- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Musings On The Money Supply

Money can still be a factor in inflation.

By Ryan Boyle

In 1963, Milton Friedman famously summarized his research thusly: “Inflation is always and everywhere a monetary phenomenon.” Across nations and eras, Friedman found that expansion of the money supply preceded a broad increase in prices. The intuition is simple: more money facilitates more spending, pushing up prices, raising incomes and leading to an inflationary spiral.

Should a sixty-year-old aphorism still inform policy? In recent decades, a number of economies have enjoyed long runs of stable growth and prices amid brisk money growth. A larger money supply is not a problem in itself; it should expand as more people work more jobs and conduct more commerce. Before 2020, we wondered if Friedman’s guidance had outlived its usefulness.

Gradual money growth does not fuel inflation, but sudden surges do.

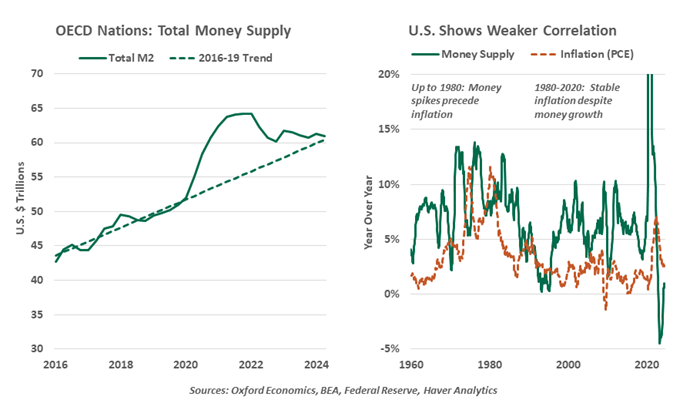

We can now attest that in sufficiently large increments, money growth will still fuel inflation. Large fiscal measures designed to address the pandemic were paid for through rapid debt issuance, which was purchased with money printed by each nation’s central bank. Across advanced economies, the money supply grew by 23% in two years. Students of Friedman warned of what would come next: a bout of inflation that ended a decades-long stretch of price stability.

But all of that is in the past. Inflation has calmed this year, and central banks have started a rate-cutting cycle. Importantly for Friedman’s devotees, the money supply has spent about two years in decline. After the rapid gain and ensuing rundown, monetary aggregates are now tracking toward the levels we would have expected to see if the former growth trends had continued uninterrupted.

This explanation feels too tidy. Money does not cause inflation unless it is deployed into the economy in a manner that adds to demand. Pandemic-era support programs covered a wide swath of the economy. Newly-printed cash that went directly to consumer and business bank accounts enabled spending and contributed to inflation. More mundane programs like the European Central Bank’s Asset Purchase Program helped to stabilize fixed income markets and support lending, but they did bring velocity that would lift prices.

U.S. programs like consumer stimulus payments, the fully refundable child tax credit and Paycheck Protection Program provided immediate liquidity. The nation’s money supply gain was among the fastest in the world, and its inflation rate also grew more rapidly than its peers. Now, the stockpile of excess consumer savings and deferred activity has run its course, and inflation is calming.

The depletion of the money supply has come through quantitative tightening (QT), in which central banks do not reinvest the proceeds when the sovereign debt instruments they hold reach maturity. Both the asset (government bond) and liability (cash previously issued to the Treasury) are written down, shrinking the balance sheet and reducing the money supply. In today’s well-capitalized financial systems, these central bank machinations do not alter activity in the real economy.

Speculation abounds as to the final destination of central bank balance sheets. Daily placements in the Fed’s overnight reverse repurchase facility have fallen to post-pandemic lows, suggesting excess liquidity is drying up; the Fed will not want to cause a panic through a funding shock. Nearly all central banks are taking an approach of strategic ambiguity. The paydown is running in the background of policy, and as long as markets continue to function well, QT is tolerable. As one Bank of England governor noted in a review of QT last year: “We continue to learn as we go.”

Some of the link between money and inflation – especially today’s disinflation – may be coincidental. Friedman’s bromide may be another old rule of economics that has been broken in the modern era.

Related Articles

Read Past Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.