- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Overture on Election Issues

The next U.S. president will face immediate fiscal challenges.

By Ryan Boyle

In terms of occupational hazards, banks are a pretty safe place to work. But when we delve into politics, risks rise. Opinions are strong and tensions are high. Friendly meetings can quickly devolve into pointed questions and heated tones. Starting today and in the weeks ahead, we will live dangerously as we discuss the economic matters surrounding the U.S. election.

The 2024 campaign has already brought a few major surprises and no shortage of discussion fodder. We will leave our readers to turn to the news sources of their choice for the political play-by-play. Our commentary will focus on the economy and policies that may affect it. And from that focused perspective, the race hasn’t been all that exciting; the candidates’ economic policies have not garnered much front-page news.

Fundamentally, less campaign emphasis on the economy is a great omen. When presidential agendas lead with economic plans, that’s a sign the nation in a bad state. Today’s circumstances are generally favorable, though consumer sentiment has been challenged: consumer debt is rising, and major purchases like housing and vehicles feel out of reach. Despite improvement, the rate of inflation remains above target, and today’s prices still don’t feel normal.

But the concerns of 2024 do not compare to the struggle to reopen the economy in 2020 or the free-fall surrounding the 2008 election. The lighter priority on economic policy has given the candidates leeway to evolve their stances; just this past week, Vice President Harris shifted her capital gains tax policy, and Donald Trump floated a deregulation plan.

In election years, we may overstate the president’s power over the economy.

Amid conventions and debates and advertisements and viral videos, it’s easy to think the next president will set the fortunes of every household and business in the coming four years. But the president’s power to control the economy is limited, and interventions are rarely needed. In a typical year, jobs will be created, asset values will increase, prices will rise and the economy will grow. One person will not redirect the nation’s momentum.

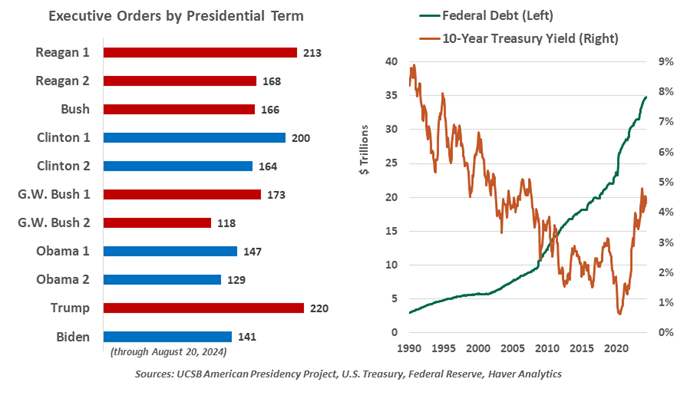

Policy priorities will also be checked by the composition of government. Current polling places low odds on a single party controlling Congress and the White House. A president taking office under divided government will be constrained from day one, and even a sweep is unlikely to yield a 60-vote Senate supermajority. All presidents have used executive orders to make modest shifts in policy, and we foresee no change to that behavior.

In coming weeks, we will dig into policy areas most important to the economy, like trade, industrial development, immigration, taxes, energy and regulation. We’ll focus on the macro view, acknowledging that individual sectors will face specific considerations. We pledge to base our discussion only on the candidates’ platforms, statements and prior records. We assume that the priorities of a second Trump term would be similar to his first, and a Harris presidency would be continuous with the Biden agenda.

We start our coverage today with a discussion of the background, challenges and limitations that either party will face after taking office next January.

Geopolitics are in a tense interval, and the U.S.’ role is uncertain. The Russia-Ukraine and Israel-Hamas conflicts are wearing on, with continual risk of escalation. China faces rising obstacles selling to the U.S. just as its property market undergoes a painful deleveraging. Across advanced economies, populist movements are pushing for insular, protectionist stances, diminishing global.

The national debt is high and rising. No longer a story of pandemic intervention, the Treasury has returned to its old norm of fiscal imbalance, running a structural deficit and tallying an ever-higher mound of debt. But unlike pre-pandemic times, interest rates are unlikely to fall by much; servicing the debt is growing more costly. The U.S. has enjoyed decades of privilege with no apparent market constraints on its ability to borrow. We struggle to predict when we might reach our credit limit, but it is an ever-present risk. And neither party can claim a record of fiscal restraint.

The next president will face a difficult financial outlook.

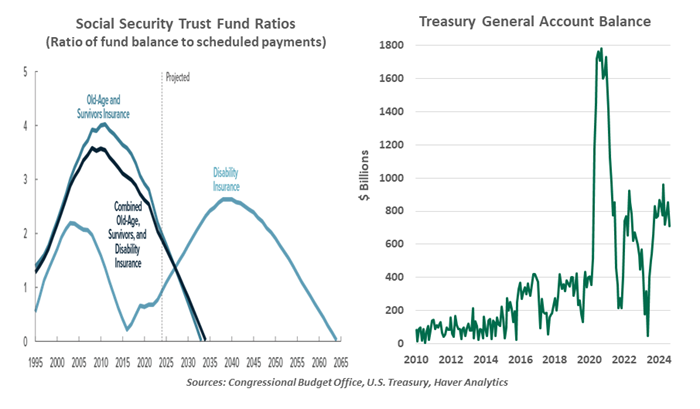

The population is aging. Like most advanced economies, residents of the U.S. are living longer, healthier lives and having fewer babies. Social support for older Americans will further strain the budget. The next president must strike a delicate balance of sustainable immigration, productivity-enhancing investment and measures to maintain vital old-age support programs.

President Trump’s signature fiscal legislation, the Tax Cuts and Jobs Act (TCJA) of 2017, included several features which will expire next year. Absent any intervention, most tax rates will revert to their pre-TCJA levels in 2026. No elected leader will welcome a change that will feel like a tax hike to most voters. Early discussions will focus on the extent to which TCJA is extended.

An important date looms even ahead of the inauguration. The national debt ceiling has been suspended until January 2, 2025. The ceiling will return to force on that date, binding at whatever level of debt is then outstanding. The Treasury General Account is flush (currently over $700 billion). Payment prioritization and quarterly tax payments will keep the nation afloat into the summer, but then the negative consequences will loom large. The combination of scheduled tax increases and the risk of a shutdown and default will make fiscal legislation urgent and complex.

Especially in an election year, it is hard not to apply a political lens to every bit of news. We try our best to stay above the fray. In our upcoming series, we intend to help our readers prepare for any outcome. Our own preparations will include packing a clean shirt in case any tomatoes are thrown in our direction.

Related Articles

Read Past Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.