- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Argentina’s Shock Therapy

Milei’s radical policies have yielded some progress against the nation's daunting challenges.

By Vaibhav Tandon

In neurology, shock therapy is a course of treatment that can help to counteract severe depression, psychosis, and catatonia. With proper coordination among anesthesiologists, psychiatrists and nurses, the therapy is safe and effective.

In economics, shock treatment involves sudden, intense changes in policy to cure long-running afflictions. While they can produce discomfort, proper coordination among the government, the central bank and the private sector can allow shock therapy to produce improved economic health.

Argentina is trying to shock itself out of a long-running economic malaise.

Argentina’s persistent struggles have made it a candidate for this approach. That is what the self-declared "anarcho-capitalist" and current president Javier Milei has prescribed to halt the country’s decades-old economic malaise.

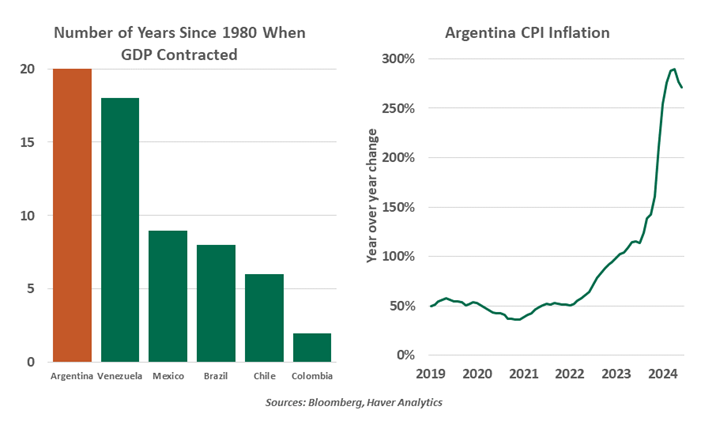

Last December, President Milei inherited a government that had been spending beyond its means for years, an economy that was being choked off by government regulations and financial markets that had endured multiple crises. Foreign reserves were running dry, while inflation was skyrocketing. The Argentine peso (ARS) had endured a dramatic devaluation in the past two decades. Currency and price controls have led to shortages of essentials like rice, while auto manufacturing suffered from a scarcity of the dollars required for imports. Argentina has one of the world’s lowest levels of credit access for households and businesses; the nation has defaulted on its debt on nine separate occasions.

Milei’s radical policies have yielded some positive results, but much work remains to be done.

Milei’s economic blueprint called for slashing government spending, dealing with hyperinflation, lowering interest rates, rebuilding reserves and creating a more market-oriented economy. Primary government spending was cut by 40% in the first quarter of 2024, led by a significant reduction in capital spending and transfers to provinces. Pensions were cut by 36% year-over-year, which contributed the lion’s share of the overall fiscal adjustment.

The peso was devalued from ARS391 per dollar to ARS833 just three days into Milei’s term of office. The devaluation bridged the gap between the official exchange rate and the informal or blue-chip rate, used to get around strict capital controls. More recently, reforms were passed to allow deregulation, privatization, and promotion of private investments in large projects.

Curbing unchecked printing of money has allowed the government to post its first budget surplus in 16 years. It has also helped cool monthly inflation to 4% in July from a three-decade high of about 26% at the end of last year. The central bank has cut interest rates six times since last December, bringing the policy rate down to 40%. While still low and insufficient to settle the large debt owed to importers, the central bank has been able to boost gross reserves.

That said, much of the broader macroeconomic mess remains. The immediate cost of austerity was a deep recession. Protests against Milei’s program have grown in recent months, as Argentines struggle to feed their families. Government agencies have been closed, costing thousands of jobs. Public works have come to a halt.

The policy rate of 40% remains far below the annual inflation rate, discouraging Argentines to save in pesos. The government has failed to remove capital controls, which restricts the ability of investors to get money out of the country. Foreign direct investment is still virtually non-existent.

Milei’s radical plan to fix the deep-rooted problems of Argentina’s economy has had some success, and it is being watched by other countries facing comparable challenges. But there is still much work to be done. Given the frail social landscape, the president needs to deliver more progress. If stakeholders cannot remain aligned, shock therapy can be a very risky treatment.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.