- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

The Weekender

Fortnightly perspectives from Gary Paulin, Head of International Enterprise Client Solutions, on global market developments and their potential broader implications

February 08, 2025

UNCERTAINTY

The vibe

I’ve recently returned from an allocator conference in Miami where I experienced firsthand the ebullient vibe of many US investors, especially those involved with technology. At breakfast on Monday, DeepSeek momentarily soured the mood, but it quickly returned thanks to conference revisiting the teachings of nineteenth century economist, William Jevon and his paradox (that efficiency improvements can lead to increased overall consumption).

Thus by lunchtime most participants were convinced that demand for compute would increase exponentially. Cheaper intelligence means value transfers from infrastructure to applications and areas downstream of technology, like the consumer. Now AI was potentially the largest positive total factor productivity shock in the history of the world. Those who don’t use will surely end up on the wrong side of history...

Sputnik

By tea-time Wednesday the unveiling of DeepSeek was considered America’s Sputnik moment, one that will shatter residue complacency, unlock further innovation and drive US growth north of 5%. Excellence requires adversary after all. By supper, discussions around DoGE (which several speakers were involved with) had all but guaranteed a balanced budget. Add deficit reduction + deregulation to lower debt issuance, new UST demand from stablecoins and the possibility of a debt jubilee by revaluing US gold reserves (a topic we discussed last year) and the 10Y’s was seen heading to 3-handle, re-rating future cashflows and sending us “off to the races”. By the time dessert arrived, I was drunk on positivity.

But as I clumsily searched my mobile to remove my US equity hedge, I met Howard Marks. And quickly sobered up.

I don’t know

They say: never meet your heroes, unless it is Howard Marks. He’s my investment animal-spirit, my mental benchmark in decision making: what would Howard say? When asked his views on tariffs, on DeepSeek and Trump’s likely reaction function, he replied “I don’t know”.

Of course, he’s not an equity investor, a tech-expert nor geopolitician. But he understands human psychology. And what’s hidden in his seemingly innocuous answer is the idea of ‘uncertainty’. A creeping unease, that if shared by others could lead to inaction, weigh on valuations and put pause to asset price appreciation.

Perhaps we should discount, even ignore it? He’s a credit investor after all...

In times of uncertainty, constants re-rate

Now, credit investors thrive on uncertainty, for constants – like contractual returns – should gain ascendancy (I’m still of the view that after having 4 down years for USTs, we won’t have a 5th). But there was something unnerving about his comment. We don’t yet know if tariffs are tactics as (as Scott Bessent proclaims), or more a permanent feature (like those of in President McKinley’s tenure)?

We don’t yet know if DeepSeek will unlock more innovation or cause more constraint? Might the internet balkanise? Will hyperscalers ever generate a RoI from their enormous capex? I. just. don’t. know.

Robyn Grew, CEO of Man said it best: "there is no doubt it is an exciting time for the US and our jobs…. "It's just not an easy time." Quite.

Animal signs and spirits

However, I did learn a few things about animals that gave me comfort. You’ll all know it’s the Year of the Snake in China. You might not know President Xi was born in the Year of the Snake, suggesting 2025 could be good for him (and China).

What’s more, snakes like dogs. In fact, snakes and dogs are surprisingly well-matched, with good potential for harmony, long-lasting relationships, even romance (says Google). So what? Well, Trump was born in the Year of the Dog!

Who wins most from cheaper intelligence?

Might this explain the change of heart since Chinese New Year: the softer and more tempered approach (than some expected) on tariffs, and more open communication. Could the biggest surprise of ‘25 be an improvement in US-China relations? And if so, which market benefits most? The US? China? Or maybe Germany or even the UK?

For if intelligence just got a lot cheaper it’s worth pondering what happens to older or more traditional industries that haven’t yet experienced the positive shock of AI.

Industries which are prevalent in Britain. Just saying.

Seals wearing headphones

One emerging consensus was America’s potential will only be reached by removing obstacles to growth. The most pressing obstacle? Regulation. Elon Musk faced launch delays on SpaceX rockets until he’d satisfied certain interest groups that a sonic boom would cause little distress to seals swimming nearby. To prove it, he kidnaped seals, fitted them with headphones and measured their distress levels to simulated rocket sounds.

Similar delays were faced by the UK’s former prime minister Boris Johnson when seeking approval to expand his swimming pool. The presence of newts required him to ensure their safety, forcing him to do ‘whatever it takes’ to protect them and build a "Newtopia". Only then was permission granted. And in California, Hotels must have signs next to pools urging people with active diarrhoea not to bathe.

One rule I agree with, and proof that some regulations are worthwhile.

Staying short compliance officers

But humour aside, there is a dramatic shift unfolding. Britain’s Reeves says growth comes before ideology. Brits now say growth comes before net-zero (good news North Sea drilling?) and more Americans think the government does too much, than too little. I feel this is a profound shift, and if productivity is a function of both carrot and stock, the stick looks likely to be removed. Good news for growth.

But as we’ve discussed previously, may be bad news for compliance officers. And seals.

Going global

And it’s not just America. New Zealand has a dedicated ‘Regulations team’, the opposition conservative party in Australia is campaigning on cutting red tape (and taxes) and Argentina’s Milei himself – the influencer of most influence – has identified 2,600 of 3,200 rules to chainsaw. India is pursuing ‘process reforms’ to streamline government, left-leaning governments like the UK want to overhaul planning laws, the French – who invented the word – are seeking “a strong movement of de-bureaucratisation” while their overlords, the European Commission (EC) have pledged to cut corporate reporting by 35% for small firms.

Indeed, the President of the ECB and president of the EC recently stated they are ready to do “whatever is necessary to bring Europe back on track”.

Read that sentence again. Even Europe wants to become more competitive. This is change.

Memories with uncorrelated returns

As an alternative asset class there is a lot to like in sport investing. It offers scarcity value, durability and seems quite recession proof. Memories are priceless. So too is community. In a world that often looks as if it’s tearing itself apart, sport brings people together. It’s one of the few formats where live entertainment has a media tailwind and broad adjacencies. Areas of interest include female sports, cricket (think India) and youth (see Unrivalled Sports).

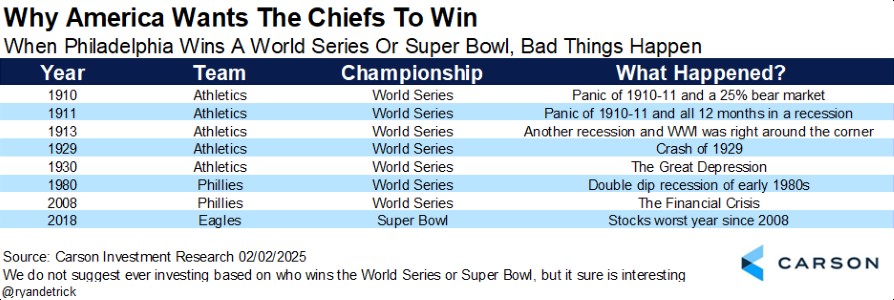

It can make millions of people happy (and very sad) and is seemingly non-correlated to equity returns. That is, unless Philadelphia wins the Super Bowl (see below).

Go Chiefs!

Source: Carson

In other news

Trump Media and Technology Group announced it’s expanding into financial services and looking into creating ETFs to invest in what it calls the "Patriot Economy," focusing on American manufacturing, energy, and growth companies. Meanwhile, Trump’s newly-proposed Sovereign Wealth Fund has sparked speculation about the inclusion of crypto, while son Eric’s been busy buying Ethereum just as Elon Musk wants to put the U.S. Treasury on the blockchain.

Finally, it’s noteworthy that disruptor Vanguard has slashed prices on several index funds. Here’s hoping Jevon’s Paradox will apply, and a lower cost simply increases demand for all funds.

Receive The Weekender

Register your interest in receiving Gary's commentary direct to your inbox.

Gary Paulin

Head of International Enterprise Client Solutions

NEITHER THE INFORMATION NOR ANY VIEWS EXPRESSED CONSTITUTES INVESTMENT ADVICE AND IT DOES NOT TAKE INTO ACCOUNT THE SPECIFIC INVESTMENT OBJECTIVES, FINANCIAL SITUATION AND THE PARTICULAR NEEDS OF ANY SPECIFIC PERSON WHO MAY VIEW THIS MATERIAL.

These are my own personal views, not those of my employer. This report is not intended for retail customers. Any further disclosure, use, distribution, dissemination or copying of this report or any of the information herein is strictly prohibited. The information in this report has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Any opinions expressed herein are subject to change at any time without notice. Any person relying upon information in this report shall be solely responsible for the consequences of such reliance. This report is provided for informational purposes only and does not constitute legal, tax or other advice nor does it constitute an offer or solicitation to purchase or sell any security, commodity, currency or other product. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining advice from their own advisors. Internet communications are susceptible to alteration and Northern Trust shall not be liable for the message if it has been altered, changed or falsified.

Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.