- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

What We're Worrying About

We identify four categories of risks to the growth outlook.

By Carl Tannenbaum

It is said that an economist is someone who can find a dark cloud behind any silver lining. Our discipline is known as the “dismal science.”

Those characterizations seem a bit unfair. We are often pushed into negativity by our employers: some of us are tasked with identifying potential downsides in the outlook and pitfalls associated with policies. Sometimes, we get paid to worry.

Please keep this background in mind as you read on. We filed a reasonably upbeat outlook for 2025 late last year, and nothing that has transpired since has changed our minds. But we have been getting an increasing number of questions about global risks that could change things for the worse. Following are the major long-run themes that we’re monitoring in this space, along with the ways in which they might manifest.

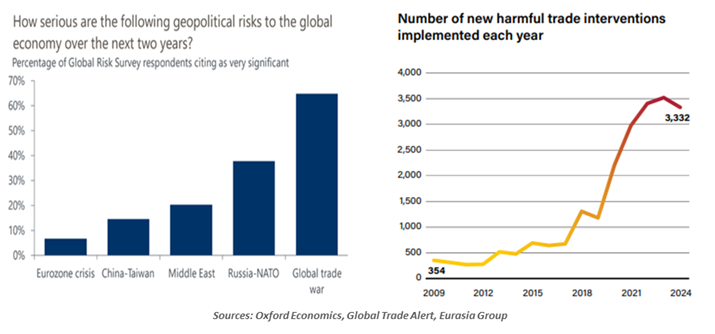

1. Diminished Global Cooperation

The willingness of nations to work together diplomatically has ebbed. The void in global leadership leaves space for regional conflicts and rogue actors to advance. (The Economist calls this a “deterrence deficit.”) International organizations and alliances have been weakened, hindering efforts to prevent and ameliorate tail events.

Conditions are therefore ripe for regional conflicts to arise and intensify. We see this today in the Middle East and Ukraine; other situations that are simmering today, like the stress between China and Taiwan, could boil over. Terror attacks, which marred the holiday period, could become more common.

Damage done by kinetic events and the use of sanctions to punish aggressors hinders economic activity. War and oppression can prompt refugees to flee their homes and seek asylum, bringing them to borders and shores which may not be fully welcoming.

A series of common concerns may be difficult to manage. International solutions to financial distress may be more difficult to arrange. Climate change will not be arrested without collaboration across countries. Fading support for the World Health Organization could make dealing with the next global health emergency extremely challenging.

As leading nations turn inward, it will become more difficult to head off tail events.

2. Trade Fragmentation

The incoming U.S. administration has threatened a range of trade actions. While some of these will be walked back, others will go through and prompt retaliation. Nations will be pressured to take sides in disputes between trading blocs.

The development of technology will proceed independently, not cooperatively. Different regional standards may emerge, reducing the fluidity of production and application. Supplies of critical commodities may be restricted, creating dislocations between raw materials and manufacturing centers. Global firms may find it more difficult to operate amid higher tariffs and national content requirements.

Nations and regions are very much focused on taking care of their own, using industrial policy to further domestic providers. The ability of emerging markets to develop could be hindered.

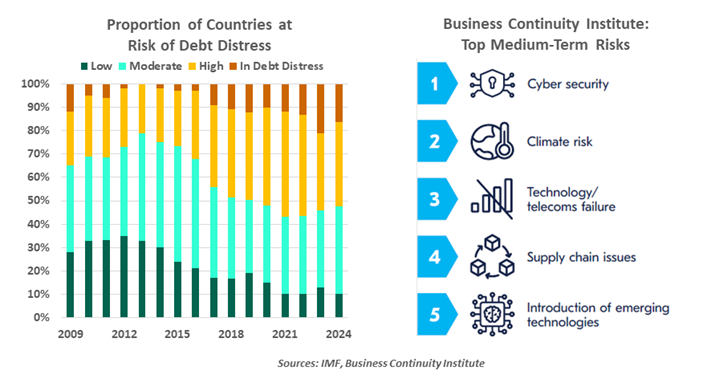

3. Fiscal Reckoning

Budget imbalances are growing in many countries and proving difficult for governments to deal with. This has fostered political instability and risks adverse market reactions.

In just the last two months, leaders in France, Germany, South Korea and Canada have been toppled (at least in part) because of squabbles over taxes and spending. Elections in these countries will be held in 2025; incumbent parties will struggle to hold power, but incoming regimes will have no better success in solving difficult budget equations.

China is dealing with a series of economic challenges, amid very high levels of public and private debt. The need for deleveraging diminishes the effectiveness of monetary stimulus, and the potential cost of demand-side measures has caused Chinese policy makers to hesitate. A deflationary hard landing remains a possibility.

Populations subject to austerity may react poorly. Civil disobedience and even violence may occur in some places. Investors may choose to move capital to more stable environments, creating volatility in currency and asset markets.

In the U.S., with the new Congress seated, work will begin on budget initiatives. The scale of proposed tax and spending changes is enormous; reconciling them (literally and figuratively) will strain fragile coalitions in Washington. Bond markets have sold off nervously during the past several weeks.

The line between good and ill is especially thin when it comes to AI.

4. The Politics of Technology

Digitalization is changing the way in which information is disseminated and used. The promise of improved productivity will be tempered by concerns over worker displacement and the use of artificial intelligence (AI) to mislead.

Countries and companies have little choice but to embrace AI: it offers hope of containing inflation, maintaining output and sustaining debt. But the potential for worker displacement will foment labor resistance. Work stoppages may become more common in the years ahead, and income inequality could grow.

Development will proceed rapidly in environments with the fewest restrictions, but this raises the risk that data will be misappropriated and misused. Cybercrime and espionage have reached new levels of sophistication and may progress faster than defenses designed to defeat them.

Information asymmetries have been widening, as social media allows participants to assemble and reinforce their own versions of the news. The potential for AI to create and disseminate misinformation could further the polarization of popular opinion. Policy consensus would become more difficult to achieve, and AI-driven propaganda efforts could upset legal and societal norms.

Finally, the digitalization of finance will give rise to product and market innovations that may be difficult to regulate. Systemic risk could rise, raising the possibility of another financial crisis.

Properly channeled, anxiety can help prepare for the worst and create plenty of space for positive surprises. But it can also become all-consuming, leading to over-analysis and risk aversion. We’ll try to strike the right balance as we cover these themes for you in the quarters ahead.

Now if you will excuse me, I need to spend some time in my happy place. If I could only remember where that is…

Related Articles

Read Past Articles

Meet Our Team

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)

Carl R. Tannenbaum

Chief Economist

Ryan James Boyle

Chief U.S. Economist

Vaibhav Tandon

Chief International Economist

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.