Global Economic Outlook: Hawk-Eyed

There is renewed anxiety among central bankers in the face of sticky inflation.

Despite widespread pessimism on prospects for major economies, growth has remained resilient. That is the good news; the down-side is that inflation has also remained strong in spite of tightening monetary settings. Private sector balance sheets remain healthy. Tight labor markets on both sides of the Atlantic are fueling wage gains and underpinning spending.

Aspirations for a soft landing had tempered the pace of monetary policy tightening. But there is renewed anxiety among central bankers in the face of sticky price pressures. Monetary authorities have either resumed tightening or turned more hawkish, displaying their willingness to take conditions further into restrictive territory. The cost of overtightening to prevent a wage-price spiral is seen as small relative to the cost of underestimating inflation’s persistence.

We continue to expect soft landings in the major centers, but uncertainty around the drag from tighter financial conditions increases downside risk.

This month’s edition of the global outlook offers a deep dive into the eurozone economy.

Eurozone

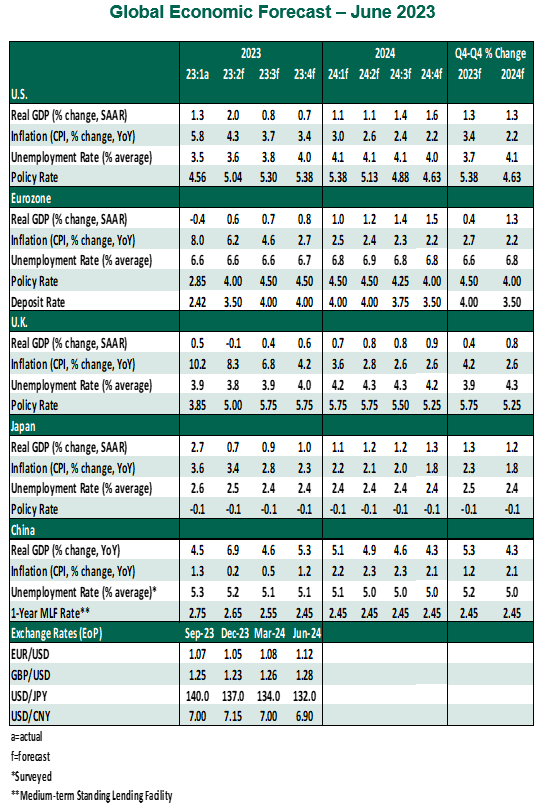

- A recession was expected towards the end of 2022 as the eurozone households grappled with high energy and food prices that stretched their budgets. Indeed, the eurozone economy endured a mild winter retreat. Gross domestic product (GDP) contracted 0.1% quarter over quarter in both the first quarter of this year and the last three months of 2022. Thanks to the cost of living crisis, household consumption pulled down GDP growth by 0.1 percentage points, after a larger 0.4 percentage point drag in the last quarter of 2022.

- After a positive start to the second quarter, incoming data and surveys are pointing toward weak economic momentum. The euro area industrial sector is suffering from weak orders. A softer global economic backdrop will weigh on export performance. Investments will be adversely impacted by higher interest rates.

- Thriving labor markets should steady consumer spending. This, coupled with lower inflation, will likely result in a modest but fragile recovery in the second half of 2023.

- In a welcome reprieve, eurozone inflation surprised to the downside in May, with relief coming from components other than energy. The year over year change in the overall consumer price index decelerated by almost a full percentage point to 6.1%. The core measure (excluding energy, food, alcohol & tobacco) decelerated three-tenths to 5.3% year over year as prices of both services and non-energy industrial goods fell in May. This news provides some hope that underlying price pressures could be easing.

- The worst phase of price increases is likely in the past for Europe, but meaningful improvements in inflation from here will be harder to achieve. As the energy shock unwinds and supply chains normalize, wage growth has become the central influence on recent inflation developments.

- The eurozone labor market remains resilient, with the unemployment rate dropping to an all-time low of 6.5%. Tight employment conditions have led wage growth to accelerate sharply, by 5% in the first quarter of 2023, compared with the same quarter of the previous year. Labor productivity contracted in the previous quarter, putting upward pressure on labor costs. Improvement in productivity growth will hold the key to preventing a wage-price spiral from forming.

- The European Central Bank (ECB) has responded to the surge in inflation by embarking on the fastest tightening cycle in its history. Although core inflation decelerated last month, one data point doesn’t make a trend and underlying price pressures are still elevated. This justifies a hawkish tone from the ECB. Officials signaled that more tightening will likely be required amid strong labor market and wage dynamics. A hike in September, which seemed highly unlikely prior to this month’s meeting, is now a real possibility.

- We now expect the ECB to hike by 25 basis points at its next two meetings in July and September, taking the peak deposit rate to 4.00%. The risk of overtightening is present, as the impact from past increases in interest rates yet to fully feed through to the real economy. This is perhaps the only factor that could force the ECB to pause the current cycle next month.

- With Europe's gas crisis diminished and budget rules set to become binding again in 2024, fiscal policy will soon become a drag on growth. However, some European governments remain under pressure to provide support to cap rising prices and protect purchasing power. But there is limited scope for further assistance, given rising government interest payments.

- Europe will also have to find room in national budgets to address climate change, defense, and technology transition. Debate is active on how these investments will count against debt and deficit targets.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.