- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

The Weekender

Weekly perspectives from Gary Paulin, Head of International Enterprise Client Solutions, on global market developments and their potential broader implications

March 22, 2025

SUPERCYCLES AND A SENSIBLE SECRETARY

The Austrian Economists have left

It appears that economists of the Austrian School have left for the US and Argentina. They’ve been replaced by neo-Keynesians under the guise of rearmament, or what we call Military Keynesianism, the new general of which is Mario Draghi, former Italian Prime Minister and President of the ECB.

This is not simply about military defences. It’s broader, as it provides cover for investment in European infrastructure and competitiveness a la the Drahi Plan. What’s occurring in Europe, and the speed that it’s happening with is staggering for long-suffering observers (like me) of the Eurocracy’s decision-making, which until recently has seen glaciers move faster.

Trump, it seems, has done in weeks what took Charlemagne decades: to unify the Europeans. Proposals to lift defence spending at the EU level, joint procurement efforts, and issuing common bonds dovetail with the enormity of Germany’s announcement. This is one of those moments that we'll reflect on in future, like the end of WW2 or the fall of the Berlin Wall.

It matters for many things – not least asset allocation. We have fiscal expansion in Europe at a time the US is deleveraging. And yes, it will take time for large allocators to react, but whereas Europe once only had tourists, it now has tanks. And soon, maybe (more) inflows.

Closing the diversification deficit

We talked a lot last year of the diversification deficit likely to emerge once AI sobriety kicked-in. We talked of a new regime, new regions (UK/EU/China), new assets (Dividends vs PE) and of buying insurance before they needed it. We also talked about commodities. I wish we hadn’t! With the rare exception of gold (which has now outperformed the S&P over five years), silver, copper, cocoa, and coffee (all up over 20%), the broader index (BCOM) was muted, up only 6% the past 12 months. Let’s call that a failure.

That said, the demand drivers we cited last year look even stronger now (see above: state largesse in Europe!). And of course, as any self-respecting capital cyclist will tell you, it’s supply that drives returns, not demand.

But as it’s demand that drives the narrative, and given I’m no analyst, let me tell you a story. A story about ‘supercycles’.

Commodity credentials

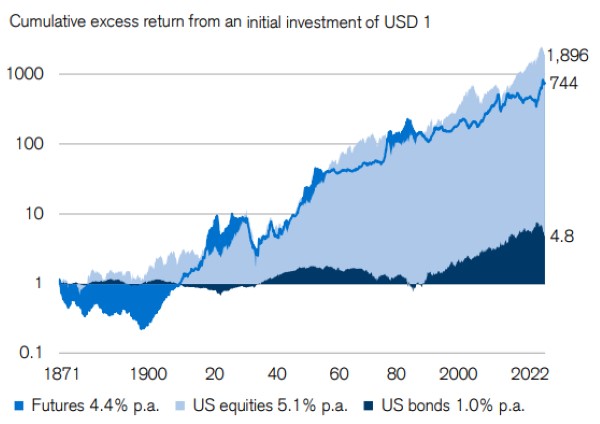

So, I thought that a supercycle for commodities was starting last year. I was early (AKA wrong). But I’m even more convinced now (AKA deluded?) But first, let’s start with their credentials. As a diversifier, commodities do well. Historically they have a low correlation with equities, a negative correlation with bonds, and provide a hedge against inflation volatility – which we suspect will hang around for a while yet (see Arnott and Shakernia for reasons why).

The necessary conditions for supercycles to emerge tend to require years of underinvestment (check), extreme bearishness/low allocations (check) and either a global economic shift, rearmament or reconstruction (check, check and check). While a dollar invested in commodities may not have delivered the excess returns like equities have, they are still pretty good.

Great, in fact, during periods of inflation.

Source: The Global Investment Returns Yearbook.

Supercycle

Now, as you know, commodity prices move in long, sweeping cycles of boom and bust, hence the term ‘supercycles’. The last one, after China entered the WTO, ended in 2012, since when the sector’s suffered from chronic underinvestment, capital constraint, nimbyism and ESG. We now have ‘national security’ trumping ESG and nimbyism. We have rearmament in Europe and Japan, reconstruction hopefully to come in Ukraine, and reshoring in the US. All are commodity-intensive endeavors.

So too is energy transition (the largest construction project on the planet), space activity (the largest outside the planet), AI capex and it seems even China – the largest consumer of commodities – is showing signs of recovery. More about her in a second...

Scarcity

But my favourite narrative remains that of Scarcity (with a little mean reversion thrown in for measure). You may remember last year we wrote of the mean-reversion potential of the transition from the ‘ethereal’ world (that of ideas/IP) to the material world (things). It was a disaster of a call (for now, mea culpa). Our premise was that scarcity – and therefore value – for technology lies not solely in IP but in the supply chain, the ‘material world’, that underlies it.

As Ed Conway illustrated in his must read, Material World, this ‘world’ is mission-critical to our tech-promised future, perhaps more now than ever. As we said at the time: “...without sand, no silicon. No silicon no glass, no covid vaccines, no iPhone. No silver no solar. No salt, no sanitation, no drinking water. No copper, no electricity”. More pressing today: no titanium, (a coincidence that Ukraine holds a fifth of the world’s reserves?), no F35 fighter jets. No niobium, no missiles, no rockets, no winning the space race.

My question is: what does Trump see (in Ukraine, Greenland, Canada, Panama and DRC) that the market cannot? Answer: rare, yet critical materials. While governments clearly see value and prepared to pursue these rare minerals, I can still find exposures on single digit PEs with huge dividends in regions that are mostly ignored. I suspect Kiril Sokoloff’s observation still holds, that: “...you could buy the top 100 miners, three years of copper production and all seaborne iron-ore with the market cap of Nvidia”.

America’s proposed Sovereign Wealth Fund should take note!

China recovering?

As discussed already, don’t fight the command of a command economy. If China wants stocks up, she will probably get her way. It’s often as simple as that. And does she (want stocks up)? Yes. And property prices. Why? Because they represent system collateral. If your end game is to raise domestic consumption, then fixing the housing market will fix collateral, confidence and ultimately consumption. It may unlock the enormous savings potential, estimated to be c40% of GDP (with arguably post-Covid revenge spending still to come in China!).

If this sounds familiar, it was the playbook the US used to recover after the GFC. The most important signal to watch, therefore, is Chinese property data, which has stabilised, as has its market proxy, the SHProp Index. Should this now start to rally, I suspect it will inspire even greater confidence in the broader equity market. And commodities. Why? It’s their biggest market.

Should old correlations hold again?

Seeing as we are on the topic of mean reversion, a reminder of where things stood for gold (and silver) historically. Yes, gold has made new all-time highs, but should it get back to the market value of US official gold to 1989 levels relative to foreign-held USTs, it would need to at least double again. With regards to silver, the gold-to-silver ratio has averaged about 60x since the 1970s. It’s now at 90x, a historically high. What if old correlations hold? Got gold? Got commodities?

The calming influence of Scott Bessent

If you listen to one podcast this week, listen to this interview with Scott Bessent, US Secretary of the Treasury. He’s self-assured, thoughtful and having been in markets for over three decades, fully conversant with what drives economic prosperity, which in the US includes stock markets. So, despite his apparent focus on Main Street, where interest rates and gasoline prices matter most, I doubt he’s giving up on Wall St. Why? Because the top 10% of earners account for 50% of consumption. And until recently they held record amounts of US stocks.

Meaning? Any wealth shock (from falling stocks) could impact consumption and by extension GDP, turning what is currently a correction into something more severe. A bear market. And no one wants that, not even Trump.

Public sector deleveraging - private sector releveraging

Bessent urges that we shouldn’t focus solely on DoGE and public sector deleveraging as being independent but as linked to 'releveraging' the private sector. While the market seems obsessed by the cuts, it could be overlooking potential benefits. Get spending down, then inflation and rates may follow - which should further lower spending, given interest expense is enormous. And while this is happening, he expects the private sector to releverage; re-shoring could help drive up real wages, deregulation of small/community banks could improve liquidity provision to Main St; so too could tax cuts.

He admits however that things might be volatile as the baton changes hand, which is why in a subsequent Bloomberg article he “expressed an urgency to move on to tax cuts and regulation rollbacks”. But when someone of his experience and with his understanding of macro suggests he’s not worried about markets, then, I’m not sure we should be either.

This all sounds quite promising for fans of order, predictability and profit.

Bond demand and compounding

While Bessent endorses Fed independence, he does think they’re being too harsh on small banks. Were they, for example, to remove the capital charge applied to banks for buying T bills, demand for such would increase and yields would come down “by 30 to 70 bps”, “where every basis point is a billion dollars a year in savings”.

And while talking of incremental T-Bill demand, he mentioned he had just come from the Crypto Committee meeting. No doubt the Strategic Reserve was discussed, but I wonder if they talked about stablecoins, which as David Sachs has suggested, could be a significant buyer of USTs. Indeed, Tether was the 7th largest buyer of treasuries last year. Just behind the UK. True Story.

And for those following Brad Gerstner’s initiative to give every new-born an investment account to benefit from the powers of compounding, Bessent seemed to endorse the idea of what he called baby bonds. Trump, he said, “wants to leave Americans assets” not liabilities. This is something that I still think the UK (where I live) should implement. After all, they originated the idea.

Receive The Weekender

Register your interest in receiving Gary's commentary direct to your inbox.

Gary Paulin

Head of International Enterprise Client Solutions

NEITHER THE INFORMATION NOR ANY VIEWS EXPRESSED CONSTITUTES INVESTMENT ADVICE AND IT DOES NOT TAKE INTO ACCOUNT THE SPECIFIC INVESTMENT OBJECTIVES, FINANCIAL SITUATION AND THE PARTICULAR NEEDS OF ANY SPECIFIC PERSON WHO MAY VIEW THIS MATERIAL.

These are my own personal views, not those of my employer. This report is not intended for retail customers. Any further disclosure, use, distribution, dissemination or copying of this report or any of the information herein is strictly prohibited. The information in this report has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Any opinions expressed herein are subject to change at any time without notice. Any person relying upon information in this report shall be solely responsible for the consequences of such reliance. This report is provided for informational purposes only and does not constitute legal, tax or other advice nor does it constitute an offer or solicitation to purchase or sell any security, commodity, currency or other product. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining advice from their own advisors. Internet communications are susceptible to alteration and Northern Trust shall not be liable for the message if it has been altered, changed or falsified.

Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.