Global Economic Outlook: Tough Nut To Crack

Slower growth and persistent inflation are pervasive across advanced economies.

The good news is that the world’s major economies have not yet cracked under the pressure of tighter monetary policy. But the bad news is that inflation in the U.S. and Europe has also yet to crack completely, meaning that more policy restraint is likely in the months ahead. This will further challenge the global outlook.

Hopes of a soft landing have not faded, but the path remains narrow. Strong labor markets are producing rising real incomes which support spending, but post-pandemic demand and saving have generally been exhausted. China was expected to emerge as a driver of global growth in the aftermath of COVID, but its post-pandemic economic boom proved to be short-lived.

Soft landing remains our base case for major markets. However, the deeper the central banks take rates into restrictive territory, the lower the chances of coming out unscathed.

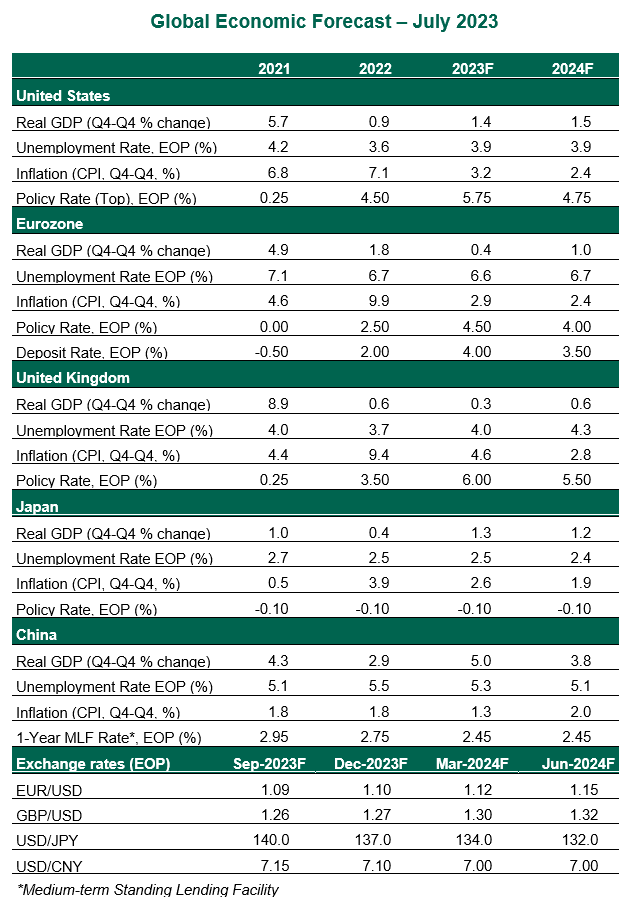

Here are our up-to-date perspectives on how major economies are poised to perform during this year and next.

United States

- Inflation improved in June, with the consumer price index falling to a two-year low of 3.0% year over year. The core measure eased to 4.8%. While a step in the right direction, the battle is far from over. The deflator on core personal consumption expenditures, the Fed’s preferred gauge, has been stuck at around 4.6% for several months. Shelter costs have not moderated in the manner that many had expected. The labor market is tight and wage growth is high, keeping services inflation elevated.

- The Fed pressed pause in June, after 10 consecutive rate increases, accompanied by guidance that more tightening was expected. The Summary of Economic Projections (SEP) revealed that most FOMC members expect two more hikes in the balance of the year. A quarter-point increase at the July 26 meeting looks like a done deal. The FOMC has erred on the side of tightening to contain inflation, and we do not doubt the path set in the SEP. Absent any stresses, a final hike in September is our base case.

Eurozone

- The eurozone witnessed a technical recession at the start of the year. Economic indicators continue to point toward weak momentum, even as consumers see their real incomes improving amid falling headline inflation.

- Core inflation surprised to the upside in June. Going forward, the region faces the potential for renewed disruptions in food supplies amid the ongoing heatwave and Russia’s withdrawal from the Black Sea grain deal. This will keep the European Central Bank (ECB) in a hawkish stance. The ECB delivered the widely expected 25 basis point increase at the June meeting, with a strong signal that further tightening may be needed. Two more hikes are in store, followed by a long pause through the middle of 2024.

United Kingdom

- The resilience of the British economy has helped policymakers and markets breathe a sigh of relief. Recession has been postponed, but the question is for how long? Elevated household saving ratios could provide some cushion, but high inflation and interest rates will continue to hold the economy back. Rising mortgage rates will deepen the housing downturn. A thriving labor market is the reason why we think the British economy will narrowly avoid a downturn.

- The U.K. shows the least evidence of disinflation. A stronger sterling will offer some reprieve from high import costs. But with wages growing at a very strong pace, the descent of core inflation will be slow. A longer period of tighter monetary policy is our base case. The Bank of England stepped up the inflation fight with a 50 basis point hike in June. Another half percentage point move in August with two more hikes at subsequent meetings is likely. Cuts will follow only when inflation pulls back markedly, likely in the middle of 2024.

Japan

- The Japanese economy, surprisingly, has been among the few bright spots this year. Consumption has improved, and the spring negotiation of pay raises will underpin demand. But the external backdrop for exports is less favorable and will drag overall growth down.

- Inflation has risen to levels not seen in decades. Yet the Bank of Japan (BoJ) is in no rush to tweak policy or raise rates. With market functioning improving, the BoJ is in no rush to tweak its Yield Curve Control program. Wider interest differentials are contributing to a weaker yen and inflationary pressures. Absent sustained wage increases, inflation is likely to fall back below the 2% mark, preventing the BoJ from changing the course of its monetary policy.

China

- The reopening boost to growth has faded. Manufacturing is contracting, deflation is looming, exports are moderating, and youth unemployment is at a record high. The real estate sector is in a downturn. Consumer confidence is dented, reflected in slower spending on everything from travel to cars and homes. The finances of heavily indebted local governments aren’t in great shape, either. The goal of “around 5%” growth is looking unattainable.

- In response to weak data, policymakers have lowered interest rates and pledged to do more at the regional level to support demand. But easing policy is unlikely to offer substantial relief. Lower rates will likely hit the profitability of banks, already staring at losses from the real estate slump. A temporary economic stimulus is unlikely to lift household incomes or sentiment, but a large scale fiscal stimulus will compromise ongoing deleveraging efforts.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.