- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

MSCI Index Rebalances: Newly Eligible Shares Driving Weight Changes

We examine how newly eligible shares and evolving criteria are reshaping MSCI index weightings and regional allocations.

KEY POINTS

What it is

We review the latest quarterly adjustments to the MSCI World Index and MSCI Emerging Markets Index, highlighting key changes.

Why it matters

Understanding how these rebalances impact sector or regional exposure is crucial for investors who rely on indexes for benchmarks or passive investment strategies.

Where it's going

The MSCI rebalance sets the stage for future opportunities and challenges, as shifting regional weights may redefine investment strategies and global market engagement in the evolving landscape.

MSCI boosted India’s weighting in the MSCI Emerging Markets Index and reduced China’s in its latest quarterly rebalance effective on Monday, November 25, continuing rebalance trends from the past several quarters. India’s weighting sits at 18% from 8% in 2020 while China has continued dropping and now sits at 25% from a peak of around 40% in 2020.

Between the MSCI Emerging Markets Index and the MSCI World Index, MSCI added 22 companies and removed 57. Along with adds and deletes, the broader rebalance triggers a significant amount of trading activity given an estimated $16.5 trillion in assets benchmarked to MSCI equity indexes as of June 30, 2024.1

The overall turnover for MSCI World was 0.57% (one way), which brought the total rebalance related turnover to 2.36% for 2024. The turnover numbers for MSCI Emerging Markets1 were 1.26% for November and 5.55% for 2024 rebalances. While implementing rebalances in index strategies, portfolio managers focus on minimizing the cost and tracking error to avoid wealth erosion throughout the event. Additionally, investors in active strategies who use indexes for benchmarks need to reassess their exposure to specific sectors or regions because of changes in index composition.

MSCI World: Buffett sells Apple, Spotify newly eligible

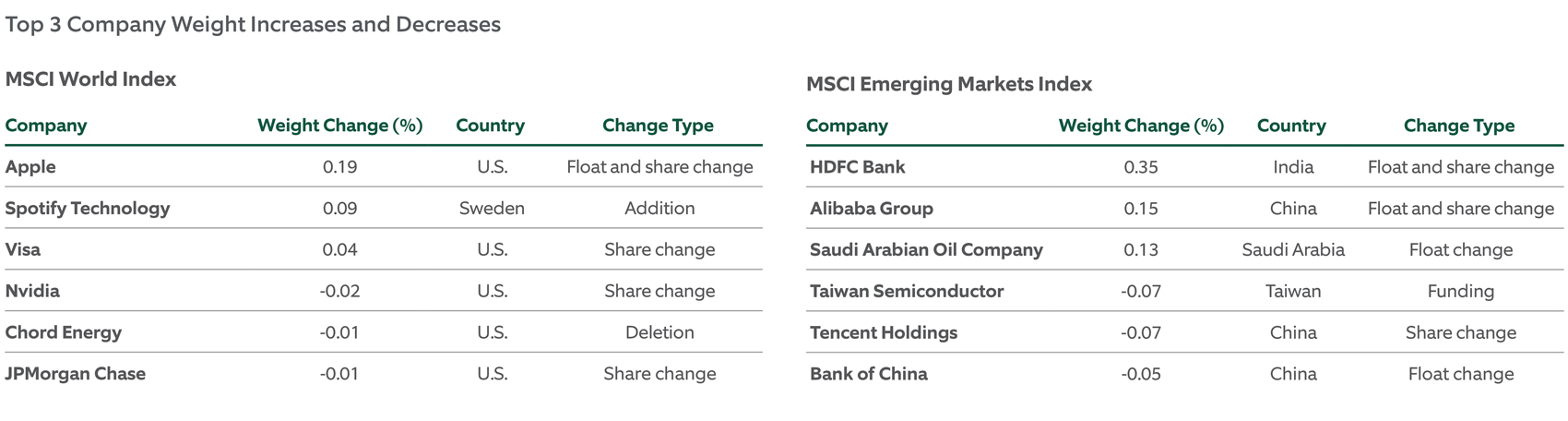

MSCI added 10 companies to and removed 21 companies from the MSCI World Index, representing a somewhat benign 0.34% in turnover. The largest addition was Spotify, the Swedish audio streaming company. The company’s primary listing is in the United States, but following the November 2024 Index Review, foreign listings became eligible for inclusion and thus Spotify was added at a 0.09% weight. Carvana was another notable addition. Due to a country change from the United Kingdom to the Netherlands, the online auto platform qualified for inclusion to MSCI Netherlands and thus MSCI World at a 0.04% weight (see Exhibit 1 – Carvana just outside top 3 weight changes).

Although not an add or delete, another notable weighting change is Apple, which saw its weight increase to 0.19%. This was a result of a float increase – Berkshire Hathaway reduced their holdings and those shares became included in the stock’s free float. Other index providers (such as S&P Dow Jones) have already adjusted their free floats for the technology giant.

MSCI Emerging Markets: India continues to benefit from rebalances, Aramco float increases

MSCI added 12 companies to and removed 36 companies from the MSCI Emerging Markets Index, representing a 0.74% in turnover. All of the additions came from the Asia-Pacific region and represented 0.42% overall. As seen in previous rebalances, the majority of the deletes came from China, accounting for 20 of the 36 names. MSCI removed Chinese companies because they failed to meet higher requirements for free float adjusted market capitalization set by MSCI’s methodology. On the addition side, the largest addition was Taiwanese game maker International Games, which was added at a 0.09% weight. Notable float changes included HDFC and Aramco following share offering earlier in the summer. The vast majority (>97%) of Aramco shares remain excluded from the investible float, so only $43.2 billion of the company’s full float of $1.8 trillion is currently included in MSCI Emerging Markets.

EXHIBIT 1: FLOAT AND SHARE CHANGES DRIVE THE BIGGER WEIGHT CHANGES

Outside of Spotify, the biggest single name changes were driven by changes in free float and, to a smaller degree, share changes.

Source: MSCI, Bloomberg, Northern Trust Asset Management. Weightings as of November 6, 2024 in U.S. dollars. The float is the amount of shares available to the public, which may change because of transactions by insiders. Share changes may occur as companies issue or repurchase shares. Index holdings are provided for information only and should not be construed as a recommendation of any security. It is not possible to invest directly in any index.

Countries: Sweden benefits from methodology change while India keeps adding constituents

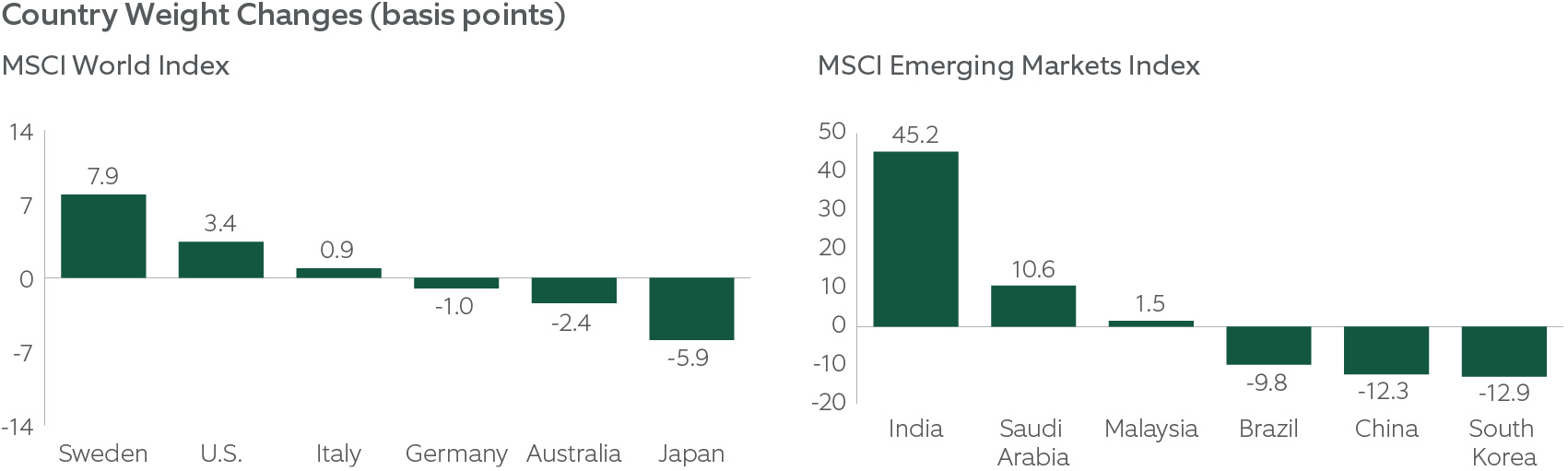

In the MSCI World Index, the rebalance caused modest changes to country weights. Notably, the U.S. weighting rose 0.17% and Sweden jumped 0.08%. Meanwhile, Japan saw its weight decrease a modest 0.06% with no notable individual stock changes. No other countries changed by more than 2.5 basis points (bps).

The rebalance caused more significant changes in country composition to the MSCI Emerging Markets Index, reflecting some stock specific moves. Notably, India’s weight increased by 0.45%, similar to last quarter’s rebalance, although the increase was largely confined to HDFC Bank which saw more shares eligible due to changes in foreign ownership. The largest country decliners were China and Korea, where the 0.12% declines in each country were spread across multiple stocks.

EXHIBIT 2: INDIA CONTINUES BENEFITING FROM INDEX REBALANCES

The benchmark’s weight to India increased by 0.45%, similar to last quarter’s rebalance.

Source: MSCI, Bloomberg, Northern Trust Asset Management. Weightings as of November 6, 2024 in U.S. dollars.

Sectors: Information Technology Shifts Composition

In the MSCI World Index, sector weightings shifted slightly. Information technology and communication services increased by 0.17% and 0.03%, respectively. Within information technology, as mentioned, Apple’s float change drove the majority of the increase, with Nvidia seeing a small weight decrease of 0.02% due to its index shares changing. In the MSCI Emerging Markets Index, financials and energy saw the biggest increases with HDFC Bank (+0.35%) and Saudi Aramco (+0.13%). Materials and information technology were the biggest decliners.

EXHIBIT 3: FLOAT CHANGES DRIVING SECTOR CHANGES ACROSS WORLD AND EMERGING MARKETS

As with countries, single name float changes also meaningfully impacted sector weights in both MSCI World and MSCI Emerging Markets.

Source: MSCI, Bloomberg, Northern Trust Asset Management. Weightings as of November 6, 2024 in U.S. dollars.

Performance Analysis: Adds Outperformed Deletes

As expected, we observed substantial trading during the rebalance period from the November 6 MSCI announcement of the rebalance details to the Monday (November 25) effective date of the rebalances, peaking on the effective date. Indexers do most of their buying at or near the close of effective day because their objective is to match the risk-return characteristics of the benchmark. However, because these rebalances are publicly known, other market participants will take on risk in an aim to profit from rebalance activity. Therefore, we often see stocks of added companies having “buy” pressure post announcement and into effective date while those of deleted companies experience the opposite effect. Intuitively, but not always in reality, the market impact of these flows can lead to adds (deletes) outperforming (underperforming). Should the intuition play out, we refer to outperformance of companies as “right way”, in line with expected flows in (buys) and out (sells) of the indexes. We analyzed to what extent performance went the right way for the adds and deletes for indexes during the rebalance period.

MSCI World Index

Adds rose 11.9% while deletes lost 2.5%, leading to a significantly positive spread of 14.4%. Most notable among adds was the performance of Spotify, which added at a 0.09% weight. Spotify rose 23% from announcement to effective day, including an 11.4% gain on November 13 as the streaming music company gained more premium subscribers than expected. Excluding Spotify, adds still outperformed deletes by 6%, which was an impressive result overall.

Although not an add or delete, Apple’s performance was also notable, as the ubiquitous information technology company was the largest weight increase, and the stock shot higher 1.3% over the last 15 minutes of trading and closed near session highs on the effective date.

MSCI Emerging Markets Index

Additions outperformed deletes by 5.9% in the MSCI Emerging Markets Index. Among the deletes, there were several names in Asia-Pacific Region that significantly underperformed over the announcement to effective date, including a 30% drop from Korean information technology company CosmoAM&T, which dropped pretty consistently although rallied 4.3% on effective day.

Focusing on the additions in India and the deletions in China, the five Indian adds were down 2.8% from announcement to effective date, actually underperforming the broader MSCI India Index which was only down 1.6% over the same period. And regarding China, the 20 Chinese deletes were down 2.0% from announcement to effective date, significantly outperforming MSCI China which was down 7.3% over the same period. Thus, while the add-delete spread was “right way”, overall, controlling for countries actually reveals a different picture across these two countries.

Exhibit 4: “Right Way” Performance

Companies added outperformed those deleted from the MSCI World and MSCI Emerging Markets Index during the rebalance period from November 6 to November 25. We call this “right way” performance because it is in line with index fund flows that need to “buy” the additions to the indexes and “sell” deletions out of the indexes.

Source: MSCI, Bloomberg, Northern Trust Asset Management, from November 6, 2024 to November 25, 2024. Add and Delete baskets are weighted based on market capitalization.

What the Rebalance Means to Investors and Index Managers

Index portfolio managers must remain vigilant during these periods to achieve the investment objective of replicating the risk and return metrics of the index and minimize tracking error. From an index tracking perspective, we believe it is crucial to understand the dynamics that surround an index rebalance — liquidity, risk environment, stock- specific news, and offsetting trade flows — to guide index portfolios through these kinds of events with as little wealth erosion as possible.

IMPORTANT INFORMATION

Northern Trust Asset Management (NTAM) is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited, issued in the European Economic Association (“EEA”) by Northern Trust Fund Managers (Ireland) Limited, issued in Australia by Northern Trust Asset Management (Australia) Limited (ACN 648 476 019) which holds an Australian Financial Services Licence (License Number: 529895) and is regulated by the Australian Securities and Investments Commission (ASIC), and issued in Hong Kong by The Northern Trust Company of Hong Kong Limited which is regulated by the Hong Kong Securities and Futures Commission.

For Asia-Pacific (APAC) and Europe, Middle East and Africa (EMEA) markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. This information may not be edited, altered, revised, paraphrased, or otherwise modified without the prior written permission of NTAM. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. NTAM may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, its accuracy and completeness are not guaranteed, and is subject to change. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on market or other conditions.

All securities investing and trading activities risk the loss of capital. Each portfolio is subject to substantial risks including market risks, strategy risks, advisor risk, and risks with respect to its investment in other structures. There can be no assurance that any portfolio investment objectives will be achieved, or that any investment will achieve profits or avoid incurring substantial losses. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Risk controls and models do not promise any level of performance or guarantee against loss of principal. Any discussion of risk management is intended to describe NTAM’s efforts to monitor and manage risk but does not imply low risk.

Past performance is not a guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by NTAM. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For U.S. NTI prospects or clients, please refer to Part 2a of the Form ADV or consult an NTI representative for additional information on fees.

Forward-looking statements and assumptions are NTAM’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Not FDIC insured | May lose value | No bank guarantee