- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Fundamentals Matter

While short-term fluctuations and sudden selloffs have tested the markets, key indicators such as corporate profits, employment data, and economic resilience have held firm.

It has been an eventful past month for the markets. A rotation into U.S. small cap equities gained traction after inflation data came in softer than expected. From a little before mid-July through the end of the month, small caps outperformed large caps by 12%. Over that period, value stocks, real estate and Treasuries performed notably well, too. While those areas produced abnormal gains, broader equities ended the month slightly up as well. However, things took a turn in August. In the span of three days global equities sold off 7%, Japan equities saw more than a 12% one-day loss, and U.S. equities breached the 5% correction threshold. The VIX Index (a measure of U.S. equity volatility) recorded its largest ever intraday spike. While it’s early days, the dust has somewhat settled since. Global equities sit over 3% above the recent trough and volatility levels — while still elevated — have come down.

Associated with the sell-off have been several candidates. Starting in the first half of July, semiconductor stocks have sold off more than 20%. Also, Bank of Japan tightening has corresponded with a sharp appreciation in the yen. This has led to an unwinding of carry trades and potentially leverage elsewhere. Adding fuel to the fire was softer than expected U.S. employment data that elicited heightened growth concerns. We do not attribute recent volatility to a change in fundamentals. The increase in the U.S. unemployment rate was driven by increased supply. Layoffs have remained low and job demand remains intact by historical standards. Corporate profits remain solid with second quarter earnings season shaping up reasonably well. We, along with consensus, expect ~13% earnings growth for U.S. equities over the next 12 months.

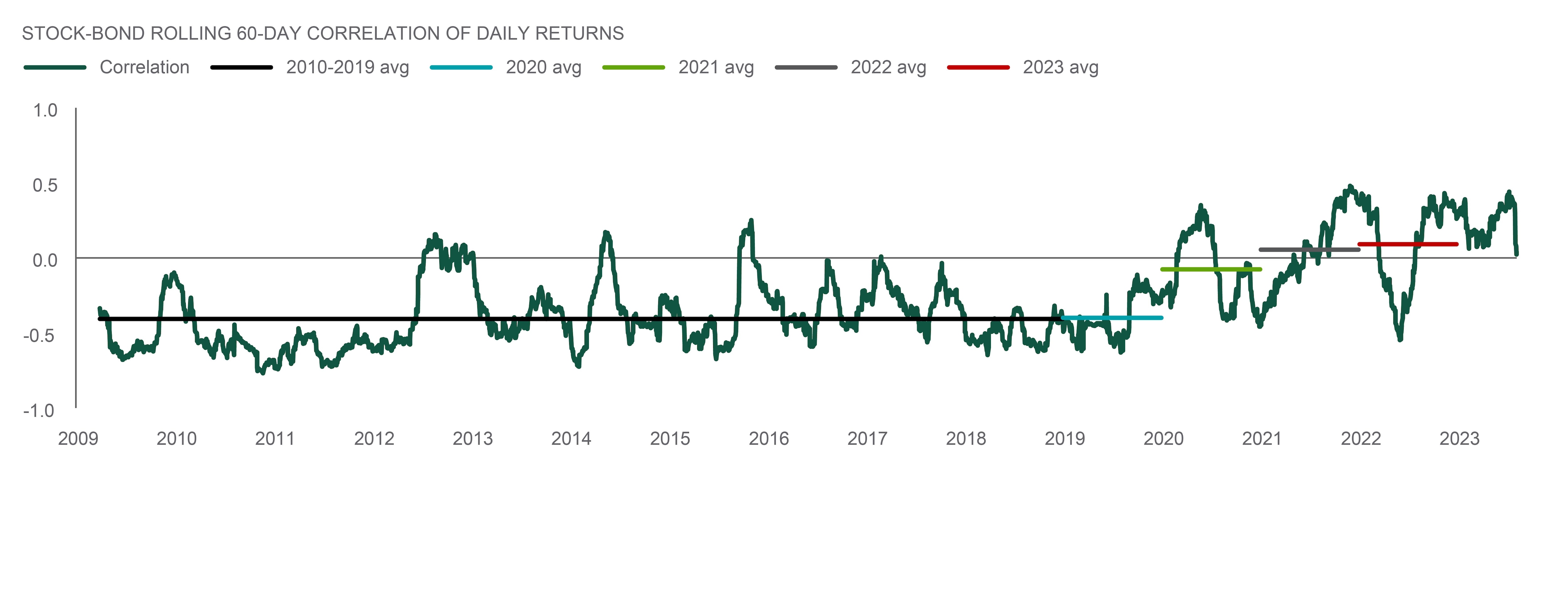

Lingering volatility is certainly possible through year end. Volatility is a normal part of market cycles, with 5% corrections occurring five times per year on average. During these periods, diversification can help buffer losses. Across the recent three-day 7% selloff in global equities, investment grade fixed income gained 2%. The stock-bond correlation has been rising over the past several years alongside accelerating inflation (see chart). With inflation coming down toward more normal levels, it is possible that a negative stock-bond correlation can continue to serve as a ballast during equity drawdowns.

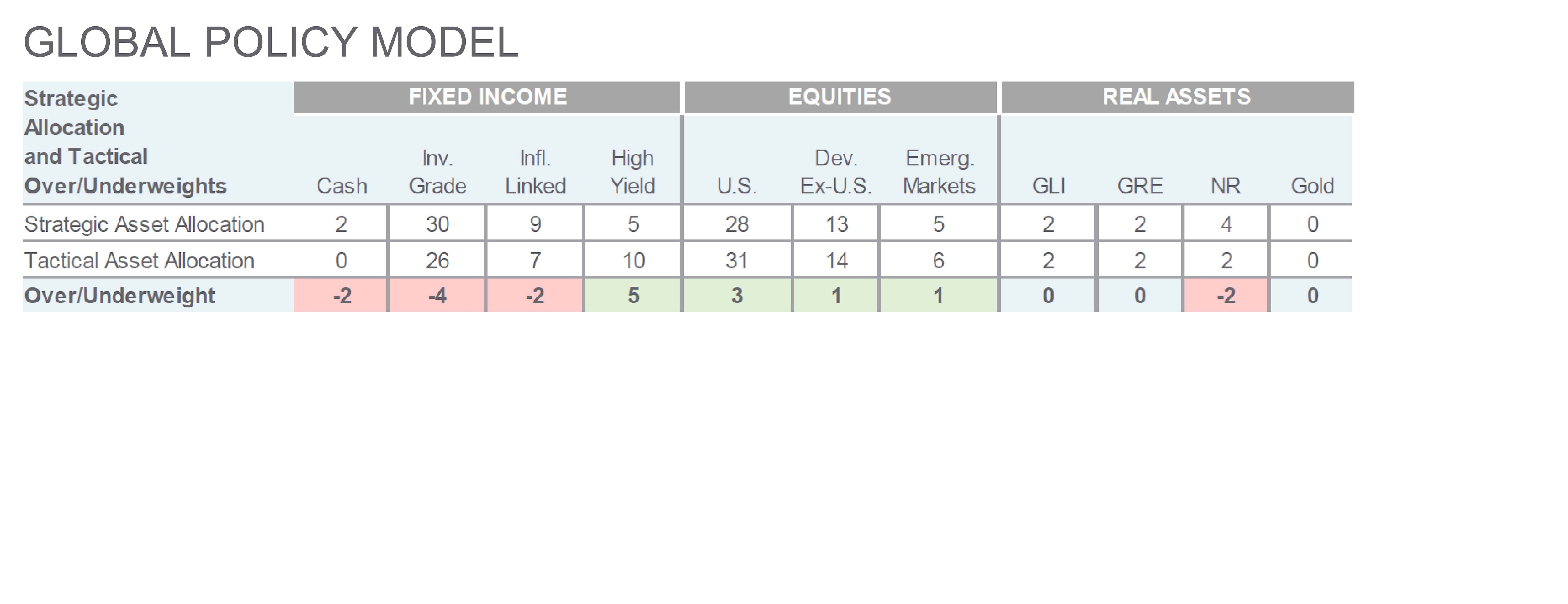

We made no changes to our tactical positioning this month. Recent market developments have not changed our constructive outlook for macroeconomic and corporate fundamentals. Our base case remains for a soft landing and easier central bank policy than in recent years. We maintain pro-risk tactical positioning in the Global Policy Model with a preference for equities over fixed income. Within fixed income, we prefer high yield over investment grade given a supportive economic outlook and cushion from high yield’s income component against adverse moves in rates and/or credit spreads.

— Anwiti Bahuguna, Ph.D. – Chief Investment Officer, Global Asset Allocation

Diversification support

The shift lower in the stock-bond correlation helped contain losses for balanced portfolios during the recent equity selloff.

Source: Northern Trust Asset Management, Bloomberg. Stocks represented by S&P 500 Index; Bonds represented by Bloomberg US Treasury Index. 2010-2019 average (avg) starts 3/30/2010. Trading day data from 12/31/2009 through 8/9/2024.

Interest Rates

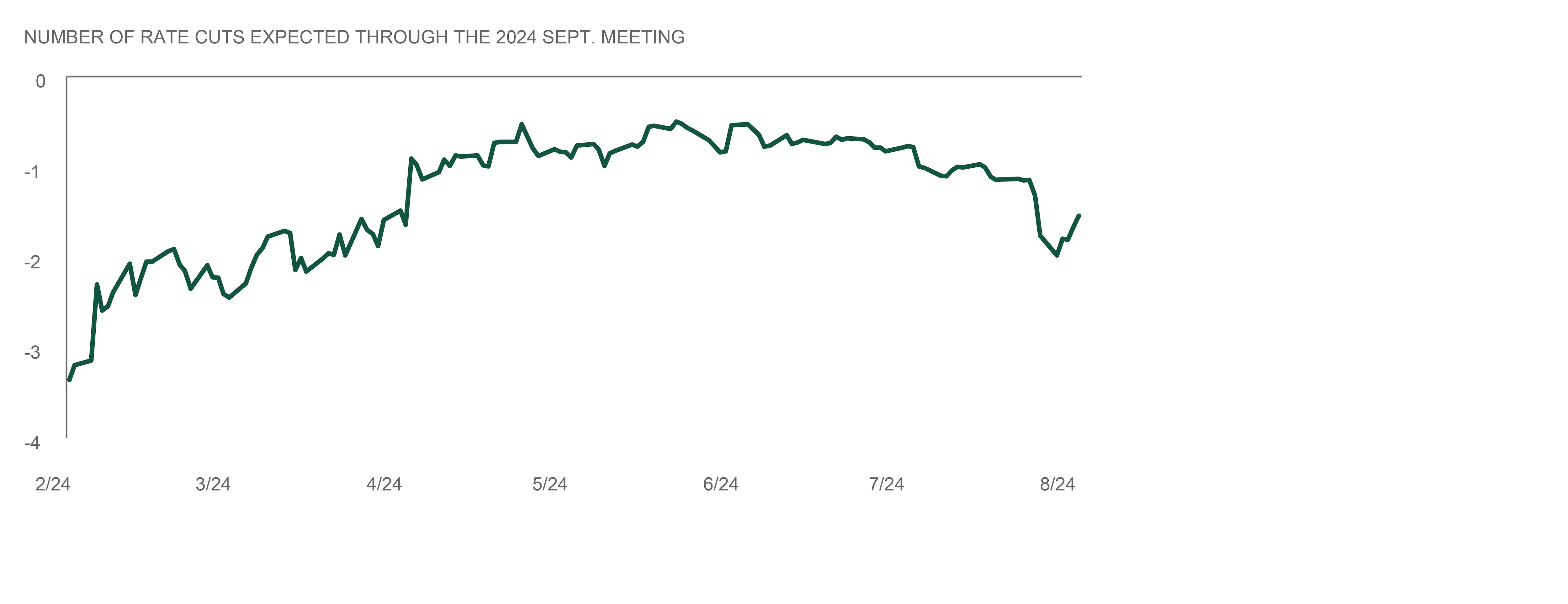

We took the main message from the July Federal Open Market Committee (FOMC) meeting to be that while recent economic data releases have given the Committee greater confidence that inflation is moving sustainably towards their target, they’re also watching the labor market for unexpected weakness.

Regarding inflation, their description was qualified as “somewhat elevated” compared to “elevated” last meeting. Similarly, they observed “some further progress…” towards their 2% objective, compared to “modest further progress” six weeks ago. Regarding the labor market, job gains “moderated,” instead of “remained strong,” and the unemployment rate “moved up but remains low,” instead of “remained low.” Perhaps most notably, the statement added that the “Committee is attentive to the risks to both sides of its dual mandate.” This is a sharp contrast to the language the Committee has used over the past couple of years, which indicated that “the Committee remains highly attentive to inflation risks.” Overall, the market did not appear to view the July FOMC meeting as a game-changer. Market participants have likely already turned their attention to upcoming data releases and the annual meeting of senior central bankers in Jackson Hole.

— Dan LaRocco, Head of U.S. Liquidity, Global Fixed Income

MOVING CLOSER

The Fed is widely expected to cut rates in September.

Source: Northern Trust Asset Management, Bloomberg. Estimated number of moves priced in to the current forward-curve structure for the U.S. using the futures model. Data from 2/8/2024 through 8/9/2024.

- The FOMC is moving closer to policy normalization.

- We, along with the market, expect the first cut in September. We expect a 25-basis point cut.

- We remain underweight investment grade fixed income and see little downside to interest rates from here.

Credit Markets

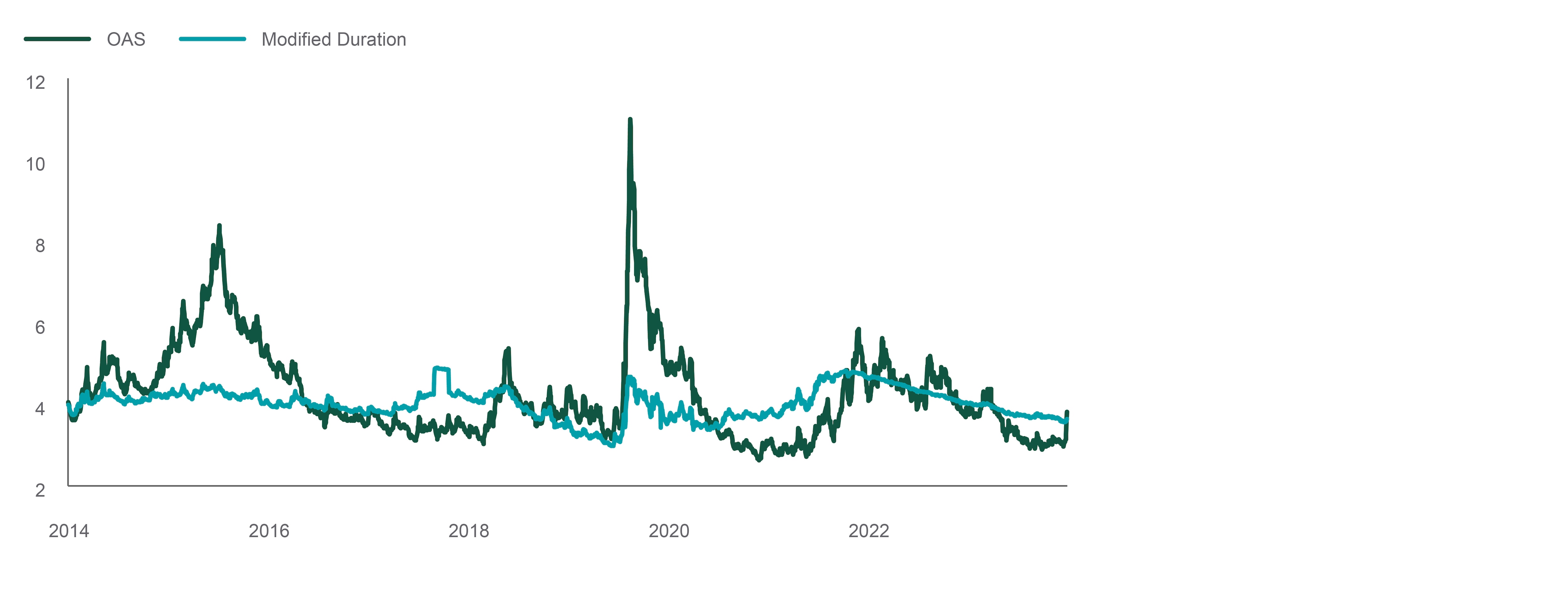

High yield (HY) spreads remain tighter than historical averages. An often overlooked contributing factor is that HY duration is much shorter than in the past. Duration and credit spreads typically are upward sloping as investors demand additional compensation for loaning money for an extended period. Therefore, the decrease in the duration of the asset class usually leads to tighter spreads.

Duration in HY is decreasing due to a number of reasons. One is because most high yield bonds have a call feature. As bonds continue to rally, they begin trading to call prices and can be called before maturity by the issuers — which leads to a decrease in duration. Another aspect is new issuance has been oriented toward shorter duration paper. Companies prefer to lock in today’s higher levels of funding for shorter periods of time. Most of the duration for the asset class also comes from higher quality issuers who have been more opportunistic in letting maturities roll off. Recent U.S. jobs data led high yield spreads to widen significantly due to the sharp rally in rates, but given these structural shifts in the asset class and better fundamentals than historical norms, this may be an attractive entry point.

— Eric Williams, Head of Capital Structure, Global Fixed Income

STRUCTURALLY TIGHTER SPREADS?

Shifts in high yield duration are leading to tighter spreads.

Source: Northern Trust Asset Management, Bloomberg. OAS = option-adjusted spreads. Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. Data from 8/7/2014 through 8/5/2024.

- High yield spreads have continued to be range bound for much of this year. Spreads remain tighter than historical averages.

- The high yield index duration is materially shorter than in the past, helping drive tighter spreads.

- High yield remains our largest tactical overweight.

EQUITIES

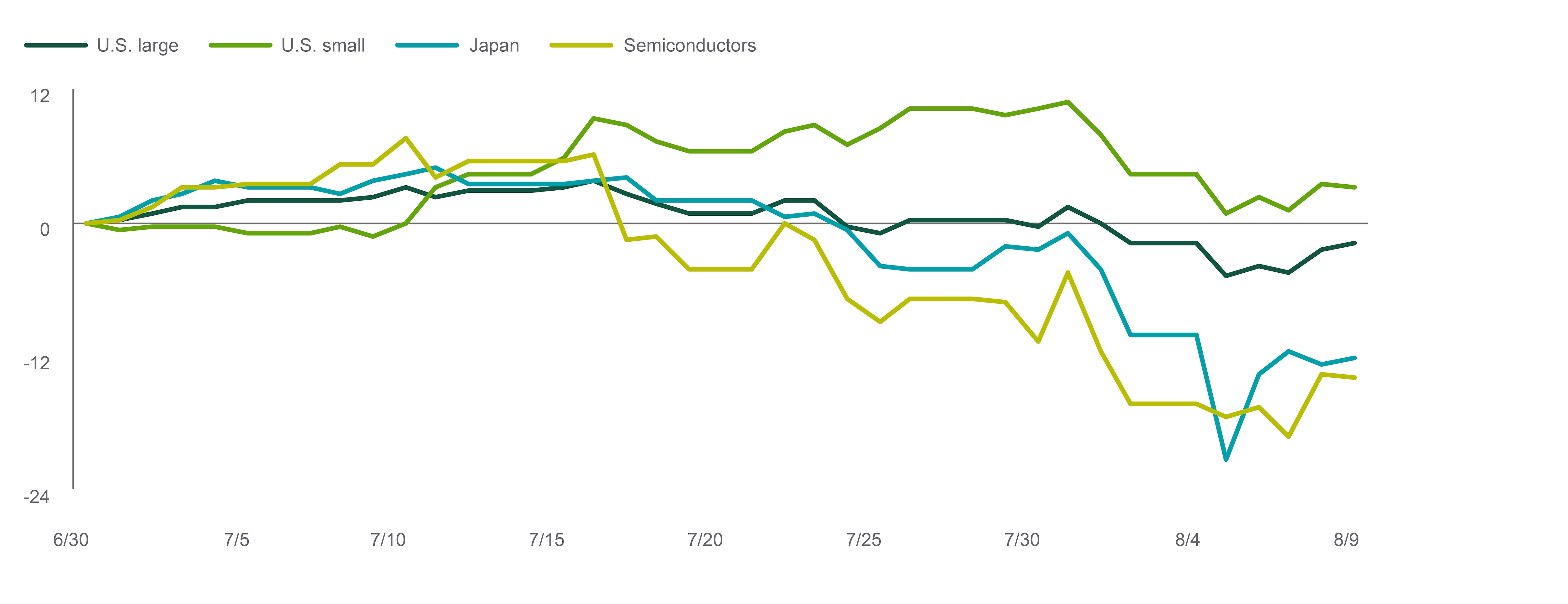

In July, U.S. small caps saw an abnormal gain of 10.8% compared to 1.2% for large caps. Consistent with past small cap rallies, the gains were quick and sharp. Returns were driven by higher valuations. Small cap revenue and earnings expectations remain subdued versus large caps. July’s solid returns quickly reversed in August. Through August 9, global equities sit 3.6% lower on the month. The small cap rally has at least momentarily reversed with U.S. small caps down 6.9% compared to 3.2% for large caps. At the forefront of the drawdown have been Japan equities and semiconductor stocks, both of which have corrected over 20% from July highs (see chart). The peak-to-trough global equity drawdown has been more contained at ~9%.

Recent market events have not altered our constructive fundamental views on a soft landing and solid corporate profits. Market corrections are a normal part of market cycles, with 5% corrections occurring ~5 times per year on average (~1.5 times for 10% pullbacks). While there have been early signs of stabilization, enduring volatility is not off the table. But with equity valuations now lower, sentiment less stretched and supportive fundamentals intact, we reaffirmed our overweight equity positioning.

— Colin Cheesman, Investment Strategist, Asset Allocation

WHAT GOES UP CAME DOWN

Global equities sold off after a small cap rally in July.

Source: Northern Trust Asset Management, Bloomberg. Total return data from 6/30/2024 through 8/9/2024. Past performance is not indicative or a guarantee of future results. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index..

- In July, small caps delivered a 10.8% return compared to 1.2% for large caps.

- The rally sputtered in August alongside the unwind of carry trades and softer-than-expected economic data. Japan and semis were among the notable laggards.

- We do not believe the selloff reflected a major fundamental deterioration or imbalance. We remain overweight all three of the major equity regions

REAL ASSETS

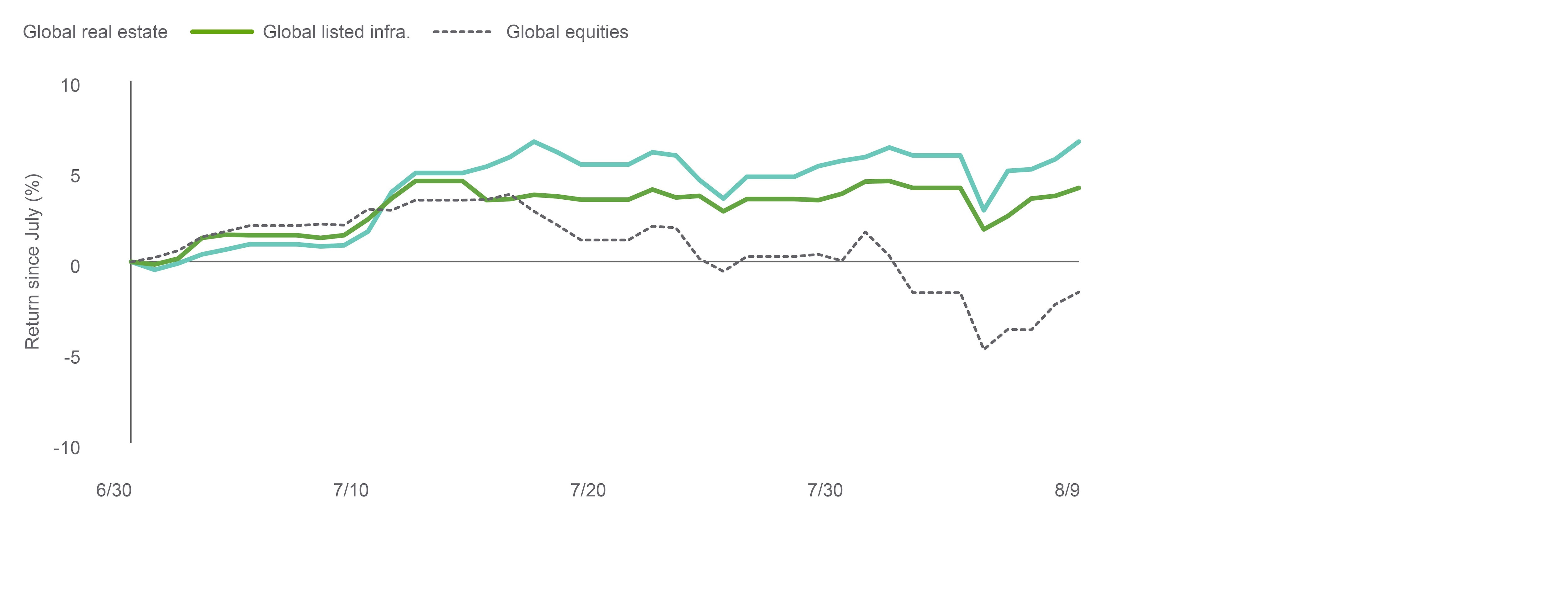

With the backdrop of widening breadth in the stock market coupled with the expectation that the Federal Reserve will be easing into the end of the year, Global Real Estate (GRE) and Global Listed Infrastructure (GLI) outperformed the broader equity market in July. The outlook for infrastructure appears to be improving. The sector enjoys tailwinds from multiple areas: defensive cash flows, expectations of lower rates, and positive fundamentals with strong growth from increasing demand for global power driven by the growing computational requirements of AI. These positive fundamentals are expected to lead to high single-digit earnings growth over each of the next few years. Further, GLI screens historically cheap on a valuation basis, which bodes well for its expected longer-term performance.

Real estate may face some headwinds if global growth significantly slows. Like GLI, the asset screens cheaply on a valuation basis, but unlike GLI, GRE earnings may not be able to keep up with broader equities. Over the next 12 months, GRE is expected to grow earnings at 2 – 3%, while broader equities are expected to grow in the low teens.

— Jim Hardman, Head of Real Assets, Multi-Manager Solutions

REAL RESURGENCE

GRE and GLI have beaten broader equities recently.

Source: Northern Trust Asset Management, Bloomberg. Data from 6/30/2024 through 8/9/2024. Past performance and historical trends are not predictive of future results. Index performance returns do not reflect any management fees, transaction costs or expenses. Indexes are gross of fees. It is not possible to invest directly in any index.

- GRE and GLI have returned more than broader equities since the end of June.

- While the infrastructure sector is expected to experience tailwinds and strong earnings growth, real estate is expected to grow earnings more modestly and may face headwinds from a slowing economy.

- We made no changes to our real assets positioning and remain neutral to real estate and infrastructure and underweight natural resources.

Source: Northern Trust Capital Market Assumptions Working Group, Investment Policy Committee. Strategic allocation is based on capital market return, risk and correlation assumptions developed annually; most recent model released 8/9/2023.The model cannot account for the impact that economic, market and other factors may have on the implementation and ongoing management of an actual investment strategy. Asset allocation does not guarantee a profit or protection against a loss in declining markets. GLI = Global Listed Infrastructure, GRE = Global Real Estate, NR = Natural Resources.

Unless noted otherwise, data on this page is sourced from Bloomberg as of August 2024..

IMPORTANT INFORMATION

Northern Trust Asset Management (NTAM) is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited, issued in the European Economic Association (“EEA”) by Northern Trust Fund Managers (Ireland) Limited, issued in Australia by Northern Trust Asset Management (Australia) Limited (ACN 648 476 019) which holds an Australian Financial Services Licence (License Number: 529895) and is regulated by the Australian Securities and Investments Commission (ASIC), and issued in Hong Kong by The Northern Trust Company of Hong Kong Limited which is regulated by the Hong Kong Securities and Futures Commission.

For Asia-Pacific (APAC) and Europe, Middle East and Africa (EMEA) markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. This document may not be edited, altered, revised, paraphrased, or otherwise modified without the prior written permission of NTAM. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. NTAM may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, its accuracy and completeness are not guaranteed, and is subject to change. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on market or other conditions.

All securities investing and trading activities risk the loss of capital. Each portfolio is subject to substantial risks including market risks, strategy risks, advisor risk, and risks with respect to its investment in other structures. There can be no assurance that any portfolio investment objectives will be achieved, or that any investment will achieve profits or avoid incurring substantial losses. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Risk controls and models do not promise any level of performance or guarantee against loss of principal. Any discussion of risk management is intended to describe NTAM’s efforts to monitor and manage risk but does not imply low risk.

Past performance is not a guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by NTAM. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For U.S. NTI prospects or clients, please refer to Part 2a of the Form ADV or consult an NTI representative for additional information on fees.

Hypothetical portfolio information provided does not represent results of an actual investment portfolio but reflects representative historical performance of the strategies, funds or accounts listed herein, which were selected with the benefit of hindsight. Hypothetical performance results do not reflect actual trading. No representation is being made that any portfolio will achieve a performance record similar to that shown. A hypothetical investment does not necessarily take into account the fees, risks, economic or market factors/conditions an investor might experience in actual trading. Hypothetical results may have under- or over-compensation for the impact, if any, of certain market factors such as lack of liquidity, economic or market factors/conditions. The investment returns of other clients may differ materially from the portfolio portrayed. There are numerous other factors related to the markets in general or to the implementation of any specific program that cannot be fully accounted for in the preparation of hypothetical performance results. The information is confidential and may not be duplicated in any form or disseminated without the prior consent of (NTI) or its affiliates.

Forward-looking statements and assumptions are NTAM’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Not FDIC insured | May lose value | No bank guarantee