- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Capital Market Assumptions: What AI Could Mean for Investors

AI’s adoption and advancement rates may counter declining productivity resulting from demographic shifts. Our confidence lies in AI’s longer term productivity boost versus shorter term adoption.

KEY POINTS

What it is

AI’s asymmetrical profile is clear in our view, with far more potential for upside gain than downside loss.

Why it matters

Increasing productivity through AI is emerging as a critical factor for economic growth in the face of challenging demographic changes.

Where it's going

We believe AI adoption and gains will likely be more evident long term, as the technology is adopted and use cases are refined.

Every year, Northern Trust’s Capital Market Assumptions Working Group develops forward-looking, historically aware forecasts on global economic activity and financial market returns. We analyze historical relationships between asset classes and drivers of asset class returns, and we develop forward-looking investment themes to inform how those relationships and return drivers may change in the future.

Our 2025 Capital Market Assumptions 10-Year Outlook contains three themes that examine the trends we see affecting the markets and economy over the next decade, providing the foundation for our asset class outlooks. One of the three themes is AI-Enabled Productivity, and that is the focus of this article.

AI-Enabled Productivity

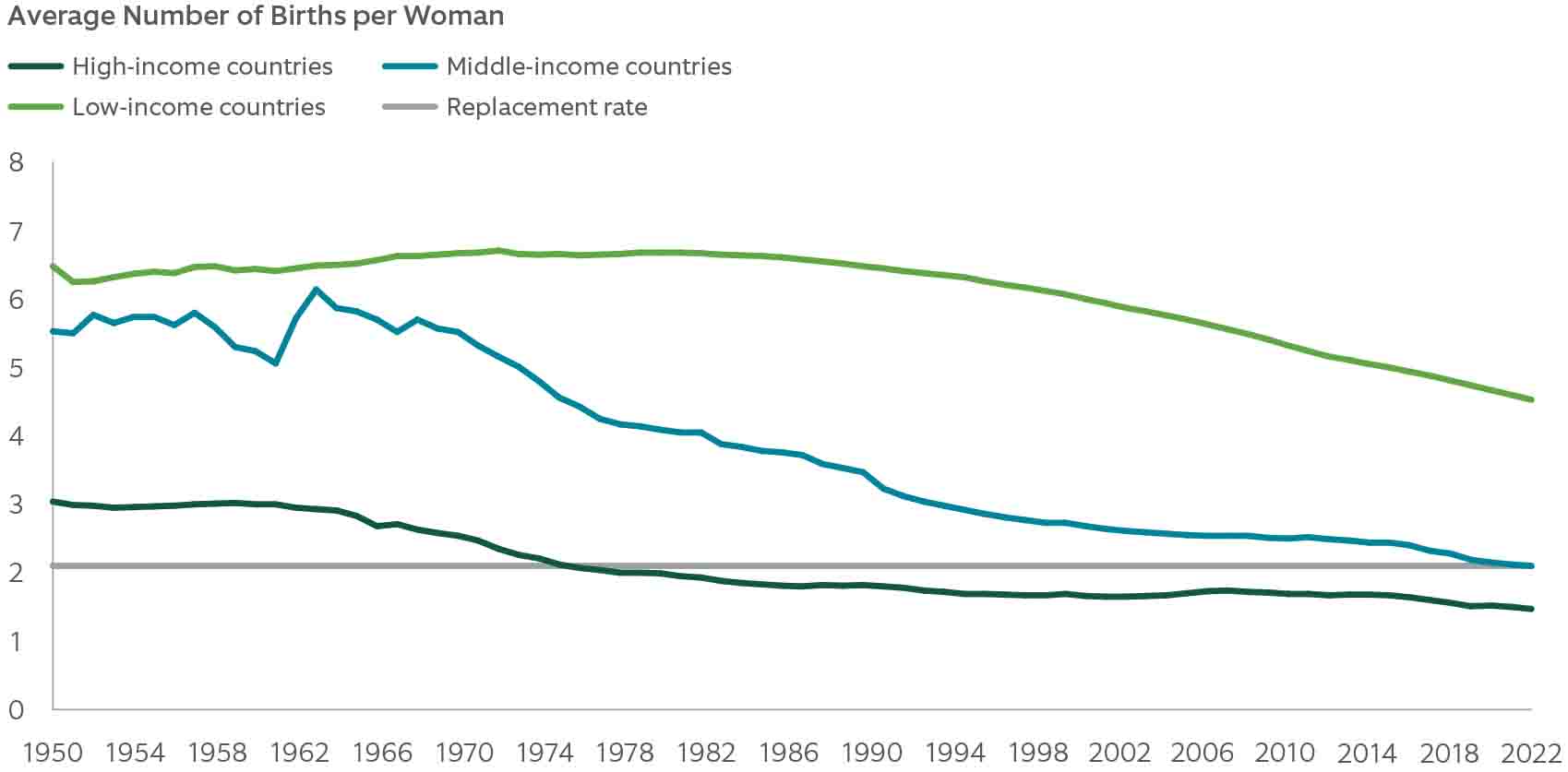

Increasing productivity through AI is emerging as a critical factor for economic growth in the face of challenging demographic changes. Historically, growth of the working age population has driven economic growth. However, fertility rates are declining (Exhibit 1), and governments are tightening their immigration policies for a variety of reasons, which likely will slow population growth. Further, life expectancies are increasing, resulting in a shrinking workforce as a percentage of total population in developed markets.

EXHIBIT 1: AI May Aid Productivity as Population Growth Slows

Historically, population growth has helped drive economic growth. As fertility rates decline, we expect AI to step in to increase productivity.

Source: United Nations, Department of Economic and Social Affairs, Population Division (2024). World Population Prospects 2024, Online Edition, data from 1950 to 2023. The replacement rate of 2.1 is the estimated number of births per woman required to maintain the population.

The potential impact of AI on productivity and economic growth is difficult to pin down and subject to great debate in academic and industry literature. While overall gains are acknowledged, the range of projections is wide. As examples, Daron Acemoglu, an economics professor at the Massachusetts Institute of Technology, argues that forecasting AI’s effect is hard to predict and requires speculation. Based on his framework, he sees a gain of 0.55% in total factor productivity over the next 10 years.1 In contrast, Goldman Sachs’ Joseph Briggs predicts a 9.2% gain in total factor productivity and 6.1% increase in economic growth over the next decade.2

Regardless of the wide range of estimates, AI’s asymmetrical profile is clear in our view, with far more potential for upside gain than downside loss. And while shorter term gains may come in spurts, or be obfuscated by other data, we believe AI adoption and gains will likely be more evident long term, as the technology is adopted and use cases are refined.

That said, AI could cause displacement in jobs and increase inequality. Potential AI productivity gains will likely differ across developed and developing economies due to the nature of existing work and respective states of technology. Within countries, impacts could also differ based on factors such as firm size, industry and adoption. Likewise, impacts on the labor market (acceleration, augmentation, automation) could vary.

As we look ahead to opportunities in an AI-Enabled Productivity world, we see potential winners and losers. Infrastructure (data centers, energy infrastructure) seems attractive, with potential opportunities to capitalize on this theme in private markets. Meanwhile, some of the losers may be highly indebted companies lacking the sufficient access to credit necessary to invest enough in AI in order to remain competitive.

About the CMA Process

Every year, Northern Trust’s Capital Market Assumptions (CMA) Working Group gathers to develop long-term financial market forecasts. The team adheres to a forward-looking, historically aware approach. This involves understanding historical relationships between asset classes and the drivers of those asset class returns, but also debating how these relationships will evolve in the future.

Our forward-looking views are encapsulated in our annual list of CMA themes, which — combined with our quantitative analysis — guide our expectations for long-term asset class returns. The CMA return forecasts are combined with other portfolio construction tools (standard deviation, correlation, etc.) to annually review and/or update the recommended strategic asset allocations for all Northern Trust managed portfolios and multi-asset class products.

The CMA Working Group is composed of senior professionals from across Northern Trust globally, including top-down investment strategists, bottom-up research analysts and client-facing investment professionals.

1 The Simple Macroeconomics of AI” by Daron Acemoglu, Massachusetts Institute of Technology, April 5, 2024. Total factor productivity is a measure of product efficiency, calculated by dividing total production (output) by average costs (inputs).

2 Goldman Sachs Global Investment research, Top of Mind Issue 129: Gen AI: Too Much Spend, Too Little Benefit?, June 2024.

IMPORTANT INFORMATION

Northern Trust Asset Management (NTAM) is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited, issued in the European Economic Association (“EEA”) by Northern Trust Fund Managers (Ireland) Limited, issued in Australia by Northern Trust Asset Management (Australia) Limited (ACN 648 476 019) which holds an Australian Financial Services Licence (License Number: 529895) and is regulated by the Australian Securities and Investments Commission (ASIC), and issued in Hong Kong by The Northern Trust Company of Hong Kong Limited which is regulated by the Hong Kong Securities and Futures Commission.

For Asia-Pacific (APAC) and Europe, Middle East and Africa (EMEA) markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. This information may not be edited, altered, revised, paraphrased, or otherwise modified without the prior written permission of NTAM. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. NTAM may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, its accuracy and completeness are not guaranteed, and is subject to change. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on market or other conditions.

All securities investing and trading activities risk the loss of capital. Each portfolio is subject to substantial risks including market risks, strategy risks, advisor risk, and risks with respect to its investment in other structures. There can be no assurance that any portfolio investment objectives will be achieved, or that any investment will achieve profits or avoid incurring substantial losses. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Risk controls and models do not promise any level of performance or guarantee against loss of principal. Any discussion of risk management is intended to describe NTAM’s efforts to monitor and manage risk but does not imply low risk.

Past performance is not a guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by NTAM. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For U.S. NTI prospects or clients, please refer to Part 2a of the Form ADV or consult an NTI representative for additional information on fees.

Forward-looking statements and assumptions are NTAM’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Not FDIC insured | May lose value | No bank guarantee