- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

May Market Pulse Visualized

My recent Market Pulse discussion with Marc Mallet focused on energy and gold. I wanted to share some of the charts, data, and articles that we covered in the May podcast.

We focused on energy on this podcast due to renewed energy in this sector. Energy stocks are relatively cheap.

Source: Goldman Sachs

The energy sector has also outperformed recently (even better returns than tech sector) and has been less correlated to the broader market.

In the U.S., energy investment has been flat or declining in recent years. Significant investment needs to be made into both energy supply and distribution now and into the future.

And demand for energy should increase dramatically in the near future, from a combination of growing middle classes in emerging markets, the pivot to renewables/clean energy sources, and growing demand from power-hungry AI services. PJM updated their 2023 power demand forecast to reflect energy-hungry data center consumption over the next decade. Generative AI is a significant reason behind this uptick in anticipated data center power demand.

From JP Morgan’s 14th Annual Energy Paper “Electravision”

The path towards increased zero/low emission energy supply will perversely drive more energy demand. When considering the pivot from traditional energy sources like coal and natural gas to renewables, one must understand capacity factor. The capacity factor represents the ratio of actual energy produced to the potential capacity of the power plant. The resulting percentage allows a comparison of the reliability of various power plants. A theoretical plant with a capacity factor of 100% means it is producing power all of the time. As illustrated below, renewables tend to have lower capacity factors because the sun sets at dusk and the wind is not always blowing. The pivot to renewables will therefore require more redundancy of power plant sources and varieties and higher levels of nameplate energy capacity because renewables tend to be less reliable sources, resulting in a longer timeframe and a more costly investment cycle than most realize.

Source: US Energy Information Administration

The process of making renewable energy power plants is also very energy intensive. Consider solar panels: the largest input is polysilicon, which is massively energy intensive to make. And given that China controls the market for polysilicon, the U.S. will increasingly move more product onshore as a result of the rapidly polarizing world we live in, putting further demands on electricity. As an example, one of the largest polysilicon plants in the U.S., Hemlock Semiconductor Operations based in Michigan, uses the equivalent electricity of Lansing and Ann Arbor combined when in full production (read more here).

Another polysilicon production plant in Montana recently closed due to the high costs of electricity (read more here).

Solar panel construction and replacement (they have about a 30 year lifespan) will be energy intensive wherever they are built.

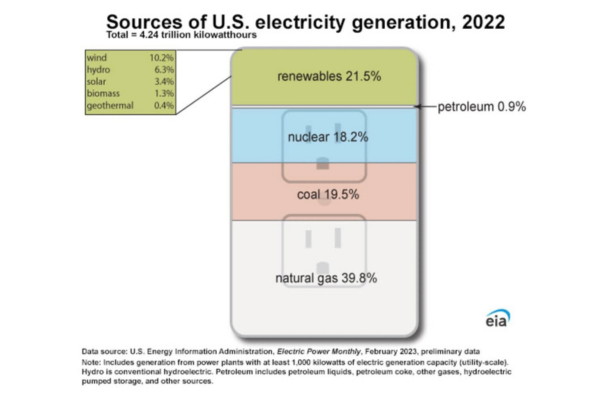

Despite heavy investment into renewables, only 21.5% of electricity produced in the U.S. today is from renewable sources. In 1990, renewables represented about 12%. Weak progress in 30+ years. Far more investment into both clean energy generation and distribution is needed.

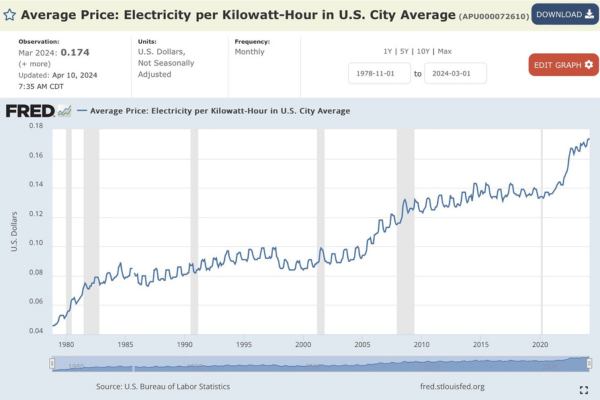

The average electricity price in the U.S. has already risen substantially, especially over the last few years…

…despite energy demand being essentially flat over this time period.

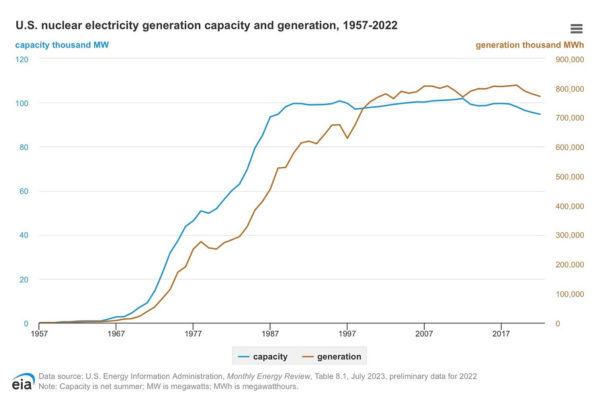

Nuclear energy development in the U.S. is nearly non-existent. Capacity and generation has been flat for over 20 years.

Plans for a new and more modernized nuclear power product have been stymied by restricted access to enriched Uranium. Russia controls over 50% of the market for enriched Uranium and the U.S. currently buys about 20% of its fuel for nuclear power plants from Russia, sending over $1 billion in payments. Any plans to harness nuclear energy will also require local supplies of fuel to come online, another much needed investment (requiring yet more energy). The inability to source non-Russian fuel has delayed Bill Gate’s TerraPower nuclear power plant construction plans until 2030 (read more here).

We also spoke about the continued strength of the gold market in 2024. Central bank buying has been a key driver of demand. In 1Q24, central bank purchases set a record, following strong buying in 2022 and 2023.

Despite all their buying, few central banks have much of their reserves in gold. If the countries below starting with Australia and moving to the right were to top up their gold holdings to just 10% of reserves, they would need to purchase roughly 70% of the total gold ever mined to do so.

Even with the run up, gold prices are still about 40% lower than the peak in the last inflation cycle adjusted for inflation and also lower relative to the S&P500 Index.

Meet Your Expert

Grant Johnsey

Grant is responsible for delivering capital market solutions to institutional clients across agency brokerage, transition management, security finance, and foreign exchange.

Northern Trust Securities, Inc.(NTSI), Member FINRA, SIPC and a subsidiary of Northern Trust Corporation. Products and services offered through NTSI are not FDIC insured, not guaranteed by any bank, and are subject to investment risk including loss of principal amount invested. Additional disclosures are included in the link, see http://www.northerntrust.com/ntsidisclosure

Business Continuity Notice- Northern Trust Securities, Inc.