- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

The Weekender

Weekly perspectives from Gary Paulin, Head of International Enterprise Client Solutions, on global market developments and their potential broader implications

September 28, 2024

WHAT A COMEBACK

The nature of comebacks

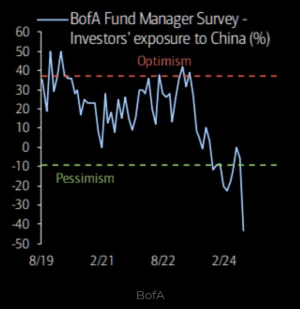

For some time we’ve discussed what new narratives could emerge post-Fed easing and how allocators are thinking about positioning for such. One such narrative was the comeback potential of China and relatedly, commodities. Sentiment was as bad as I can remember on China and was at seven-year lows with regards to commodities (per FMS). Most analysts had capitulated – many managers have dropped China from their EM funds (see ABDRN just last week) and anything that once touted Chinese exposure, was being trousered – think luxury, wines & spirits, iron-ore, Starbucks, Nike, Estee Lauder, etc. As a consequence, exposures were so low and fears so high that China, and indeed EM generally were off-radar for most global investors, such that EM vs US valuations fell to all-time lows. But as Ruchir Sharma in the FT said recently, “that is the nature of comebacks”. “They emerge from obscurity, and the deeper the shadows from which they spring, the more drama surrounds the comeback — once it is recognised’.

And things got pretty deep in China...

Source: Global Allocators

And boy, did we get some drama.

With more to come I suspect.

“When policy panics, markets rally” – Ed Yardeni

Is China panicking?

While the scale and degree of coordination is noteworthy, it’s the timing which stands out. We were expecting China to wait until after the Fed in fear of adding pressure to their currency, but few were expecting anything in September. The Politburo typically devotes its April, July, and December sessions for the economy. September is reserved for other issues, so an ad-hoc discussion of the economy suggests the top brass are worried. Worried enough to send in the cavalry with a flag-bearer embossed with ‘whatever it takes', employing tactics we’ve seen in other successful battles, namely the US vs GFC 2009. Slashing the cost of money, expanding the balance sheet, recapitalising banks, direct cash handouts! and QE for housing and stock buy-backs while stating ‘price recovery’ (i.e. reflation) as the north-star for policy.

It’s weeks like this you are reminded why macro investors and analysts spend so much more time on China than India. While India remains a potentially great investment, China matters. To everything. Even Mrs. Paulin’s ISA.

The Bannister Effect

My friend Bill Callanan from Syzygy is my ‘go-to’ for all things China and the only remaining bull I could find on the Street (unlike a few others, like me, who talk positively on China, go quiet for months/years and claim commitment once it turns). He talks about the Fed’s latest move as the monetary version of the “Bannister Effect”, a reference to the number of runners who broke the 4-minute mile, 4, the year after Roger Bannister first accomplished the feat in 1954.

And while the US may not be facing a recession, it’s bigger challenge could be having a higher expense bill for interest costs than defence spending – a scenario not seen in more than six decades – and one, if it continued, might end quite poorly (see Habsburg Spain, the Ottoman and British Empires for clues). Cutting rates might be a better option than cutting entitlements? And so, it seems, a global easing cycle (sans Japan and Brazil of course) is under way, and the pace-setter, the US, has just been passed by the Chinese in a comeback that mirrors Dave Wottle in 1972 Olympic 800m final. See here, it’s gold (more on that fine metal in a second). Or maybe FXI which tracks the FTSE China 50 Index, having been down -12% in Q1, it’s staged a stunning comeback and is now running first in the stakes for major equity markets YTD. Even eclipsing the S&P, up 25% (at time of writing).

Pulling on a string

A crisis of confidence is more often a crisis of collateral. Meaning: if you fix collateral, you will fix confidence and maybe even consumption. And it’s not like the Chinese don’t have any money. They do, trillions of it. Roughly 40% of GDP is currently stuffed under the mattress with lots more overseas which may now be enticed home should the Yuan and/or collateral values rise. Which they now might, given all the measures aimed at lifting stock prices, and critically, property (which accounts for the greatest % of wealth). With regard to stocks, not only are SoE’s incentivized to get stock prices up, they are being offered cheap loans to do so – via buybacks. Assuming they pay higher dividends than the loan interest costs, such will be accretive, it will lock in a positive carry and provide a free option on upside and a clear path to appeasement (given stock prices are now KPIs). And the banks don’t mind lending against this asset for they know in doing so supply will fall and price should rise. This is not the monetary policy version of pushing on a string. This string is being pulled. And with regard to property, where similar re-lending packages exist for housing buybacks, and where banks are prepared to cough-up all the funds (i.e. 100% LTV) then, should rental yields surpass interest costs, well, this string becomes a rope – one that lifts the anchor.

And off we sail...

Asymmetric Beta

Despite the interest in EM-ex China Indices, if you’re minded to take more active share in the region, don’t use derivatives and are benchmark aware, then the idea of asymmetric beta as discussed by Northern Trust Asset Management’s Michael Hunstad might appeal? In this article he argues it’s possible to skew a portfolio towards higher quality stocks without increasing tracking error and giving you lower beta on the downside. Meaning, it is possible to outperform while cutting your tail risk. And if you speak to him, ask him to explain why ‘quality’, and increasingly ‘dividend’ are factors you need to consider more in your allocation models, especially in China where those high dividend payers will see yields compound as the PBOC provides cheap funding for buy-backs. For some, it will be hard to get over Xi’s ideological constraints but I do wonder whether tensions between the US and China may diffuse somewhat if we were to get a peace deal in Ukraine. Something Donald Trump seems pretty keen on.

The pain trade is higher

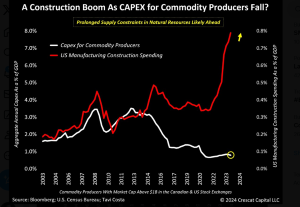

Needless it is to say – and many others will – that a permissive Fed, a reflating China, a weakening USD, lower oil prices (see below) and consequent improving global liquidity at a time of low inventories and chronic under-investment, present all the hall-markets of a structural bull-market for commodities. Pick your poison from Chile’s copper production (the world’s largest) remaining at the same level it was 12 years ago or the fact mining capex has actually fallen in the US despite the beginning of the largest construction projects the world’s ever seen: decarbonisation + deglobalisation. Copper recently stopped going down on bad news (i.e. China), Australian and Canadian currencies looked poised for higher honors and per Michael Hartnett at BoAML, investors are the most underweight commodities since June 2017.

The pain trade in other words is higher. With one exception. Oil.

Source: Crescat Capital, Tavi Costa

Oil: down on good news

After seeing the Chinese headlines on Thursday and having watched with some excitement the move in commodity related stocks, I was staggered to see oil prices not react. They actually fell. Normally, when the world’s largest consumer says they are about to unleash unprecedented amounts of stimulus to juice consumption, prices would rise? What gives? Well, Saudi gives. Or rather has given-up on their $100 crude target in what appears a pivot towards regaining market share. When they did something similar back in June of 2014, a strategy aimed at US Shale, oil prices halved over the following 18 months. Great news for global liquidity. Not so for oil stocks.

The other BIG event gone unnoticed

The other big thing that happened this week was Japan appointed 67 year old Shigeru Ishiba to be their next leader. He is known for his hawkish views on both monetary policy (see Yen rally) and defence and even campaigned as an advocate of an “Asian NATO” – an idea that risks flaming tensions with China. Interestingly though, the Americans say they have no intent on such and Biden’s even tried to veto Nippon Steel’s bid for US Steel on ‘security grounds’. What these issues are, is unclear but I suspect the reasons might be more political, than geo-political. Apparently they have elections soon.

Rising liquidity: bitcoin or gold?

I have a chart on Bloomberg which acts as a proxy for global liquidity. It’s just made a new all-time high. And, given what’s discussed above, I suspect there’s more to come. So, what assets do well in such an environment? Small-caps, gold, real estate, commodities and EM, I hear you say.

All true. But the highest asset correlation is bitcoin. According to this report by the brilliant Lyn Alden, bitcoin moves in the direction of global liquidity 83% of the time in any given 12-month period, which is higher than any other major asset class. I own some bitcoin and can see why improving liquidity enhances its appeal: it’s a supply-constrained store of value. But so too is gold. And should gold digitize, as is the World Gold Council’s intent, and assume attributes of divisibility and portability, what role is left for bitcoin?

As an aside, one aspect of gold I’ve heard little about is its potential to be reclassified as a High Quality Liquid Asset (HQLA). This could change its financial utility, from being solely a reserve asset to a form of lending collateral, and expand its appeal from central banks to all banks.

Mrs. Paulin would like to see that, as well.

Receive The Weekender

Register your interest in receiving Gary's commentary direct to your inbox.

Gary Paulin

Head of International Enterprise Client Solutions

NEITHER THE INFORMATION NOR ANY VIEWS EXPRESSED CONSTITUTES INVESTMENT ADVICE AND IT DOES NOT TAKE INTO ACCOUNT THE SPECIFIC INVESTMENT OBJECTIVES, FINANCIAL SITUATION AND THE PARTICULAR NEEDS OF ANY SPECIFIC PERSON WHO MAY VIEW THIS MATERIAL.

These are my own personal views, not those of my employer. This report is not intended for retail customers. Any further disclosure, use, distribution, dissemination or copying of this report or any of the information herein is strictly prohibited. The information in this report has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Any opinions expressed herein are subject to change at any time without notice. Any person relying upon information in this report shall be solely responsible for the consequences of such reliance. This report is provided for informational purposes only and does not constitute legal, tax or other advice nor does it constitute an offer or solicitation to purchase or sell any security, commodity, currency or other product. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining advice from their own advisors. Internet communications are susceptible to alteration and Northern Trust shall not be liable for the message if it has been altered, changed or falsified.

Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.