- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Good Deflation

How much further can goods prices fall?

By Vaibhav Tandon

One of the pleasant surprises of 2023 was how quickly inflation decelerated in major economies. Most of the good news came from falling goods prices.

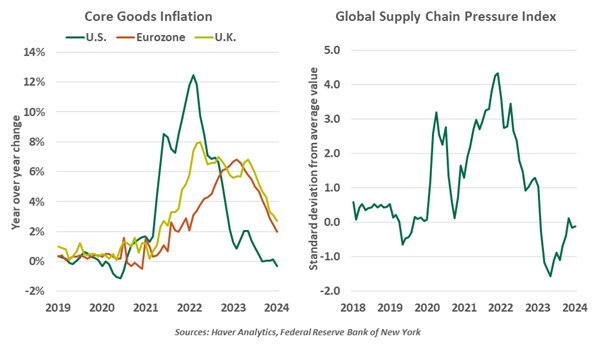

Core goods (which exclude the food and energy categories) account for up to 30% of consumer price indices in Europe and the United States. In the U.S, after peaking at a year over year increase of 12.5% in 2022, prices of core goods are now declining. Falling costs of consumer appliances, home furnishings and cars have led the way.

In the eurozone, non-energy industrial goods inflation has decelerated from a peak of 6.8% year over year in February 2023 to 2.0% in January 2024. Similar disinflationary trends have been observed in the U.K., with core goods prices moderating from a peak of 8% year over year in April 2022 to 2.7% last month.

The pandemic created a series of forces that contributed to a surge in goods prices, with supply chain problems most prominent. Though supply chain pressures heated up a bit recently amid rising shipping disruptions in the Red Sea, supply constraints have generally continued to ease over the past year (see below chart). As we highlighted here, shipping disruptions alone won’t be inflationary.

As economies reopened, consumers shifted back to services, exerting downward pressure on goods prices. Inventories in many sectors are back in line with pre-pandemic levels. Lower pricing power amid weakening demand is forcing firms to accept thinner margins to retain market share.

Though falling, core goods inflation is still elevated by historical standards. In the decade prior to the pandemic, non-energy industrial goods inflation averaged only about 0.5% year over year in the eurozone and the U.K. In the U.S., durable goods prices were in deflationary territory, averaging a drop of 0.8% per year from 1998 to 2020. Globalization was a big influence that kept goods prices low, as manufacturing moved to low-wage countries, cutting costs of production.

Disinflation will have to broaden beyond goods to reach the 2% inflation target.

With commodity prices remaining soft, we think goods disinflation has a little further to go in the near term. Recent producer price developments are pointing toward further cooling of non-energy consumer goods. Developments in China, the world’s factory, also suggest there is some more disinflationary impulse in store. Deflation is becoming more entrenched in the Chinese economy, with manufacturing leading the price cuts.

Weak demand at home and sluggish exports are forcing Chinese businesses to mark down their products. Lower prices of imports will be welcomed by western consumers and central bankers. However, exporting deflation could escalate trade tensions, especially if domestic manufacturers are undercut.

Goods disinflation will ultimately run its course, and is likely to become a modestly inflationary force. With globalization in retreat and supply chains increasingly driven by geopolitical forces over cost considerations, core goods inflation is unlikely to fall to pre-pandemic rates.

Disinflation in durables won’t be enough to bring inflation back to targeted levels. But it is sure doing more than its fair share.

Related Articles

Read Past Articles

Meet Our Team

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)

Carl R. Tannenbaum

Chief Economist

Ryan James Boyle

Chief U.S. Economist

Vaibhav Tandon

Chief International Economist

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.