COVER STORY

To a logician, a false dichotomy is a fallacy that implies that there are only two possible answers to a single question: Left or right? Up or down? Here or there?

On the short list of false choices, “None of the above” is not an option. But in the real world of investment choices, answers are rarely so black or white.

A key question faced by shareholders is whether active or passive management might generate better risk-adjusted returns over time. The argument is academic and relevant, controversial and polarizing.

Active managers, of course, seek to outperform a market benchmark through astute stock or bond selection. At the opposite end of the spectrum, passive managers try to match a market benchmark (less operating expenses) by owning all or a representative sample of the securities comprising it.

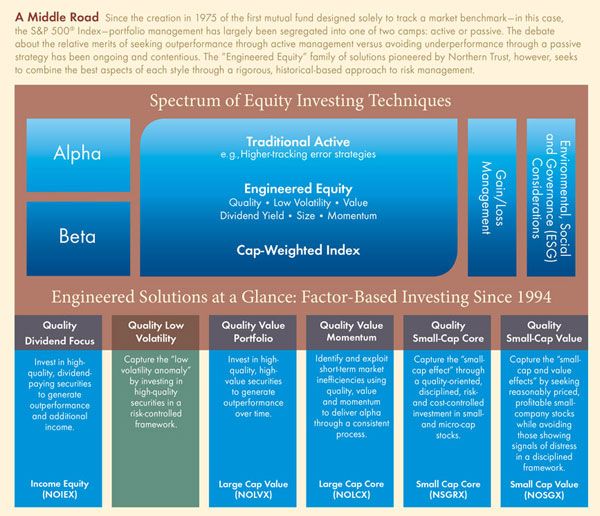

A middle ground

There are sound reasons for selecting either—or both—of those strategies. But that doesn’t mean that there isn’t a middle ground, a third option, one whose complimentary methodology ideally combines favorable aspects of both styles.

“Having to choose between active and passive management oversimplifies a complex and individualistic set of factors,” said Matt Peron, senior vice president and managing director of global equity at Northern Trust Asset Management. “It doesn’t have to be an ‘either/or’ decision. Active and passive strategies can complement one another.”

Indeed, claiming a middle ground between active and passive could be justified by evidence and theory. “We believe that there is a way to combine the two strategies that borrows from some of the potential advantages of each,” Peron said.

In a nutshell, the main advantage of active management lies in the ability to weed out holdings that the manager believes are less likely to outperform over time. Passive management can offer investors lower operating costs, as well as the risk-diffusing benefits of maximum diversification.

“There are strong points to both the active and passive styles,” said Peron. “So we set out to identify strategies that could combine the best characteristics of each.”

Timely debate

The goal of linking potentially favorable aspects of the active and passive styles could be especially important now, as memories of the global credit crunch and Great Recession remain disturbingly fresh. Dampening volatility, generating income, boosting diversification and enhancing transparency have assumed greater importance to investors in the post-crisis world, especially for those in or approaching retirement age.

According to Peron, investors in active management strategies are seeking greater consistency and value from whatever outperformance their holdings generate. “They want to know whether the relative performance of their funds merits the risks undertaken by straying from a market benchmark,” he said.

Such concerns are understandable and, perhaps, overdue.

For example, an active manager overweighting the high-flying high-tech sector in the late 1990s would have subjected shareholders to a hyperbolic ride—and almost certainly extreme underperformance when the dot-com bubble burst.

“Having to choose between active and passive management oversimplifies a complex and individualistic set of factors.”

Matt Peron, senior vice president and managing director of global equity for Northern Trust Asset Management

Though skilled managers still can find pricing inefficiencies to exploit, more than three-quarters of actively managed mutual funds nonetheless lagged their respective benchmarks during the five years through June 20141 .

Meanwhile, the passive approach of investing in capitalization-weighted indexes is being put under the microscope as well. That’s because just matching a benchmark amid a severe downturn like the one that struck global equity markets in 2008 may be considered something of a Pyrrhic victory, or one that’s been achieved only after suffering heavy losses.

“Dampening volatility during turbulent economic times potentially could take some of the sting out of a bear market,” noted Peron. “But the key to making that happen is to understand which risks are worth taking and which ones are not.”

Expertise or good fortune?

One component of the active versus passive argument involves determining how much outperformance should be attributed to managerial skill and how much derived from just being in the right place at the right time.

Or, to adapt a well-known aphorism: What portion of an active manager’s success should be attributed to just showing up?

Importantly, performance numbers can be viewed in terms of how much risk the manager took to attain them.

“It’s really a question of whether the magnitude of any outperformance adequately compensated investors for any extra risk the manager took to get it,” said Peron, who added that most risk factors are both identifiable and quantifiable.

Risk factors

The process of identifying and quantifying those factors led Peron and his research team to dig deep into the history books. That quest began, however, with an irrefutable fact of investing life.

“There is a relationship between risk and reward,” Peron acknowledged, adding that returns from the only risk-free asset class, U.S. Treasury Bills, would have fallen far behind those on stocks and bonds over most long periods.

Still, Peron noted that the historical relationship between risk and reward is not necessarily symmetrical or proportional.

In poring over reams of historical data, Peron and his researchers determined that the risk-adjusted returns of most actively managed funds are closely related to the biases that typically make up their security selection process.

Those biases, or risk factors, include market capitalization, relative valuation, price momentum and dividend yield. Peron said that while some risks are worth taking, others can and should be avoided, depending on personal preferences.

“We recognize that each investor has unique goals, financial circumstances and risk tolerances,” Peron said. “So it is never a matter of one size fitting all.”

But it is a matter of trying to assure that once investors have determined how much risk is appropriate for their situation, the managerial style they choose maximizes the potential return for whatever amount of risk is taken.

“Northern Trust’s engineered approach to constructing active portfolios seeks to contain risk to those categories that historically have adequately compensated investors for the amount of risk assumed,” Peron said.

Five Funds Driving the Active-Passive Bridge

Northern Trust has 15-plus years of experience in researching, engineering and implementing an active management strategy designed to link key characteristics of the active and passive investment styles. The strategy, based on Northern Trust’s systematic proprietary quality factor, forms the basis of portfolio construction in five Northern Trust mutual funds: Income Equity, Large Cap Value, Large Cap Core, Small Cap Core and Small Cap Value. Talk to your Northern Funds relationship manager about which of those “middle of the road” funds might best fit your needs.

Three pillars

That’s where what Peron calls “the three pillars of Engineered Equity” comes into play, laying a foundation for the bridge linking the active and passive styles.

The proprietary points of distinction that make up Northern Trust’s engineered approach to portfolio construction include:

1. Implement portfolios efficiently.

The objective of this first pillar is to give Northern Trust fund managers the tools to understand and potentially avoid unintended risks in their value- and core-based strategies.

Unintended risks are usually “uncompensated,” and thus detract from the risk-return profile of a fund. To help mitigate that possibility, the Northern Trust global equity quantitative research team developed an efficiency ratio to measure the risk-reward impact of various factors over time.

“It’s a matter of getting paid for the amount of risk that’s been taken,” he said.

Topping the list of what might be called a “worthwhile” risk are stocks with above-average dividend yields and those with below-average price-to-earnings ratios.

In each case, of course, the equity market is waving something of a red flag.

If there weren’t concerns, a stock’s price would be higher and its dividend yield lower. Which is why, Peron said, borrowing the broad diversification that is a major characteristic of a passively managed fund is a bedrock component of Northern Trust’s engineered approach to active management.

“Since the late 1920s, value stocks have been the top-performing group,” said Peron. “But the diversification aspect is vitally important in tempering the risk that goes along with buying value.”

Peron cited the example of British Petroleum, a value stock that abruptly lost half its value following the disastrous May 2010 oil spill in the Gulf of Mexico.

“By isolating the factors that embody risk, we strive to construct actively managed portfolios that are tailored to the needs of all our shareholders,” Peron said. “Our objective is to ‘engineer out’ uncompensated risk factors.”

2. Be savvy, but straightforward.

While engineering a more refined portfolio construction process, Peron said it is important to guard against making the system overly complicated.

With that goal in mind, Northern Trust fund managers using the engineered management style rely mostly upon fundamental measures of value and quality.

However, they also drill down into each of those traditional factors and combine them in ways that could dampen volatility during periods of market stress.

3. Embrace quality.

Northern Trust’s proprietary quality factor systematically sorts businesses according to characteristics that often have been shown to generate outperformance. Typically, these are companies that have strong balance sheets, high returns on equity and management teams that are adept in deploying capital.

On the flipside, Peron said that extreme volatility is a market characteristic of lower-quality securities, as well as being a type of risk that is not worth taking on.

“Our engineered strategies generally avoid high-beta stocks (those that are significantly more volatile than the overall market),” Peron said. “Certainly, volatility can be your friend under certain circumstances and during brief periods, but our research has shown that the potential reward of owning low-quality, volatile stocks is not worth the risk of holding them over the long haul.”

High leverage, or the amount of debt relative to equity on a company’s balance sheet, is another characteristic that often indicates lower quality. While it can be tempting to chase those types of stocks because of the potential to boost returns by using borrowed money, Peron said that too often those tactics saddle investors with large losses.

Peron acknowledged that, like highly volatile stocks, lower-quality securities sometimes outperform their sturdier counterparts. But those periods tend to be short-lived and virtually impossible to determine in advance.

Taken together, the three pillars of fund management that Peron described could provide a link between the two dominant investment styles of the last 30 years.

“Combining quality and value, for example, with broad diversification has been shown to be an effective way to merge active and passive management,” Peron said. “There really is a third and potentially better way of building portfolios for the long term.”

Logicians would like that answer.

Click for larger image

1 “Most mutual funds lag S&P 500 on one year returns.” Stan Choe. The Denver Post. Sept. 14, 2014.

Past performance is no guarantee of future results.

Diversification does not guarantee a profit or protect against a loss.

Equity Risk: Equity securities (stocks) are more volatile and carry more risk than other forms of investments, including investments in high-grade fixed-income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes.

High-Yield Risk: Although a high-yield fund’s yield may be higher than that of fixed income funds that purchase higher-rated securities, the potentially higher yield is a function of the greater risk that a high-yield fund’s share price will decline.

Interest-Rate Risk: Increases in prevailing interest rates will cause fixed-income securities, including convertible securities, held by the Fund to decline in value.

Small-Cap Risk: Small-capitalization funds typically carry additional risks since smaller companies generally have a higher risk of failure. Their stocks are subject to a greater degree of volatility, trade in lower volume and may be less liquid.

Value Risk: Value-based investments are subject to the risk that the broad market may not recognize their intrinsic value.

S&P 500® Index is an unmanaged index consisting of 500 stocks and is a widely recognized common measure of the performance of the overall U.S. stock market. It is not possible to invest directly in an index.

Alpha measures a fund’s risk-adjusted performance and represents the difference between a fund’s actual performance and its expected performance, given its level of risk.

Beta represents the systematic risk of a portfolio and measures its sensitivity to a benchmark.

Environmental, Social and Governance (ESG) three factors used to evaluate sustainability and ethical impact of an investment in a company or business.

Tracking Error measures the difference between the fund’s performance and that of the index.