- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Auto Sales Slowdown

The pandemic changed how new cars are bought and sold.

By Ryan Boyle

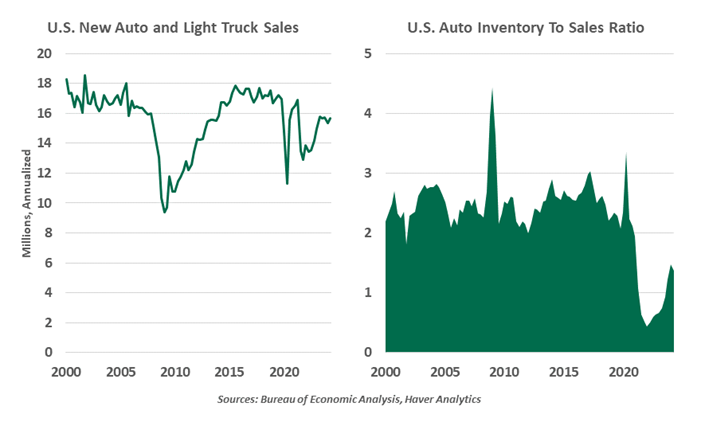

Few parts of the economy were as disrupted by pandemic supply chain challenges as the automotive sector. Input product shortages are now mostly history, but auto sales and inventories have not bounced back to their former pace. From a norm of over 17 million sales in 2015-2019, the U.S. auto industry has yet to sustain an annualized rate of 16 million since the pandemic. Why has the new car market encountered a lower speed limit?

The central issue is affordability. Seasoned car shoppers will recognize the sales tactic of negotiating around a monthly payment, letting buyers think more in terms of an achievable bill rather than one large lump sum. TransUnion reports that average monthly payments on new car loans rose from $600 in 2021 to $743 in 2023, holding steady since. Loan terms had already stretched as far as seven years to keep buyers within their budgets.

High interest rates are working as expected in the auto sector.

Payments are a combination of principal and interest. After many years of very low interest rates—where even 0% offers felt commonplace—financing is no longer cheap. The average four-year new car loan rate from a bank rose from 3.5% at the start of 2022 to 7.7% two years later. Total balances of auto loans and leases grew only 2.8% annually in the second quarter of 2024, in contrast to credit card balance growth of 10.8%. (Despite their higher cost, credit cards offer liquidity in a pinch; auto purchases can be deferred.) This is a sector in which higher interest rates are clearly cooling activity.

The loan principal is also a culprit. The mean new vehicle transaction price stands at over $47,000, about $10,000 above the pre-pandemic average. Consumers have reached their limits, as both prices and payments have been in a flat trend for a year.

Auto dealers have also adjusted their behavior. For much of their history, dealers sought to have vehicles on hand to meet any shopper’s need on their first visit. But that inventory is costly, requiring financing and secure parking space. In the pandemic, buyers shifted to more of an e-commerce model: browse and buy online, and take delivery later. Dealers now close sales with less haggling and more profit. Most dealers are now holding half their prior level of inventory.

Lower interest rates ahead may help bring some buyers back into the market. But those shoppers will find the days of cheap loans, ample inventory and aggressive discounting are also history.

Related Articles

Read Past Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.