- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Options Quarterly Commentary Q3 2024

U.S. equities ended the third quarter of 2024 with a strong performance, despite elevated market volatility on multiple occasions. Whilst September has historically been the worst performing month for equity markets, the S&P 500 SPX ultimately closed Q3 24 at 5762.48 (up 5.9% vs Q2 24). Volatility throughout the quarter was driven by geopolitical tensions in the Middle East, weak U.S. economic data and uncertainty around Fed rate cuts. The CBOE Volatility Index (VIX) ultimately closed the quarter at 16.73 (up 35.5% v Q2 24), reaching a high of 65 (highest print since COVID) in premarket trading on August 5th. Global markets were shocked when the BOJ unexpectedly raised interest rates, in turn seeing markets violently sell off on the forced unwind of the Yen carry trade. However, markets quickly digested this event as an isolated incident as opposed to a broader macro concern, and equity markets quickly recovered back to all-time highs.

Source: Bloomberg

We saw an additional bout of volatility approaching the FOMC meeting on September 18th, with the options market pricing in a 1.2% swing in either direction for the S&P 500. Following the Fed’s 50 basis point cut the S&P500 closed down –0.29%, with the real volatility ‘payoff’ coming the following day as the S&P500 soared +1.70% to a fresh all-time high. As noted in an article by JP Morgan, a sector rotation occurred during this period with value stocks outperforming growth stocks by 7%, plus a rally in small caps stocks, which typically perform well in low-interest rate environments.

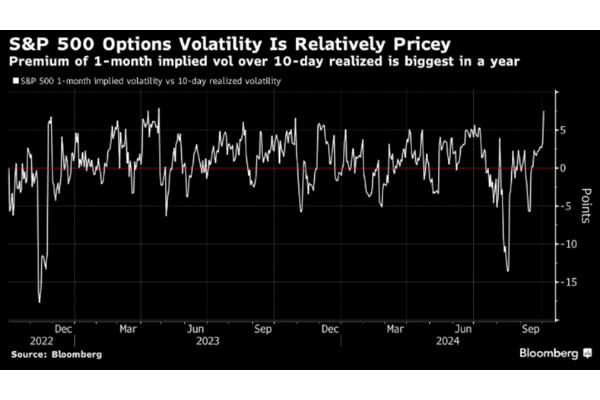

As we head into the fourth quarter, we are likely to see sustained volatility due to continued geopolitical tensions and uncertainty around future Fed cuts and the upcoming U.S. presidential election. According to EqDerivatives, the main driving factor for elevated implied volatility premiums relative to realized volatility is due to the strong performance of the S&P 500. Said another way, on our desk we are seeing many investors’ demand for traditional put buying return to lock in the gains they are sitting on heading into year-end, which has helped push up implied volatility. On the flip side, the NTSI options desk has seen some clients choose to take advantage of this volatility premium through both increased put selling and covered call writing.

Source: Bloomberg

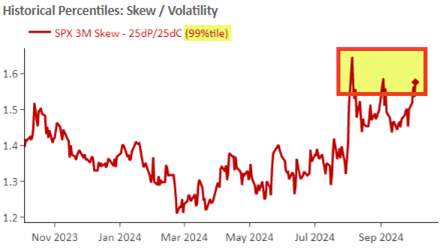

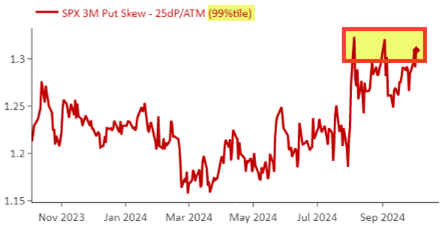

As noted by Nomura, investors are increasingly looking to hedge their portfolios against macro event risk to lock in their positive PnL as we approach year-end. This increased demand for downside protection has caused out of the money put skew to rise to 99% percentile (as illustrated below). Conversely there has been less demand for upside exposure, reducing the 3 month at the money call skew down to 2% percentile.

Source: Nomura

According to the CEO of Parallax Volatility Advisors, with regards to the U.S. election, investors are being patient and so far, there hasn’t been a significant uplift in tail hedging ahead of vote day with the largest flows being mainly from volatility sellers. Analysis from UBS has shown that so far options markets are pricing in an estimate of 2.8% move in either direction the day after the vote and this figure is expected to rise further as we get closer to vote day. Due to the uncertainty over the outcome of the election and implied volatility rising, volatility trades are seemingly more popular than directional ones. As noted by EqDerivatives, historically in election years the VIX tends to increase entering into October, before selling off right before the event and although S&P 500 options are pricing in potential swings on the day immediately after the vote, implied volatility for subsequent days is much lower.

Investors can take advantage of this period of volatility ahead. An article from BlackRock observed that historically, higher volatility has produced higher returns in the short term. When VIX levels are at 12 or below, the SPX returns roughly 5% six months later. As a comparison, when the VIX reaches 29 or higher, the average six-month returns are 16%. Volatility spikes like we have seen over Q3 can create buying opportunities with potential for higher short term returns.

Options involve risk and are not suitable for all investors. Call for a copy of the Options Clearing Corporation (“OCC”) Disclosure Document entitled "Characteristics and Risks of Standardized Options." Please read it carefully before investing.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. This material is directed to professional clients (or equivalent) only and is not intended for retail clients and should not be relied upon by any other persons. This information is provided for informational purposes only and does not constitute marketing material. The contents of this communication should not be construed as a recommendation, solicitation or offer to buy, sell or procure any securities or related financial products or to enter into an investment, service or product agreement in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful. This communication does not constitute investment advice, does not constitute a personal recommendation and has been prepared without regard to the individual financial circumstances, needs or objectives of persons who receive it. Moreover, it neither constitutes an offer to enter into an investment, service or product agreement with the recipient of this document nor the invitation to respond to it by making an offer to enter into an investment, service or product agreement. For Asia-Pacific markets, this communication is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author's employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP, Northern Trust Global Services SE UK Branch and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT, are authorised and regulated by the UK’s Financial Conduct Authority. The Northern Trust Company, London Branch and Northern Trust Global Services SE UK Branch are also authorised and regulated by the UK’s Prudential Regulation Authority. Not all of the products and services mentioned within this material are authorised and regulated by the UK’s Financial Conduct Authority or UK’s Prudential Regulation Authority. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 7th floor, Claude Debussylaan 18 A, 1082 MD Amsterdam; Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE Norway Branch, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651) (NTGL)/Northern Trust Fiduciary Services (Guernsey) Limited (29806) (NTFSGL)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) (NTIFASGL) are licensed by the Guernsey Financial Services Commission. Registered Office: NTGL/NTFSGL -Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. NTIFASGL - Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3QL. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386). Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.