- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

S&P 500 Index Rebalance: Uber Addition Boosts Weight of Transportation

The addition of rideshare company Uber to the S&P 500 index notably impacted the sector and industry composition.

Key Changes in the Index

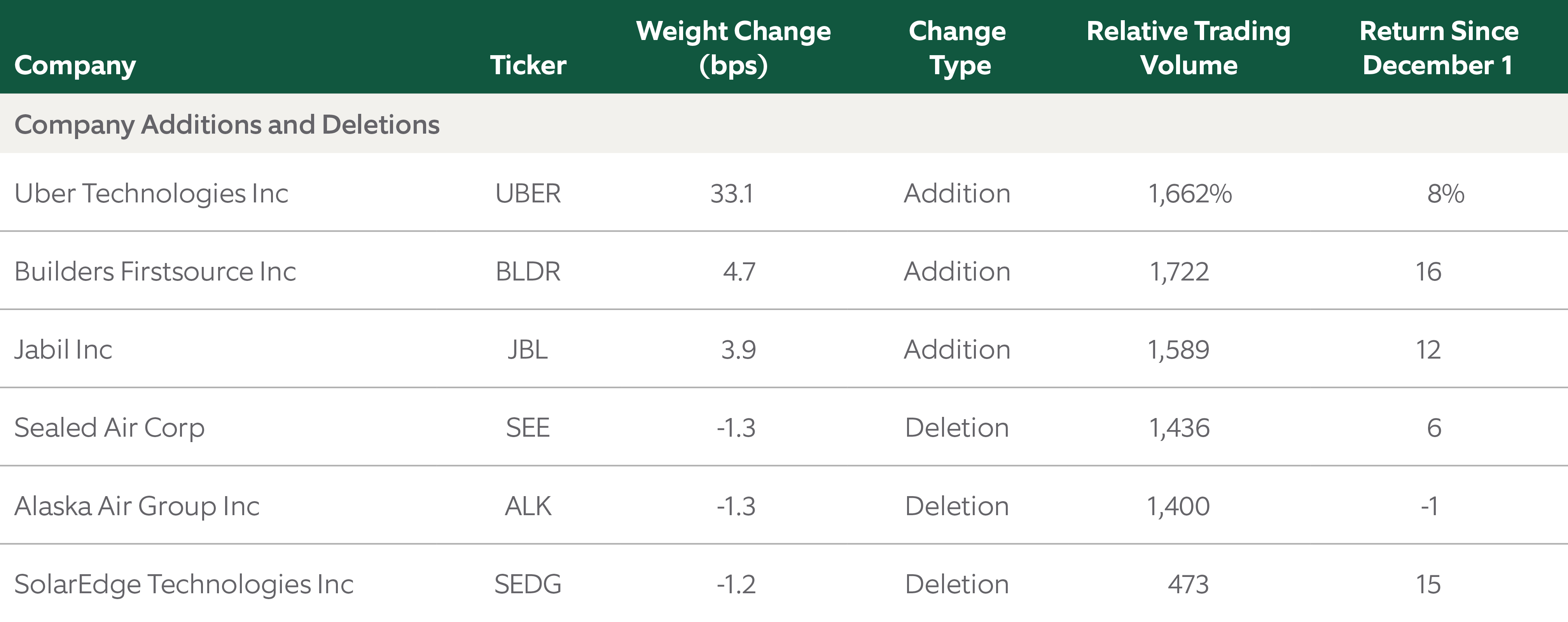

In the December S&P 500 Index rebalance effective December 18, S&P Dow Jones Indexes added rideshare company Uber Technologies, with a weighting of 0.3% in the index. While the delay in adding Uber to the index may surprise some investors, S&P requires member companies to demonstrate positive earnings in the latest quarter and over the preceding four quarters. This was the same rule that kept Tesla out of the large cap index until December 2020, when the electric vehicle company was finally added as the sixth-largest company to the index. Additionally, constituents must maintain an adjusted market cap of at least $14.5 billion. Uber has a market cap of $118 billion, multiples of the $31 median market cap for companies in the S&P 500.

Other additions include building products company Builders Firstsource with a 0.04% weighting and manufacturer Jabil with a 0.03% weighting. S&P removed airline Alaska Air, packaging company Sealed Air and solar power firm SolarEdge Technologies from the index. More details on key weight changes are in Exhibit 1.

EXHIBIT 1: KEY CHANGES IN THE S&P 500

Uber joined the index with a weighting change of 0.3%. Three companies were added while three were removed.

Source: S&P Dow Jones, as of December 1, 2023. Share decreases occur when companies repurchase shares. Relative trading volume is the daily trading average since December 1 versus the average 60-day daily trading before December 1.

Aligning the Index Portfolio to the Changes

As an index portfolio manager, we look at increased weightings for companies as “buys” and decreased weightings as “sells,” as that is how we need to trade the portfolio to align with the rebalancing. The weightings of the buys and sells must be equal to maintain consistency in the index, and in this case each side of the S&P 500 rebalance represented 0.42% in the index. The buys include 0.38% for the three new companies and sells included the 0.03% reduction for the elimination of the three companies and 0.39% for share decreases. All weights mentioned above are based on December 1 close prices, when S&P announced the changes.

Sector and Industry Impact

The rebalances also changed the sector and industry composition of the index, as shown in Exhibit 2. At a sector level, industrials increased the most through the addition of Uber. Communication services and financials declined the most partly because of share decreases in Google browser company Alphabet, credit card firm Visa and financial firm JPMorgan. Industry movements largely followed sectors. The transportation sector gained the most through Uber while media and entertainment sector fell the most due to Alphabet. Energy declined the most partly because Exxon Mobil and Chevron. Industry group movements largely followed sectors. The transportation sector gained the most through Uber while the energy sector fell the most.

EXHIBIT 2: UBER DRIVES SECTOR AND INDUSTRY WEIGHTING CHANGES

The addition of Uber boosted the weightings of the industrials sector and transportation industry.

Performance of S&P 500 Rebalance

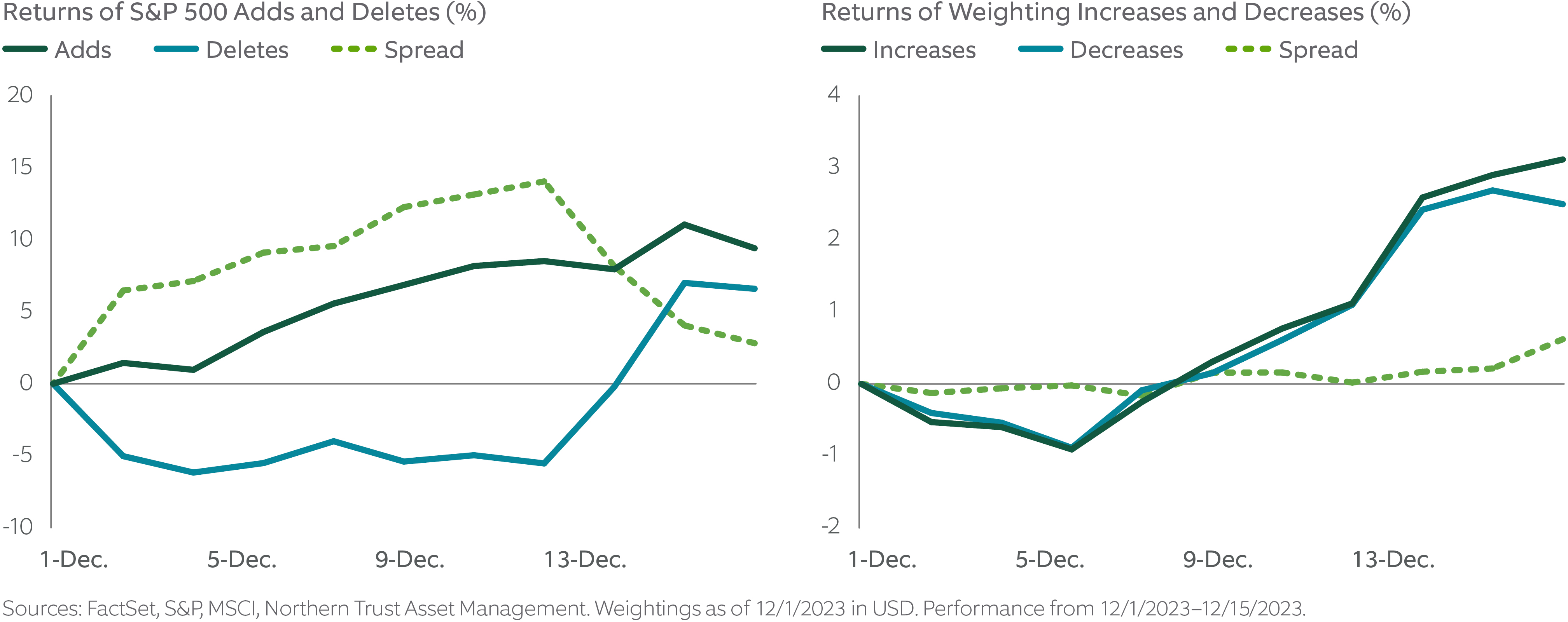

Although the pressure from index managers can impact performance, we note that the S&P rebalance is well advertised. This actually provides a shock absorber as other market participants can provide liquidity and dampen the potential market impact. Further, there are other catalysts driving stock prices beyond the rebalance including macro events and those specific to companies. In the case of this rebalance, adds outperformed deletes with deletes closing the spread on the last trading day. Increases and decreases largely performed in-line with each other. These results are shown in Exhibit 3. The sheer number of names in each category also resulted in lower spread with increases edging out decreases in the last days of trading.

December 15 saw expected, but extreme trading volumes due to the simultaneous expiration of stock options, stock index futures, and stock index options contracts, an event know as a triple witching date. Uber experienced trading volumes 16 times above average as seen in Exhibit 1. Overall, the heightened trading did not create much impact.

EXHIBIT 3: PERFORMANCE WENT THE 'RIGHT WAY'

Normally, we expect the added companies to outperform the deleted companies, which occurred since the S&P release on the changes on December 1.

What the Rebalance Means to Investors and Index Managers

The S&P 500’s December rebalance has shown that eligibility requirements can prove impactful because growth companies can reach significant market capitalizations prior to turning a consistent profit, as was the case with Uber and Tesla three years prior. While the overall index turnover was relatively small at 0.92%, given the amount of assets that track the S&P 500, trading volume increased significantly for the added and deleted companies, along with stocks with share and/or float changes.

Attentive analysis is crucial to understand how an impending index rebalance will shape the index, and by extension, the portfolios that track it. We believe this analysis requires a thoughtful approach with the aim of keeping tracking error to a minimum while ensuring that the market impact and trading costs related to rebalancing do not erode wealth over time.

IMPORTANT INFORMATION

Northern Trust Asset Management (NTAM) is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited, issued in the European Economic Association (“EEA”) by Northern Trust Fund Managers (Ireland) Limited, issued in Australia by Northern Trust Asset Management (Australia) Limited (ACN 648 476 019) which holds an Australian Financial Services Licence (License Number: 529895) and is regulated by the Australian Securities and Investments Commission (ASIC), and issued in Hong Kong by The Northern Trust Company of Hong Kong Limited which is regulated by the Hong Kong Securities and Futures Commission.

For Asia-Pacific (APAC) and Europe, Middle East and Africa (EMEA) markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. This information may not be edited, altered, revised, paraphrased, or otherwise modified without the prior written permission of NTAM. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. NTAM may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, its accuracy and completeness are not guaranteed, and is subject to change. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on market or other conditions.

All securities investing and trading activities risk the loss of capital. Each portfolio is subject to substantial risks including market risks, strategy risks, advisor risk, and risks with respect to its investment in other structures. There can be no assurance that any portfolio investment objectives will be achieved, or that any investment will achieve profits or avoid incurring substantial losses. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Risk controls and models do not promise any level of performance or guarantee against loss of principal. Any discussion of risk management is intended to describe NTAM’s efforts to monitor and manage risk but does not imply low risk.

Past performance is not a guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by NTAM. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For U.S. NTI prospects or clients, please refer to Part 2a of the Form ADV or consult an NTI representative for additional information on fees.

Forward-looking statements and assumptions are NTAM’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Not FDIC insured | May lose value | No bank guarantee