- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Hitting A Rough Patch

SEPTEMBER 2023

After displaying a mixed performance in the first six months of the year, a slowdown is becoming more uniformly apparent across major Asian economies. The outlook for the region is clouded by softening external demand, especially from China, and the higher for longer monetary policy environment at home & abroad. Consumption is losing its luster and won’t be able to fully offset the impact from reduced exports.

Inflation across the region has continued to fall, bringing the tightening cycle close to its end. The focus will likely shift to when central banks will pivot to looser policy. China is an exception, with the country’s central bank already easing to avoid persistent deflation. That said, higher global food and energy prices may complicate central banks' communications and decision-making in the coming months.

Growth is expected to be soft in the remainder of the year and for most of 2024, with the most apparent risk coming from China’s economic woes and growing fragmentation.

Following are our views on how major Asian markets are poised to perform this year and next.

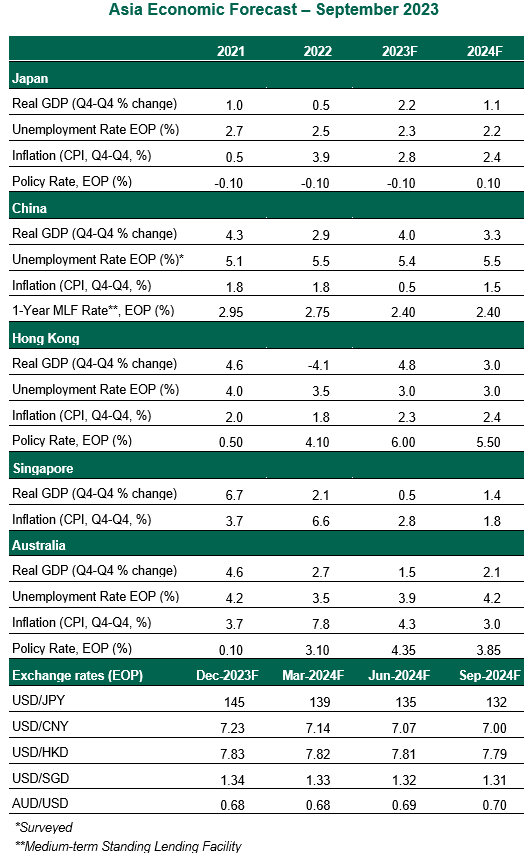

Japan

- The Japanese economy grew at an annualized rate of 4.8% in the second quarter, mainly driven by a surge in net exports. Growth is expected to slow after a strong first half, however, given the deteriorating external backdrop. Wage gains from the spring negotiation will underpin consumption, but the pace of recovery will be slow as pent-up demand and support measures fade.

- The Bank of Japan (BoJ) maintained policy rates at its September meeting, following a tweak in its yield curve control (YCC) policy in July. Recent communications have fueled speculation around further policy changes within the coming quarters. Given recent strength in wages and elevated inflation, we believe further policy revisions are in store, but not this year. The scrapping of YCC next spring followed by a pivot to monetary tightening in the second half of 2024 is our base case.

China

- China’s post-reopening bounce faded quickly. Real gross domestic product (GDP) grew 0.8% in the June quarter, down from 2.2% in the first three months of 2023. The slowdown reflects the end of China's multi-decade real estate boom, an increasingly challenging backdrop for exports and a guarded stance by Chinese policymakers. Activity data for August brought tentative signs of stabilization, but one month does not make a trend. China’s continued economic recovery is still challenged by insufficient domestic demand and narrowing export channels. Real GDP growth is likely to slow further to 4.0% year over year by the end of 2023. 2024 is likely to be even weaker, with 3.5% growth expected for next year.

- China’s massive property sector, the main source of wealth generation for Chinese households, remains a major headwind. Property sales have plunged. Housing construction continues to fall, and home prices slid further last month. Unemployment is rising, and confidence is falling. The incremental easing approach taken by policymakers suggests that they are no longer willing or able to rely on large-scale stimulus to boost growth.

Singapore

- Singapore’s GDP grew only 0.1% in the second quarter after a 0.4% contraction at the start of the year. A sharp rebound will be needed for full year growth to land anywhere close to the government's narrowed forecasted range of 0.5%-1.5% for 2023. A substantial improvement is unlikely given the tough external environment. Export volumes are shrinking, with China's economy unlikely to lend much support; America’s tighter monetary policy will weigh on its domestic growth in the quarters ahead, reducing imports from Singapore. Falling export earnings will feed through to reduced business investment and lower employment opportunities, exerting further downward pressure on domestic demand.

- Softening price pressures, coupled with weakening growth momentum, will prompt the Monetary Authority of Singapore (MAS) to keep its monetary policy parameters unchanged this year. That said, further weakness in economic activity will quickly shift the focus to monetary easing. The MAS uses an exchange rate-based framework to ensure price stability; we expect it to pivot by slightly reducing the appreciation of the Singapore dollar exchange rate policy band early next year.

Hong Kong

- Hong Kong’s economy showed signs of recovery at the start of the year, but momentum has weakened since then. The reopening boost is fading, with retail sales growing 4.3% sequentially in the second quarter after a 10.7% increase in the first quarter. The housing market recovery is suffering from higher mortgage rates. House prices are moderating, and transaction volumes have fallen below last year’s average. Trade is sluggish, given weak Chinese and western demand. Domestic consumption, underpinned by an improving labor market and the government's consumption voucher program, will be the main growth driver.

- · The Hong Kong Monetary Authority (HKMA) left its base rate unchanged at 5.75% at its September meeting, tracking a decision by the U.S. Federal Reserve to keep rates steady. With the Fed likely to hike one more time this year, we expect the HKMA to stick to its pre-set formula, implying a peak policy rate of 6.00%.

Australia

- The Australian economy grew faster than most of the major developed economies during the first half of 2023, led by net exports and business investments. However, tighter monetary policy and brisk inflation are stretching household budgets and weighing on spending. Conditions in the housing market are starting to stabilize, but the past declines in household wealth will continue to weigh on growth. The labor market is still tight, but is likely to loosen with softer economic activity. Australia’s export dependence on China also makes it among the countries most vulnerable to a Chinese slowdown.

- ·The Reserve Bank of Australia has now kept rates on hold at three consecutive meetings, but has refused to rule out the possibility of another hike. Against the backdrop of stubbornly high inflation, a reflating housing market and tight labor market conditions, we expect one more hike of 25 basis points later this year to a terminal rate of 4.35%, followed by a long pause. This means that tight policy settings will remain a drag on growth for much of 2024.

Meet Our Team

Subscribe to Economic Trends & Insights

Discover our latest insights on all economic news, from breaking headlines to long-term trends.

Discover our latest insights on all economic news, from breaking headlines to long-term trends.

Watch Carl explain the latest economic news in his own words.

Review our forecasts for selected economic indicators and interest rates and explore how they could affect future U.S. economic conditions.

Explore the trends that will shape growth, employment, inflation and interest rates for major markets around the world.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation.

This material is directed to professional clients only and is not intended for retail clients. For Asia-Pacific markets, it is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors.

For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author’s employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 7th floor, Claude Debussylaan 18 A, 1082 MD Amsterdam; Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE Norway Branch, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651)/Northern Trust Fiduciary Services (Guernsey) Limited (29806)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) are licensed by the Guernsey Financial Services Commission. Registered Office: Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386), Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.