- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

A Shaky Recovery

JUNE 2023

Editor’s Note: Welcome to the premier issue of Northern Trust’s quarterly Asia Economic Outlook. We hope these views will be helpful to clients interested in details on regional performance.

2022 was a tough year for Asian economies, hit by soaring energy prices and the strong dollar. Higher energy prices pushed up inflation and added to the need for central bank tightening. Prospects for this year are not much improved, with varied economic performances expected across the continent.

Higher interest rates will keep domestic demand in check. Disinflation will continue, reflecting normalized supply chains and the impact of tighter monetary policy. Reduced interest rate differentials with the United States will help regional currencies hold their values a bit better.

China’s reopening will generate some positive spillovers, but export growth will wane with western economies set to slow sharply. Growing fragmentation amid rising geopolitical tension will weigh on the performance of highly open Asian economies.

Encouragingly, lessons from the 1997 Asian and 2008 global financial crisis are helping insulate the region from the banking stress experienced in the United States.

Following are our views on how major Asian markets are poised to perform this year and next.

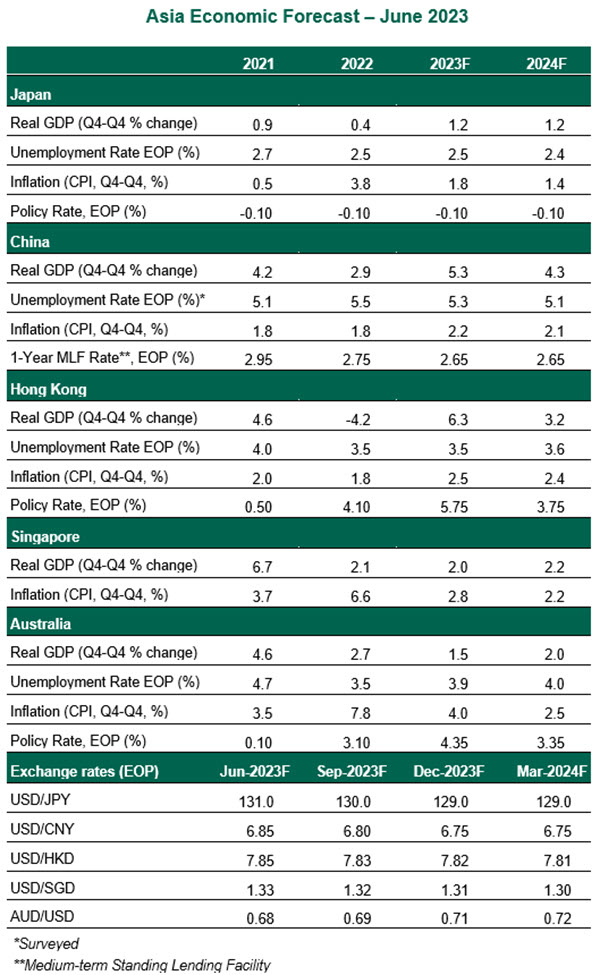

Japan

- Trends in Japan are following a similar path to those in the rest of the developed world, but on a more subtle scale: higher inflation, better wage gains for workers, and recovering growth. Pent-up demand and more reliable supply chains supported the economy at the start of the year. That said, growth momentum is set to weaken, led by a sluggish external backdrop and fading domestic demand.

- Inflation has been hovering well above 2% target since March 2022, fueling speculation that the Bank of Japan (BoJ) will be forced to reverse course under the new leadership. With inflation unlikely to sustain above 2% for reasons listed here, only modest policy changes are in the offing. The BoJ will likely tweak its yield curve control program by shortening its target maturity.

China

- The Chinese economy grew at a dismal rate of 3% year over year in 2022, below the global average for the first time in over four decades. With the economy no longer weighed down by COVID restrictions, the reopening has spurred a recovery in consumption. The property market is starting to stabilize. However, the optimism has tempered with the rebound falling short of broader expectations. A combination of weak employment, housing market uncertainty, weakened household balance sheets and softer export demand will hold the economy back. Our views on China are summarized here.

- A stalling post-pandemic recovery has forced the People’s Bank of China (PBoC) to resume monetary policy easing. The PBoC cut the reserve requirement ratio for almost all banks by 25 basis points amid spikes in domestic borrowing costs in March, followed by a 10 basis points reduction in the short- and medium-term lending rates. The moves indicate the central bank’s willingness to support recovery amid downside surprises to activity. Fiscal policy too will remain pro-growth with a focus on maintaining support for embattled developers and the property sector.

Singapore

- After recording a second year of economic recovery from COVID, the Singapore economy entered 2023 on weaker footing. Gross domestic product contracted in the first quarter. Singaporeans have been pulling back, reflected in a sharp contraction in retail sales at the start of the year. Industrial production fell for a seventh month in a row in April. China's reopening is expected to provide only a modest positive uplift to Singapore’s goods and tourism sectors. Higher inflation in rents and other operating costs are undermining Singapore’s attractiveness to foreign businesses. Trade data revealed another steep fall with more pain likely in store for the continent’s most trade-dependent economy.

- Amid increased financial stability concerns, moderating inflation dynamics and a less supportive growth environment, the Monetary Authority of Singapore (MAS) paused its tightening cycle. Given the inflation and growth outlook, we don’t expect any further tightening by the MAS.

Hong Kong

- After suffering a 3.5% contraction last year, Hong Kong’s economy is showing signs of recovery. Removal of COVID-related restrictions has led to visible improvements in activity and cross-border travel this year. The retail sector will benefit from a raft of measures such as cash handouts to residents, lower taxes and energy subsidies, along with inbound tourism. However, like most of its regional peers, the global financial hub also faces strong headwinds from the slowdown in the major advanced economies and tighter financial conditions.

- The Hong Kong Monetary Authority (HKMA), which follows the U.S. Federal Reserve in raising rates, hiked the Base Rate by 25 basis points to 5.50% at the May meeting. With the rising odds of the Fed hiking in July, we expect the HKMA to stick to its pre-set formula, implying a peak Base Rate of 5.75%. Hong Kong dollar (HKD) peg has come under renewed pressure. But despite recent pressure, the HKD's peg to the U.S. dollar is here to stay, backed by strong foreign reserves.

Australia

- Growth in Australian economic activity slowed in the March quarter and is forecast to remain subdued through this year. Retail sales volumes during the first quarter of 2023 fell for a second straight quarter, a sign that rising interest rates and the high cost of living are working to curb consumer spending. Conditions in the housing market are starting to stabilize, but the past declines in household wealth will continue to weigh on growth. Labor markets remain tight, but the unemployment rate is expected to rise because of subdued economic growth.

- After an initial pause in April, the Reserve Bank of Australia returned to tightening with hikes in May and June. Although inflation has peaked, the RBA board is still uncomfortable with its brisk pace given recent trends in wages and house prices. As a result, we expect one more hike of 25 basis points at the next meeting to a terminal rate of 4.35%.

Meet Our Team

Subscribe to Economic Trends & Insights

Discover our latest insights on all economic news, from breaking headlines to long-term trends.

Discover our latest insights on all economic news, from breaking headlines to long-term trends.

Watch Carl explain the latest economic news in his own words.

Review our forecasts for selected economic indicators and interest rates and explore how they could affect future U.S. economic conditions.

Explore the trends that will shape growth, employment, inflation and interest rates for major markets around the world.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation.

This material is directed to professional clients only and is not intended for retail clients. For Asia-Pacific markets, it is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors.

For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author’s employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 7th floor, Claude Debussylaan 18 A, 1082 MD Amsterdam; Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE Norway Branch, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651)/Northern Trust Fiduciary Services (Guernsey) Limited (29806)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) are licensed by the Guernsey Financial Services Commission. Registered Office: Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386), Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.