- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Soft Landing Takes Shape

The Northern Trust Economics team shares its outlook for U.S. growth, employment, inflation and interest rates.

We enter the fourth quarter with fundamentals falling nicely into line. Uncomfortable inflation and the overheated job market appear to be in the past, and they are cooling without dragging the economy into contraction. An easing cycle is underway, with questions centered not on if rates should fall, but rather, how far and how fast. While it is too soon to declare victory, the soft landing is close at hand.

We remain mindful of the risks to the outlook. This cycle has reinforced the old lesson that inflation can appear settled, only to take off again unexpectedly. Oil prices are volatile, reflecting heightened risks in the Middle East. Hurricane season has been especially severe, with damages still being assessed. The election casts a shadow of uncertainty, sidelining investment until the political landscape is clearer.

Following are our thoughts on recent data and developments.

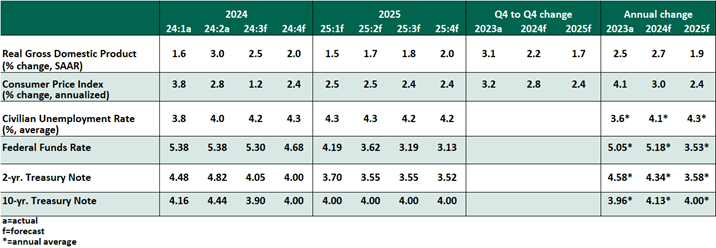

KEY ECONOMIC INDICATORS

Influences on the Forecast

- The September employment report bucked the trend of slower hiring that had caused concern over the summer. Payroll gains of 254,000, plus upward revisions to weak readings in prior months, showed that strength remains in the labor market. Gains in the household survey brought the unemployment rate down one tenth to 4.1%. We do not believe the market is reheating, but rather, coming into balance. We are tracking the risk of wage-driven inflation, as average hourly earnings stepped up to 4.0% year over year.

The past three readings of the hiring rate (hires as a share of total employment) have settled at a low level last seen in 2014. The rate of quitting (voluntary departures) is also at a nine-year low. Turnover is a component of a healthy labor market; such moribund rates of activity could indicate more cooling ahead.

The dockworkers’ strike at the start of October was too brief to cause lasting economic harm but shows that labor disruptions are still possible.

- Inflation remains on an uneven path toward a cooler steady state. The September consumer price index (CPI) notched an annual gain of 2.4%, its lowest reading in over three years. Shelter prices grew 4.8% year over year, the first reading under 5% since the inflationary cycle commenced. However, food prices showed some reflationary strength, while core inflation (excluding food and energy) is stuck at 3.3% year over year, led by services.

- In prepared remarks, Federal Open Market Committee (FOMC) members have been noncommittal about the path of easing ahead. Given the reports of strength in labor and adequate improvement in inflation, there is no need for the FOMC to hurry their easing. We expect a cadence of 25 basis point cuts at each meeting until a rate of 3.0% is reached in the middle of next year. With inflation still above target and employment tapering, risks to the outlook for monetary policy are balanced.

- An anomaly in U.S. output data was resolved with revisions to the National Income and Product Accounts. Growth in gross domestic income (GDI) had fallen below growth in gross domestic product (GDP). The two measures should arrive at similar trends, and the divergence was seen as a potential sign of latent weakness in the U.S. economy.

Contrary to fears, a more complete accounting showed that personal income and savings had been underestimated, a sign that the economy had more strength than initially estimated. The saving rate was revised up by 2%, which suggests healthier household balance sheets.

- Two severe hurricanes made landfall in recent weeks, following atypical routes over the continent. The economic consequences of such events are locally severe but tend not to drag national measures down significantly. Data in coming months may indicate elevated unemployment as workers are temporarily unavailable.

- At the start of the month, the reference Secured Overnight Financing Rate (SOFR) settled above the Fed Funds target range, and the Fed’s standing repo facility was drawn for the first time since its creation in 2019. Liquidity has become less abundant. Recurring spikes in SOFR may signal that the time is right to end the Fed’s balance sheet paydown.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.