Banking on the Banking System

Tightening credit conditions will weigh on growth, especially in Europe..

The initial months of the new year delivered positive surprises for the global economy. Major advanced economies looked on track on avoid a downturn, inflation moved past its peak and labor markets remained resilient. However, recent stress in the banking sector in the U.S. and Europe has shaken confidence.

It’s too soon to assess the broader implications of the ongoing banking turmoil. We expect that tighter credit conditions will prove to be a headwind for activity. Europe, particularly, will feel the pain as banks account for the lion’s share of credit received by European businesses and households. Policymakers will also have to tread carefully, striking the right balance between taming inflation and sustaining financial stability.

Some concern over the banking sector may continue. But policymakers’ willingness to backstop temporary liquidity mismatches, coupled with stronger balance sheets across sectors, should prevent the episode from swelling into a bigger crisis.

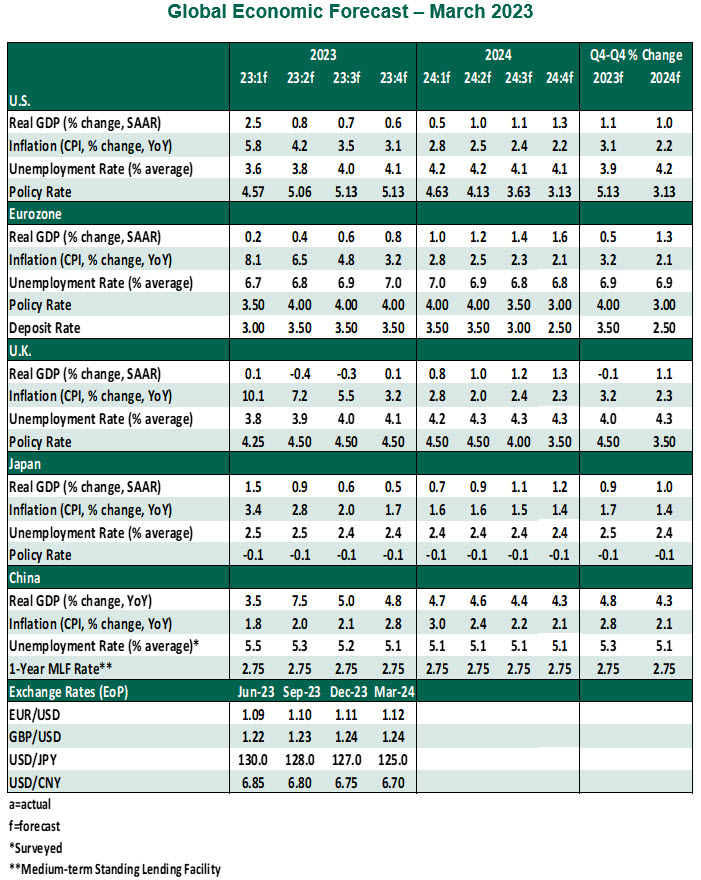

This month’s edition of the global outlook offers a deep dive into the U.K. economy, which faces a host of headwinds.

United Kingdom

- Momentum in the U.K. economy has been improving since the start of the year. Gross domestic product rose by 0.3% month over month in January, regaining some of the ground lost in December 2022, when output had declined by 0.5%. Retail sales have rebounded, raising optimism that the nearly two-year decline in sales is at an end. Purchasing managers’ indices are back in expansion territory. These data points have raised hopes among observers that a slump can be avoided. We are not so sanguine.

- In our view, a recession has only been delayed, not avoided, as the economy continues to face a host of challenges. Widespread industrial action and strikes are already weighing on activity. Inflation is set to remain high this year, outstripping earnings again. Financial conditions will tighten further on the back of current banking sector turmoil, which will limit growth. Despite some loosening in the recent budget, there will still be a significant tightening of fiscal policy in the period ahead. We expect the U.K. economy to contract in the next two quarters.

- 2023 will prove to be another difficult year for British households. Consumer incomes will remain squeezed amid elevated price pressures and tighter monetary policy. More than 1.4 million mortgage holders are facing a hefty rise in debt servicing costs when they renew their fixed rate mortgages this year.

- Both headline and core inflation were higher than expected in February, adding to the Bank of England’s (BoE) dilemma. The overall rate rose three-tenths to 10.4% year over year, while core inflation over the prior twelve months increased to 6.2% from its January value of 5.8%. The increase was primarily driven by higher prices in the restaurants and hotels category, along with notable increases in the costs of food and beverages. The combination of strong base effects, lower energy costs and easing supply chain pressures will continue to exert downward pressure on inflation. However, sticky underlying price pressures mean that inflation will descend only gradually.

- Most measures of employment suggest the labor market remains tight. The unemployment rate is steady, near its historic lows of 3.7%. Firms continue to report labor shortages as the jobs-workers gap remained unchanged in January. Millions of Britons are not actively looking for work due to mental health issues, long COVID and liberal terms for receiving benefits payments. Wage growth, though recently easing, remains above the level consistent with the BoE inflation target. As a result, the risk of a wage-price spiral remains the highest in the U.K. among major advanced economies. With weakening economic conditions, we expect to see the unemployment rate rise, putting downward pressure on earnings.

- Following the lead from the Federal Reserve and the European Central Bank, the BoE has also stayed focused on fighting inflation. The British banking sector remains resilient with healthy capital and liquidity positions; no U.K. institutions have been caught in the recent rumor mill. Given the Monetary Policy Committee's focus on tight labor market conditions and persistent underlying price pressures, the BoE raised the Bank Rate by 25 basis points this month to 4.25%, while leaving the door open to another hike at the May meeting.

- Recent data and the messaging from the March meeting are in line with our expectation of the Bank of England concluding its tightening cycle with a final 25 basis point hike at its next meeting. With inflation expected to remain well above the 2% target into next year, the first cut is unlikely to come before the middle of 2024.

- The Spring Budget offered some immediate relief to struggling households. The energy price guarantee, which caps annual energy bills at £2,500 per year, will remain in place for an additional three months to June 2023. Last year’s 5 pence per liter cut in the fuel duty was also extended for another year. That said, overall fiscal policy is set to tighten significantly.

- Households will be affected by the continual freeze on income tax allowances, which effectively acts as a tax increase. According to the Office for Budget Responsibility calculations, freezing income tax and National Insurance thresholds will raise an extra £29.3 billion a year in taxes by 2027/28.

- The new Brexit deal for Northern Ireland was formally adopted last week, removing a key uncertainty around the future of the U.K.’s trade ties with the EU. With the fears of a trade war fading, business investments could recover after having stagnated in the wake of Brexit. However, the Windsor Framework does little to remove the existing bottlenecks that were introduced following the U.K.’s departure from the bloc.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.