- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Bitter Sweet Symphony

Elevated geopolitical tensions are the biggest source of uncertainty for the trade-dependent economies in Asia.

By Vaibhav Tandon

Asian economies witnessed a volatile 2023, with inflation, rising interest rates, and China’s economic woes dragging growth down. While the road to reflation will be bumpy for China, the rest of Asia is likely to do well this year.

Several factors contribute to our optimism. Labor markets in most major regional economies remain strong. The drag from tighter global monetary policy will fade. External demand will be constrained by weak growth in developed economies in the first six months of the year, but those headwinds will fade in the second half of 2024 as western economies achieve a soft landing.

The improvement in the semiconductor/chips cycle will underpin demand for Asian goods, which suffered through a slump for the last two years. Depleting U.S. inventories are also pointing towards increased demand for regional exports.

The path to economic prosperity is not assured. Policy uncertainty will remain high as over 50 economies worldwide head into elections. The evolving international landscape amid heightened geopolitical tensions will remain the biggest source of uncertainty for the trade-dependent economies in Asia.

Following are our views on how major regional markets are poised to perform in 2024.

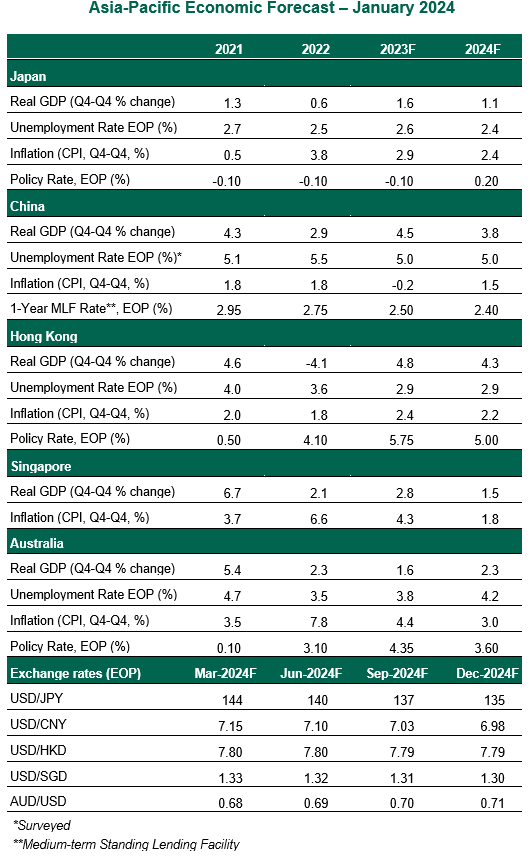

Japan

- Japan was one of the better-performing advanced economies in the first half of 2023, but lost some momentum in the second half. High inflation and a subdued external backdrop took their toll. But the incoming data suggests momentum is returning. Consumer confidence, corporate sentiment and the outlook for business investment are improving. Higher salaries and growth in real wages are set to support private consumption. The Japanese economy has woken up from a deep slumber, but is still some distance from being up and running.

- The Bank of Japan (BoJ) offered no surprises as it left interest rates in negative territory at the December meeting. To markets’ disappointment, the BoJ governor refrained from giving any hint of an imminent exit from negative interest rate policy. In our view, the BoJ will be the only major bank which will move to make policy less accommodative this year. A high wage settlement in spring negotiations will allow the central bank to move rates gradually into slightly positive territory.

China

- China is struggling to reflate its economy with property sector woes at center stage. Private investment has been anemic, and capital outflows have been substantial. While Tokyo has exited deflation, Beijing is battling hard to avoid it. Consumption and sentiment remain weak. China remains the world’s manufacturing hub, but its dominant position will continue to weaken, constraining its export growth.

- China is not facing an imminent crisis. The economy is likely to muddle through a firmly managed clean-up process. However, the risk of the economy falling into a debt-deflation loop is very much alive as policymakers navigate through the unfavorable structural environment and tough policy choices. Growing concerns about geopolitical risk will continue to weigh on investor appetite for Chinese assets.

Singapore

- Singapore ended the year on a strong note, with real gross domestic product growing 2.8% year over year in the fourth quarter of 2023 compared to 1.0% in the prior quarter, led by gains in the manufacturing and construction sectors. Global electronics demand is recovering, driven by a replacement cycle with new models and upgrades. This will provide support to the vital exports sector. As the global goods cycle turns, inflation eases and global monetary policy turns less restrictive, Singapore’s economy is expected to post an improved performance in 2024. But the subdued demand from a structurally weaker China will be a limitation.

- Rebalancing of the labor market and wage moderation will ensure continued progress on disinflation, allowing the Monetary Authority of Singapore (MAS) to unwind its historically tight monetary policy. We continue to expect the MAS, which uses an exchange rate-based framework to ensure price stability, to reduce the rate of appreciation in the Singapore dollar later this year.

Hong Kong

- Recent activity data showed Hong Kong's (HK) economic recovery remains modest. The likelihood of a significant improvement in economic fortune is low. Recent property sector easing measures, such as lower stamp duties and higher maximum loan-to-value ratios have failed to provide a lift to the housing market. Weaker Chinese demand is weighing on Hong Kong’s exports and its tourism sector. Consumption, which was underpinned by an improving labor market and the government's consumption voucher program in 2023, will moderate as weaker trade sector performance feeds through to the domestic labor market.

- Apart from trade, Hong Kong is also exposed to China through the ongoing property sector downturn there. HK banks have significant credit exposure to mainland China, accounting for about 40% of total loans. That said, the sound financial system will help absorb the potential shocks from credit losses from mainland China.

Australia

- Australia's economy outperformed expectations for much of 2023, but is carrying less momentum into the new year as policy settings exert a drag on activity. There are signs that the labor market is slackening. While the growing demand for labor was met with additional population growth, it added to upward pressure on inflation, especially in housing. The combined impacts of tighter fiscal and monetary policy settings will weigh on growth in the first half of the year, but moderating inflation and the boost to real incomes will aid a durable improvement in the last two quarters of 2024.

- The Reserve Bank of Australia (RBA) remained on hold at the December meeting as it assessed incoming data. The minutes of the meeting showed that the central bank was encouraged by global disinflation. However, strong core inflation warrants a cautious approach by the RBA, leaving less room for early easing. We expect wage and price disinflation to continue, which will set in motion a gradual easing late in 2024.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Related Content

Weekly Economic Commentary

Discover our latest insights on all economic news, from breaking headlines to long-term trends.

Learn More

The View From Here

Watch Carl explain the latest economic news in his own words.

Learn More

US Economic Outlook

Review our forecasts for selected economic indicators and interest rates and explore how they could affect future U.S. economic conditions.

Learn More

Global Economic Outlook

Explore the trends that will shape growth, employment, inflation and interest rates for major markets around the world.

Learn More

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation.

This material is directed to professional clients only and is not intended for retail clients. For Asia-Pacific markets, it is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors.

For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author’s employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 7th floor, Claude Debussylaan 18 A, 1082 MD Amsterdam; Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE Norway Branch, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651)/Northern Trust Fiduciary Services (Guernsey) Limited (29806)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) are licensed by the Guernsey Financial Services Commission. Registered Office: Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386), Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.