- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Europe: Struggling To Keep Pace

Cautious investment is holding back the outlook for European nations.

By Carl Tannenbaum

We Americans often think that we are the best at everything. But I can say categorically that is not true. Two weeks of work in Europe reinforced the conclusion that our breads and pastries are no match for the bakery offerings in the Old World. Breakfast is just better over there.

The coffee is pretty good in Europe, too, and it fueled a great series of conversations centered on what’s ahead for the global economy. Following are a handful of key reflections from a very productive fortnight.

“How do you do it?” I was often asked. Thinking the question referred to the sometimes hectic pace of my travel, I highlighted the importance of organization and fitness.

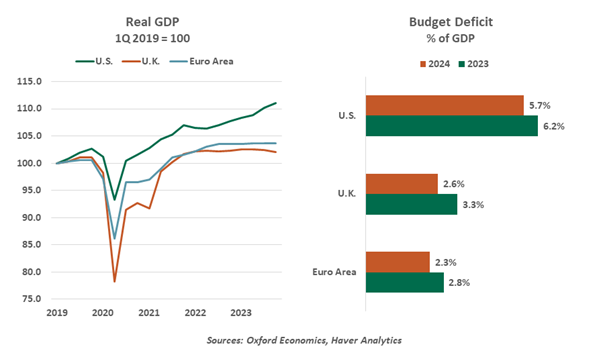

But the curiosity was not about my personal endurance, but rather that of the American economy. The difference in performance on either side of the Atlantic over the past few years has been substantial.

A central reason for this has been fiscal policy: whereas the United States has been spending money with seeming impunity, European countries have been constrained.

Government spending in Europe moderated after COVID-19, but the U.S. kept on going. Congress passed the CHIPS Act, the Infrastructure Bill, and the Inflation Reduction Act (which had more to do with energy transition than the price level). Together, these initiatives will cost more than $2 trillion, spread over several years. The issuance of new Treasury securities has been immense.

By contrast, annual deficits in both the United Kingdom and the euro area are capped by formal guidelines and investor appetite for sovereign debt. With rising interest rates increasing the costs of debt service, room in national budgets for expansive investments has diminished.

Europe could probably use a fiscal boost. Britain’s economy is growing only marginally, and several euro area economies (including Ireland and Germany, which have traditionally been leaders) are contracting. Monetary policy across Europe remains restrictive. But officials in the region have been reluctant to propose stimulus.

An interim budget released by the Chancellor of the Exchequer (equivalent to the U.S. Treasury Secretary) offered little in the way of growth initiatives. In late 2022, an ambitious budget proposal roiled Britain’s government bond market; policymakers fear a similar reaction if too much fiscal expansion is suggested in the run-up to the U.K. election later this year.

Europe is being similarly cautious, having just adopted updated debt and deficit rules last year. The continent is struggling to find space for additional spending on security, energy transition and digital transformation.

The apparent ability of the U.S. to spend without limit is the subject of some envy in Europe.

Clients I met with expressed wonderment over how the U.S. Treasury can continue to issue so much debt without apparent consequence. Europeans also struggle to understand how America can be almost halfway through its fiscal year without a complete budget, and why markets haven’t punished the periodic threats of government shutdowns or technical defaults. I had to admit that I shared their concerns, and pointed them to the article decrying the sad state of U.S. finance we wrote last fall.

For now, the lack of fiscal discipline in the United States is paying economic dividends. But Europe’s experience suggests that those who fail to be sufficiently austere will have austerity thrust upon them. Washington would do well to heed that lesson.

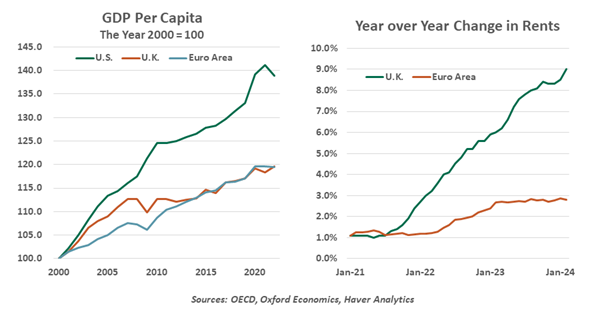

Europe has also lagged the U.S. in productivity growth. Gross domestic product (GDP) per capita has expanded more rapidly in America for more than two decades, and the gap has widened since the pandemic.

Some have posited that America’s headlong rush into artificial intelligence is at play. The top U.S. stocks, known as the “Magnificent Seven,” are dominated by drivers of the new technology. (By contrast, Europe’s top stocks are known as the “GRANOLAs,” a composite of first letters that is dominated by pharma companies producing path-breaking weight loss drugs.)

But the impact of AI is largely ahead of us. Structural factors that foster more innovation have favored the U.S., providing hope for inflation, market performance, and debt sustainability.

Housing shortages are chronic across Europe. Construction has not kept up with the flow of newcomers, keeping substantial upward pressure on rents and property prices. Europe does not include the costs of shelter in its inflation measures to the same degree that the U.S. does; if American conventions were used, European inflation would be worse than is currently stated.

To escape a future of slow growth, Europe will need to invest in itself more aggressively.

At several stops, we met with investors who are focused on emerging markets. The developing world avoided the buildup of inflation seen in larger economies. But many of their central banks nonetheless had to raise interest rates to protect the values of their currencies. Cuts from the Federal Reserve, the Bank of England, and the European Central Bank (ECB) would give smaller countries further room to relax monetary policy and provide relief to their economies.

I was asked repeatedly about the U.S. election. Our European clients follow American politics very closely; I was constantly impressed by their detailed knowledge of the leading candidates. I encouraged them to focus on the policies, and not the personalities. (Admittedly, that was not an easy thing to do.) We discussed the major economic issues that surround the November voting: trade, immigration, and fiscal policy chief among them. While politics are certain to be turbulent over the next eight months, markets often behave more steadily during these intervals.

I am writing this essay while walking on a treadmill, part of an effort to atone for visiting too many boulangers and bäckereien. But if croissants are wrong…I don’t want to be right.

Related Articles

Read Past Articles

Meet Our Team

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)

Carl R. Tannenbaum

Chief Economist

Ryan James Boyle

Chief U.S. Economist

Vaibhav Tandon

Chief International Economist

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.