- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Liberté, Égalité, Austérité

The path toward fiscal balance is treacherous.

By Carl Tannenbaum

Last weekend, the Cathedral of Notre Dame reopened after being severely damaged in a fire five years ago. It took thousands of craftsmen and a reported €840 million to restore the iconic structure. Thanking those who contributed, French President Emmanuel Macron hailed the “fraternity of people who committed to something bigger than themselves.”

It was an uplifting moment amid a troubling interval in Paris. France was one of two major nations whose governments collapsed earlier this month; South Korea was the other. Local circumstances and personalities played major roles in each case. But political polarization and fiscal friction were common denominators, elements that we see in many other world capitals.

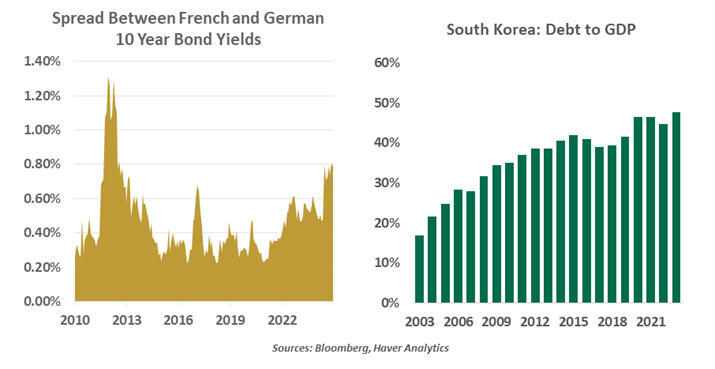

Absent the Summer Olympics, France could easily have experienced a recession this year. Industrial output has fallen off, business investment is down and consumers lack confidence. These factors have limited government revenue and increased the annual budget deficit to 6% of gross domestic product (GDP). France’s overall ratio of debt to GDP stands at 112%; both of these measures are well above limits placed on euro member states.

As a result, France is under an excessive deficit procedure with the European Union (EU). Shortfalls are to be reduced on a certain schedule, with penalties for noncompliance. This requires tax increases and spending cuts, neither of which is popular with the populace.

President Macron gambled this past summer by calling legislative elections early. Instead of gaining support for his centrist agenda, he got an assembly which was strong on both wings and weak in the middle. Even the introduction of former EU official Michel Barnier as Prime Minister failed to initiate compromise. The Assemblée expressed no confidence in Barnier last week, leaving a major void in leadership. A budget for the next fiscal year still needs to be passed.

Markets have been punishing French debt for the lack of fiscal resolve. Spreads between French and German bond yields are at their highest levels in more than ten years; France is actually paying a higher rate of interest to borrow than Greece is at the moment.

Debt can polarize politics and create instability.

Events in South Korea were much more dramatic. Frustrated by a two-year political impasse, President Yook Suk Yeol declared martial law. This brought back unpleasant memories of military rule that ended 35 years ago, and of the Asian financial crisis of 1998.

South Korea’s budget deficit has been increasing in the years since the pandemic. Funding it has required increasing draws on reserves, which are maintained to stabilize currency values when needed. These funds were earmarked to prevent a recurrence of the financial crisis, which initiated a crash in the Korean Won and impaired South Korea’s economy for a long time thereafter.

President Yook has been concerned about the outlook for growth in South Korea, as prospects for exports have diminished. He proposed additional stimulus, which his legislature was reluctant to provide. He decided to take extreme measures to break the deadlock.

As of this writing, Yook remains South Korea’s leader, at least in name only. But the population remains intent on seeing him removed. However the saga ends, South Korea’s international reputation, and its currency, have been dented.

These two case studies are a world apart. But they center on governments which found themselves in fiscal positions that were at risk of becoming unsustainable. The austerity required to address them becomes a political lightening rod; parties maneuver to blame each other for the malaise. They seek to gain an advantage in the next election, rather than compromise in a manner that might be most effective in the long run. In the process, they accept the risk that markets will rebel…which they sometimes do.

This combination of circumstances has been familiar to smaller, emerging markets for some time. But the issues are scaling up. France’s economy is the world’s seventh-largest; South Korea ranks number fourteen. And there may be other large, indebted countries waiting in the wings. If any of them fail, it will cost a lot more than €800 million to restore them.

Related Articles

Read Past Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.