assets,2 demand a significant amount of collaboration across our investment team. For all our index portfolios that are benchmarked to the S&P indexes, we must carefully manage the rebalances to ensure we achieve our primary objective of matching the risk and return characteristics of the benchmark.

Key Changes: Financial and Technology Additions Lead

This fourth and final rebalance event of the year arrives as the benchmark U.S. market gauge continues its impressive two-year run. After coming off a 2023 calendar year total return of 26.2%, the S&P 500 Index returned 25.0% in 2024, and had notched 57 all-time high marks[1] before a retreat over the last two weeks of the year. Despite the very recent softness, the U.S. market has been on a multi-year surge as we assess the latest index composition changes.

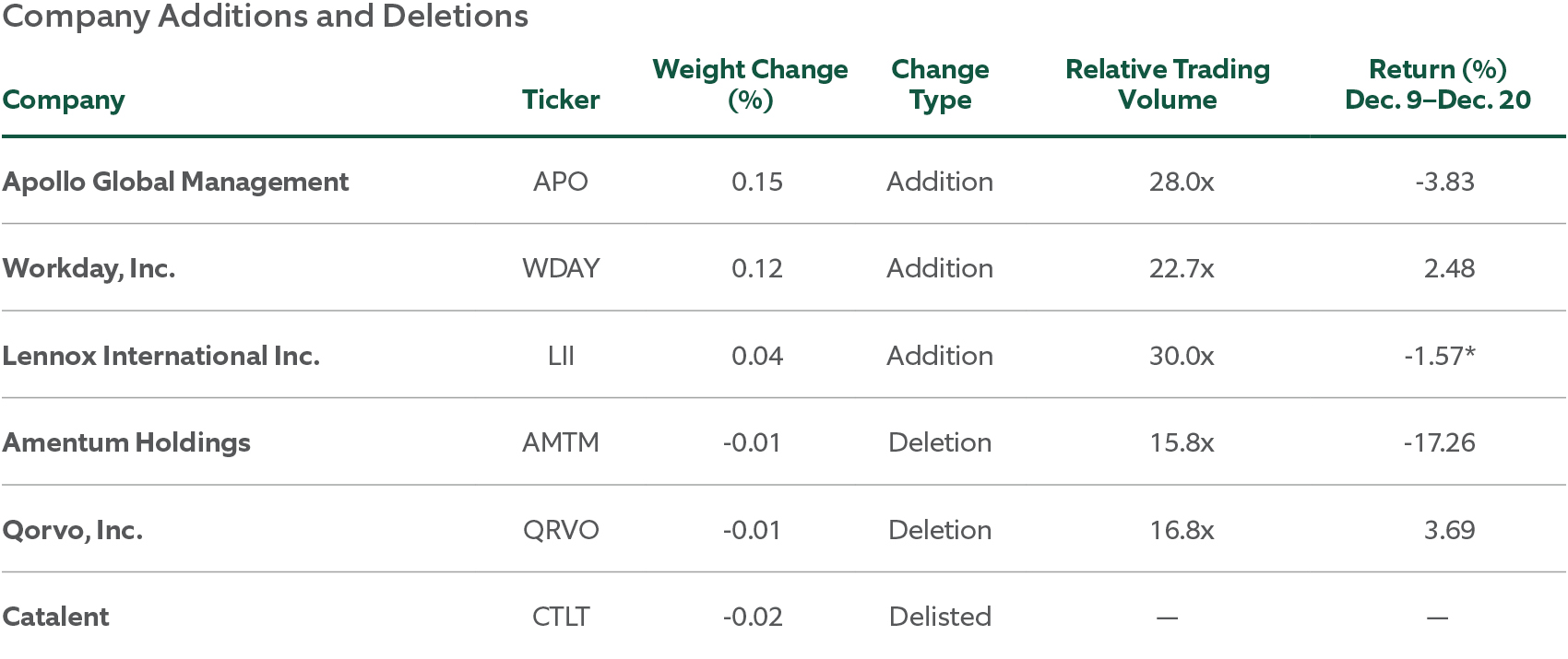

This quarter’s S&P 500 rebalance includes three additions to the index, while three stocks dropped out (see Exhibit 1). Apollo Global Management, an investment manager in the financial services industry, entered the index with a weighting of 0.15%. The second addition with an initial weight of 0.12%, is the cloud-based software application provider, Workday, Inc., part of the technology sector. This addition continues the trend of technology sector companies being added to the leading index in seven of the last eight quarterly rebalances, either through a direct addition or a migration up from the S&P MidCap 400 Index. The final addition is Lennox International, an industrial company that was a late inclusion in this rebalance event, replacing the healthcare company, Catalent, which was acquired by Novo Holdings in a deal that closed on December 18. The two other companies that moved down from the S&P 500 Index transitioned to the S&P SmallCap 600 Index: Amentum Holdings, an industrial company, and Qorvo Inc., a semiconductor solutions company.

A notable feature in the December rebalance is S&P’s annual growth and value reassignments for their style indexes. These adjustments generate additional flows as stocks transition between the style indexes, providing market participants with an important factor to consider as the index changes approach their effective date.

EXHIBIT 1: ADDITIONS LED BY FINANCIAL AND TECHNOLOGY COMPANIES

Apollo Global Management and Workday were added while Amentum and Qorvo were demoted. Lennox International replaced Catalent.

Source: Index data from S&P-Dow Jones as of December 6, 2024. Volume and performance data from FactSet and Bloomberg from December 6 to 20. Relative trading volume is the daily trading volume on December 20 versus the average 60-day daily trading before December 6. Index holdings are provided for information only and should not be construed as a recommendation of any security. It is not possible to invest directly in any index. Past performance is not indicative of future results. *The performance for Lennox International is the period from December 18 to 20.

Sector Impact: Financials Lead the Modest Changes

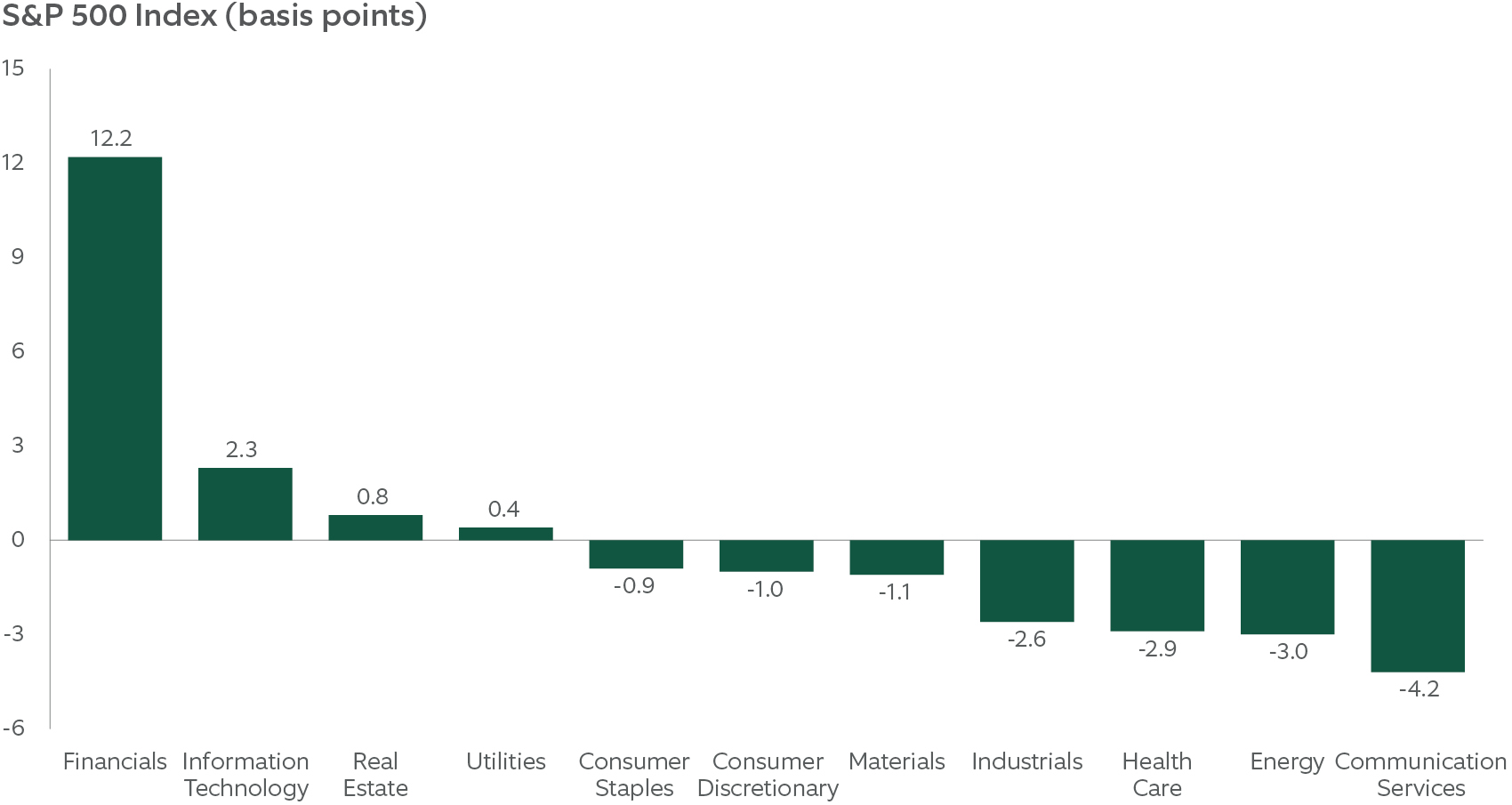

With the additions, deletions, and notable share changes that took effect, the sector composition of the index only marginally changed during this rebalance, as shown in Exhibit 2. Financials saw the largest bump, mainly driven by the addition of Apollo Global Management and a share increase of Visa, Inc., while communication services dropped the most as both Alphabet and Meta had modest share decreases that contributed to the majority of the decline in sector weight. The technology sector only rose a few basis points as the addition of Workday was partially offset by share decreases in giants Apple and Nvidia, and therefore small weight reductions in those names.

EXHIBIT 2: Sector Changes

Financials was clearly the largest sector weight change during this quarter’s rebalance.

Source: S&P-Dow Jones, as of December 9, 2024. It is not possible to invest directly in any index.

Performance Analysis: Mixed Performance

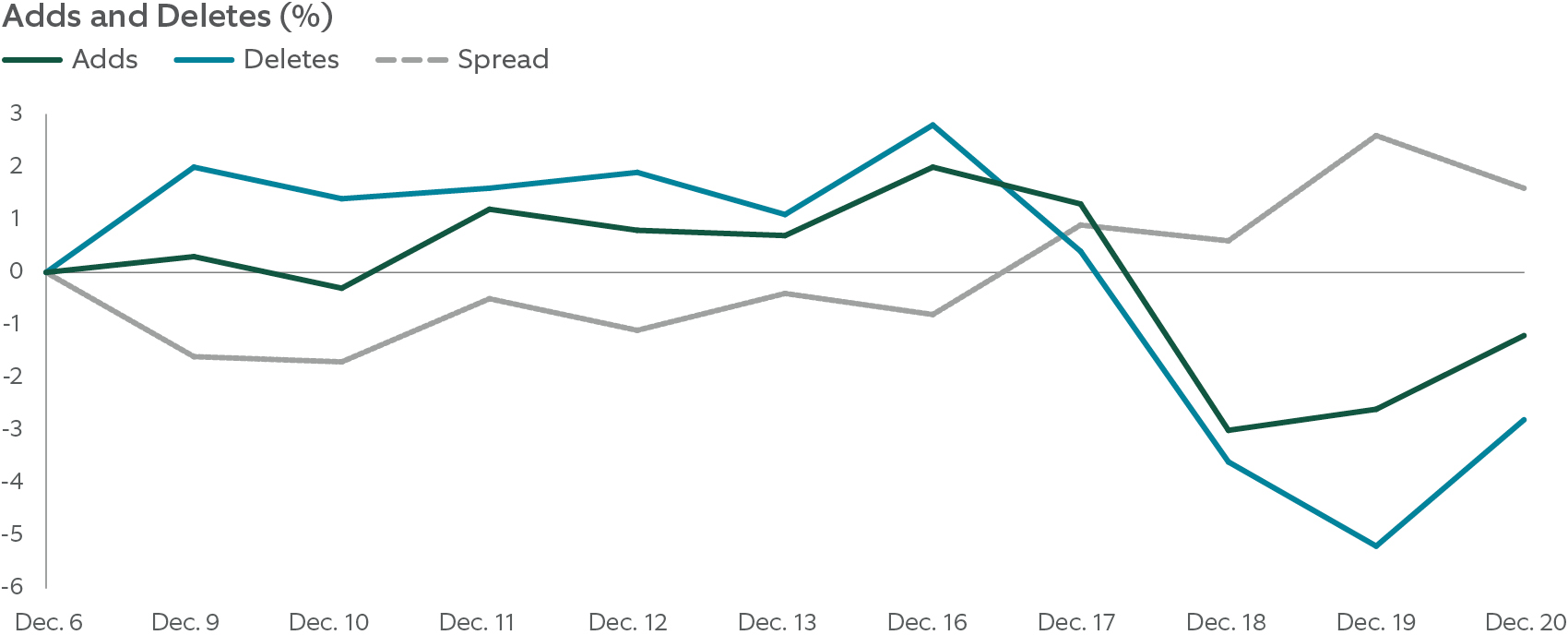

As expected, we observed substantial trading during the rebalance period from the announcement of the rebalance details to the effective date of the rebalance, peaking on the effective date. Index managers do most of their trading at or near the close of the effective date because their objective is to match the risk-return characteristics of the benchmark. However, because these rebalances are publicly known, other market participants will take on risk in an aim to profit from rebalance activity. Therefore, we often see stocks of added companies having “buy” pressure post-announcement and into the effective date, while deleted companies experience the opposite effect. The market impact of these flows can result in added stocks to outperform and removed stocks to underperform, though this doesn’t always hold true. If this expected pattern occurs, we describe the outperformance of companies as “right way,” aligning with the expected inflows (buys) and outflows (sells) of the indexes. We analyzed the extent to which performance aligned with the “right way” for adds and deletes in the index during the rebalance period.

The two additions included in the original announcement posted diverging performance on the first trading day following the index-change release on December 6. Challenging intuition and recent rebalance trends of stocks popping post announcement, Apollo Global Management actually sold off on December 9, returning -3.03%, while Workday was positive, returning 5.06% on that day. The aggregate performance of the additions and deletions only started trending “right way” as the rebalance period moved toward the effective date with a positive spread (adds minus deletes) emerging on December 17 as shown in Exhibit 3. This positive spread carried through the effective date, although the two deletes outperformed the additions on the effective date itself, leading to a “wrong way” finish on the final trading day. The performance analysis does not include Lennox International due to its late announced inclusion in this rebalance event after the market close on December 18.

EXHIBIT 3: PERFORMANCE OF THE S&P 500 REBALANCE

Both adds and deletes finished the rebalance period with cumulative negative returns; however, adds outperformed the dropped companies, leading to a positive spread since the index change announcement.

Source: S&P-Dow Jones, Factset, Northern Trust Asset Management. Review period is December 9 to 20, 2024. Past performance is not indicative or a guarantee of future results. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Indexes are the property of their respective owners, all rights reserved.

What the Rebalance Means to Investors and Index Managers

The December rebalance, which is inclusive of additions, deletions, share changes, and a late company swap, requires close examination and precise implementation. Given the amount of assets that track the S&P 500, trading volume increased significantly for the added and deleted companies, along with stocks with share changes.

Attentive analysis is crucial to understand how an impending index rebalance will shape the index, and by extension, the portfolios that track it. We believe this requires a careful review of liquidity conditions, expected trade flows, and optimal trade strategies. The aim for portfolio managers is to keep tracking error to a minimum while ensuring that the market impact and trading costs related to rebalancing do not erode wealth over time.

1 S&P Dow Jones Indices Annual Survey of Assets as of December 31, 2023.

2 Unless otherwise noted, rankings were published 6/10/2024 in Pensions & Investments magazine’s “2024 Special Report on the Largest Money Managers,” and are based on 12/31/2023 AUM. Rankings are calculated based on 411 investment management firms responding to P&I’s online questionnaire. To qualify for inclusion in the rankings, each firm must manage assets for U.S. institutional tax-exempt clients, such as qualified retirement plans, endowments or foundations, and answer the minimum required questions. Multi-Manager ranking appeared in “Special Report: Investment Outsourcing,” 7/11/2024 based on P&I data as of 3/31/2024. Past performance is not indicative of future results.

3 Through the market close on December 6, 2024; Bloomberg daily last price levels on SPX. Past performance is not indicative or a guarantee of future results. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Indexes are the property of their respective owners, all rights reserved.

IMPORTANT INFORMATION

Northern Trust Asset Management is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited, issued in the European Economic Association (“EEA”) by Northern Trust Fund Managers (Ireland) Limited, issued in Australia by Northern Trust Asset Management (Australia) Limited (ACN 648 476 019) which holds an Australian Financial Services Licence (License Number: 529895) and is regulated by the Australian Securities and Investments Commission (ASIC), and issued in Hong Kong by The Northern Trust Company of Hong Kong Limited which is regulated by the Hong Kong Securities and Futures Commission.

For Canada, Asia-Pacific (APAC) and Europe, Middle East and Africa (EMEA) markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. This information may not be edited, altered, revised, paraphrased, or otherwise modified without the prior written permission of NTAM. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. NTAM may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, its accuracy and completeness are not guaranteed, and is subject to change. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor.

This information is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on market or other conditions.

All securities investing and trading activities risk the loss of capital. Each portfolio is subject to substantial risks including market risks, strategy risks, advisor risk, and risks with respect to its investment in other structures. There can be no assurance that any portfolio investment objectives will be achieved, or that any investment will achieve profits or avoid incurring substantial losses. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Risk controls and models do not promise any level of performance or guarantee against loss of principal. Any discussion of risk management is intended to describe NTAM’s efforts to monitor and manage risk but does not imply low risk.

Past performance is not a guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by NTAM. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For U.S. NTI prospects or clients, please refer to Part 2a of the Form ADV or consult an NTI representative for additional information on fees.

Forward-looking statements and assumptions are NTAM’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information. Historical trends are not predictive of future results.

Not FDIC insured | May lose value | No bank guarantee