- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Getting To The Bottom Of “Greedflation”

Policies to address high prices are fraught with complications.

By Carl Tannenbaum

“The point is, ladies and gentleman, that greed, for lack of a better word, is good. Greed is right, greed works. Greed clarifies, cuts through, and captures the essence of the evolutionary spirit. Greed, in all of its forms; greed for life, for money, for love, knowledge has marked the upward surge of mankind.”

-- Michael Douglas as Gordon Gekko, “Wall Street” (1987)

That anthem was characteristic of the era. After two decades of economic frustration, free market policies had prompted a surge of growth and a bull market for stocks. The captains of industry were corporate raiders, who purchased companies, slashed expenses, pushed up prices and reaped outsized rewards.

The 2008 crisis ended the glorification of high finance. The emphasis on self-interest has been muted; firms now think a lot more about corporate social responsibility. Actions that stray too far from the common good are called out for criticism.

Of late, firms have once again been cited for padding their profits at the expense of consumers. Food costs are an issue in U.S. presidential stump speeches, with pledges to act against grocers who have priced too aggressively. These concerns echo similar claims that have been leveled against food stores in Canada, Australia and other markets. But the case study of the food industry illustrates how difficult it is to substantiate claims of opportunistic price increases, or what has become known as “greedflation.”

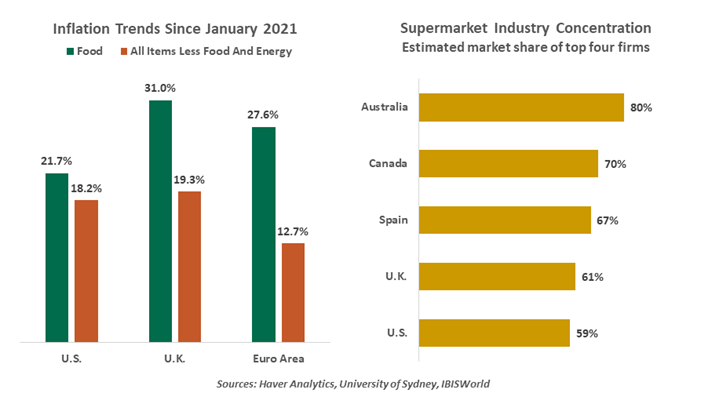

Rising prices have been a central economic issue for the past three years, and food has been a focal point. (Our commentary on this topic can be found here and here.) Food carries a modest weight in the baskets of what consumers spend their money on, but it carries a very large weight when consumers form their impressions of inflation. Groceries are not a discretionary purchase, and we are reminded of their costs during our frequent trips to the store. They are a major reason why perceptions of inflation are much worse than what is being reported.

Food prices have escalated much more significantly than general inflation over the past three years. And the grocery sector is among the more concentrated of industries. This combination of circumstances has created ample grounds for suspicion. It is worth noting that the United States has had a better experience than other markets have, but that is cold comfort for American households.

It is difficult to separate avarice from other factors that affect bottom lines.

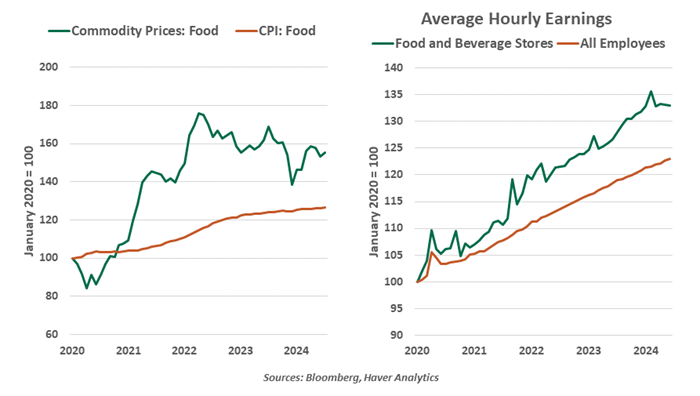

Supermarkets operate on very thin margins. A study by the Federal Reserve Bank of New York, based on data from the U.S. Census, showed that profit margins for food and beverage retailers increased from 2.9% to 4.4% between 2019 and 2023. (For reference, pharmaceutical companies have pre-tax margins of almost 30%.) Food prices increased by 25% over that interval, suggesting that a relatively small portion of that increment fell to the bottom line of grocers.

Operating costs for supermarkets have increased substantially since the pandemic. Consider:

- The costs of goods sold have increased. The Commodity Research Bureau index of food-related commodities has increased by 45% since the beginning of 2021, more than the rise in grocery prices. Beef, eggs, coffee and rice have all been affected by specific supply challenges that have made them much more expensive.

- Wages for grocery store employees have increased by 15% more than overall wages in the United States over the past five years. Average hourly earnings for some food processing workers have also increased substantially. Turnover has always been an issue in both of these sectors, and recruiting was especially difficult during COVID-19.

- Transportation costs have also risen sharply. Diesel fuel (commonly used in trucking) is 56% more expensive than it was three and a half years ago, and there have been periodic shortages of commercial truck drivers. The shift to eating at home during the early phases of the pandemic required an expensive re-routing of supply chains; those were gradually reversed as consumers regained comfort with eating out.

Demand has also played a big role in rising food prices. Pandemic-era support included stimulus checks, enhanced unemployment benefits and additional aid to families with dependent children. Merchants have been able to pass along higher input costs comfortably.

The deep dive into the supermarket sector reveals how hard it is to isolate avarice from all of the other factors that affect bottom lines in various industries. Overall, it does not appear that profit margins have expanded that much in the past few years.

Efforts to control prices and reduce industry concentration often backfire.

Efforts to address greedflation are fraught with complications. Is a government in the best position to determine what an appropriate profit margin is? Prices serve as important signals: they discourage overconsumption and prompt additional supplies. Interrupting the market mechanism could produce unintended consequences.

Industry concentration does, in theory, make it easier for participants to coordinate pricing and boost margins. But it also affords buying power that can limit the costs of inputs and the prices that consumers pay.

Across time and across geographies, efforts to control prices and to break up oligopolies have shown very poor results. Promising an attempt may be politically popular, but following through may actually make households worse off.

If Gordon Gekko were to walk down Wall Street today, he wouldn’t recognize the place. No one is wearing sharp suits, social clubs are closing and he’d have to purchase carbon credits to operate his corporate jet. But while greed is no longer in vogue, incentives remain very important to the functioning of an economy. We tinker with them at our own peril.

Related Articles

Read Past Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.