- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Allocating to Alternatives

Alternative investments can improve risk-adjusted returns and future goal funding outcomes. But investors must thoughtfully select hedge funds and bear systematic risk while funding commitments to private investments.

By Peter Mladina, Executive Director of Portfolio Research, Wealth Management

David Moore, CFA, CAIA Director of Manager Research Wealth Management

Charles Grant, CFA, Director of Asset Allocation Research Wealth Management

Although private investments and hedge funds are both alternative investments, they have very different roles in a portfolio. Private investments can enhance portfolio returns,1 whereas select hedge fund strategies can diversify portfolio risk.2 Together, they can improve the risk-adjusted return of a portfolio — i.e., its efficiency ratio, defined as the portfolio’s expected return divided by its risk (standard deviation). Private investments can increase the numerator of the efficiency ratio by boosting the portfolio’s expected return. Select hedge fund strategies can reduce the denominator of the efficiency ratio by reducing the portfolio’s risk through uncorrelated (diversifying) returns.

These benefits largely come from alpha (risk-adjusted excess return), so capturing them requires bearing some illiquidity and active risk. It is common for investors to seek alpha by hiring active managers in public equity, but there is no evidence of manager skill net of expenses in public equity.3 In contrast, the opportunity set for alpha is far greater in alternative investments — particularly private investments. And capturing alpha from alternative investments benefits the portfolio’s risk-adjusted return far more (and far more reliably) than capturing alpha from public equity. So spend your active risk budget — your appetite to hire active investment managers — on alternative investments. And consider low-cost, passive implementation for traditional stocks and bonds.

Asset allocation is the most important decision in portfolio construction. If assets serve the purpose of funding lifetime goals, then the optimal asset allocation solution must incorporate both assets and goals. The standard 60% stock/40% bond portfolio and its variants are increasingly being replaced by customized goal-aligned portfolios, composed of dynamic allocations to risk-control (goal-hedging) and risk-asset (return-seeking) sub-portfolios. As part of risk-asset sub- portfolios, alternative investments can improve the funding of partially hedged and unhedged goals. Private investments, through return enhancement, can decrease the present value needed to fund future goals. Select hedge fund strategies, through risk diversification, can decrease the dispersion (risk) in future goal-funding outcomes.

The market portfolio of capital assets is a good benchmark for asset allocation as it captures the collective decision-making of all asset allocators.4 To determine the recommended mix of alternative investments within risk-asset sub-portfolios, we look to relative equilibrium market weights as a good starting point.

From there, we find an “optimal” weight based on a combination of Northern Trust (pre-tax) capital market assumptions and an active risk budget as seen in Exhibit 1:

For suitable investors, the risk-asset model has flexibility to further increase alternative investment allocations within a risk-constrained maximum range. Higher allocations to alternatives generally start with private investments because of higher return potential and a larger opportunity set for alpha. But a portion of expected return enhancement is compensation for illiquidity, a primary risk to goal funding, so oversized allocations to private investments are more appropriate for investors with long-term goals, significant wealth transfers or large surplus assets. Successful goal funding also requires having sufficient cash on hand at the necessary time. Select hedge funds can provide diversifying sources of return to reduce volatility and make final payouts more certain for nearer term goals.

While hedge funds tend to be fairly liquid with relatively straightforward implementation, the funding of private investments through closed-end funds tends to present unique considerations. In addition to the typical diversification considerations within balanced portfolios (e.g., by asset class, geography, manager, etc.) private investment programs should also account for vintage year diversification as there can be a wide dispersion of returns from vintage to vintage (even when selecting top performers within a given vintage). Therefore investors should be mindful of not only selecting quality managers, which has proven to be critical in delivering good outcomes, but also deciding when to make commitments.

After capital is committed to a closed-end fund, the manager is typically required to deploy the fund’s capital within an investment period of a few years and must ultimately exit the fund’s investments by the end of a finite period (or term). But the manager is subject to unknown market conditions, into which they must invest and which they must ultimately exit, to realize returns. And market timing can be difficult. So instead of trying to market-time the best entry point for a single allocation, an investor may find it beneficial to implement and persistently adhere to a commitment pacing program — for example committing 25% of target each year, on average.

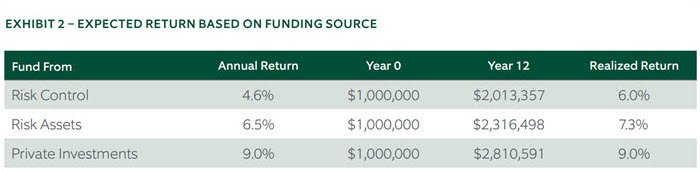

The ongoing nature of funding private investments naturally raises the question of how to best do so while most confidently capturing the enhanced return expectation. We illustrate two approaches in helping frame the decision of whether to fund commitments from risk-control (proxied by investment- grade fixed income) or risk-assets (proxied by global equity) based on Northern Trust capital market assumptions for a 12-year planning horizon (the typical term for a closed-end fund):

Based on Northern Trust’s return forecasts and a proprietary pacing model, funding commitments to private investments from risk-control is forecasted to return 6.0% (annualized) while funding from risk- assets is expected to generate a higher return of 7.3%. The highest expected return (9.0%) comes from an established private investment program that is able to “self-fund” commitments from existing funds’ distributions.

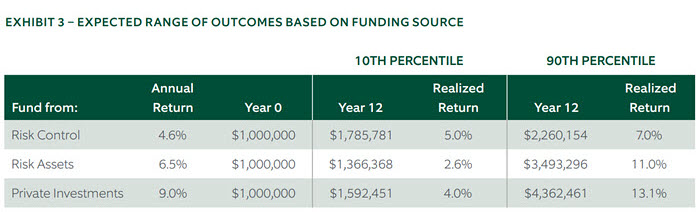

However, future realized returns will likely differ from single point-estimates. To illustrate reasonable ranges in expected outcomes, we ran Monte Carlo simulations using Northern Trust capital market assumptions of return and risk (standard deviation) while making a simplifying assumption that risk-assets have zero correlation to risk-control while being perfectly correlated to private investments (as a less diversified subcategory of risk-assets):

Exhibit 3 shows the 10th and 90th percentile outcomes of a Monte Carlo simulation based on 3,000 trials. The 90th percentile outcomes are fully consistent with Exhibit 2 in that funding from risk-assets results in a higher return (11.0%) than risk-control (7.0%). The 10th percentile outcomes differ with funding from risk-control resulting in a higher return (5.0%) than risk-assets (2.6%), reflecting a wider range in potential outcomes given a higher level of assumed risk for risk-assets than risk-control.

Rational investors understand systematic risk and return are generally related. So in order to maximize the potential return enhancement of private investments, suitable investors must be willing to bear the risk of funding commitments with risk-assets until the private investments program is sufficiently mature to self-fund contributions.

While future commitments are hard-dollar obligations, the preferred funding source (risk-assets) is highly correlated, meaning the target exposure to private investments should generally move in the same direction as its funding source. Furthermore, the appraisal-based nature of private investments typically results in slower movement of asset re-pricing, which can provide additional time to recalibrate a commitment pacing program to private investments. And select hedge funds can provide diversifying sources of return to improve total portfolio efficiency while providing an additional liquidity source within risk-assets as necessary.

1 See “Increase Portfolio Returns with Private Investments,” Northern Trust Research Article (2021)

2 See “Diversify with Select Hedge Fund Strategies – Revisited,” Northern Trust Research Article (2021)

3 See “Manager Performance and Persistence,” Northern Trust Research Article (2022)

4 See “A Benchmark for Efficient Asset Allocation,” Northern Trust Research Article (2017)

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S.

This document is a general communication being provided for informational and educational purposes only. The opinions and conclusions expressed herein are those of the authors and are not meant to be taken as investment advice or a recommendation for any specific investment product or strategy and does not take your financial situation, investment objective or risk tolerance into consideration. Performance examples are hypothetical and for illustration purposes only and actual results may be lower or higher than a portfolio that may be more or less diversified and/or managed in a different manner. In performing its services, Northern Trust will take into account other relevant facts and circumstances such that positions and transactions for any particular client account may differ with the investments described herein. Northern Trust provides fiduciary and investment management services to various types of accounts, including but not limited to, separately managed accounts, registered and unregistered funds. The investment advice given to one client account may differ from the investment advice given to another client account. Northern Trust and its affiliates may have positions in, and may effect transactions in, the markets, contracts and related investments described herein, which positions and transactions may be in addition to, or different from, those taken in connection with the investments described herein. All information discussed herein is current only as of the date of publication and is subject to change at any time without notice. This material has been obtained from sources believed to be reliable, but its accuracy, completeness and interpretation cannot be guaranteed. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining specific legal, accounting or tax advice from their own counsel.

All investments involve risk and can lose value. The market value and income from investments may fluctuate in amounts greater than the market. Forecasts may not be realized due to a multitude of factors, including but not limited to, changes in economic conditions, corporate profitability, geopolitical conditions or inflation.

LEGAL, INVESTMENT AND TAX NOTICE. This information is not intended to be and should not be treated as legal, investment, accounting or tax advice.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS. Periods greater than one year are annualized except where indicated. Returns of the indexes also do not typically reflect the deduction of investment management fees, trading costs or other expenses. It is not possible to invest directly in an index. Indexes are the property of their respective owners, all rights reserved.