- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Reflections On The 2024 Election

What's next for the economy after the election?

The people have spoken. While there are still some unknowns, the contours of the American government that will be seated next January are reasonably clear. Here is our early take on how the election results will affect the American economy:

- As of this writing, it appears likely that Republicans will control the White House and both houses of Congress. This outcome will invite a more aggressive policy agenda.

- More expiring provisions of the Tax Cuts and Jobs Act (TCJA) of 2017 are likely to be extended. While there are procedural rules in Congress that limit the impact that fiscal programs can have on budget deficits, we expect annual shortfalls to be higher than previously anticipated.

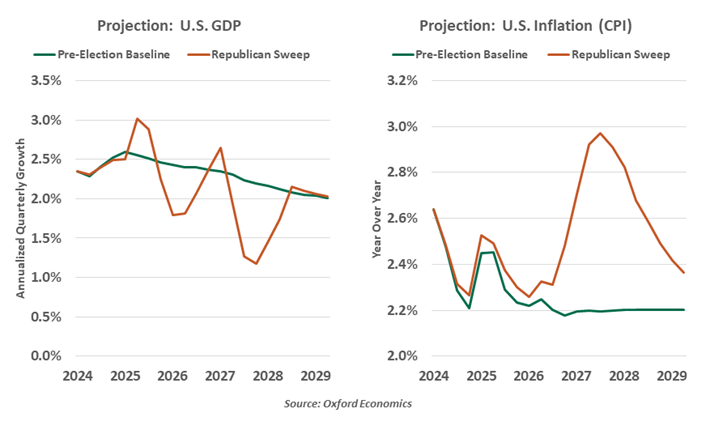

- Tax relief will boost economic growth in the short term, but not in the long term. A lighter regulatory touch for some industries may also support growth, but those effects are more difficult to estimate.

- Increases in tariffs and reductions in immigration are more likely and could be more extensive under unified government. However justified these measures might be, both will add to inflation.

- As a result of all of the above, interest rates are likely to be higher for longer than they would have been under a divided government. Look for friction between the administration and the Federal Reserve to re-emerge.

Following is some background on why the results came in as they did.

When Bill Clinton faced President George H.W. Bush in the 1992 election, Democratic strategist James Carville urged the candidate to focus on pocketbook issues. Carville’s trite summary of the message was “It’s the economy, stupid!” Clinton won, and Carville’s urging became standard campaign protocol.

Economic discontent unseated many incumbents this year.

This year’s American election took place amid very strong economic conditions. Growth has been robust, unemployment is low, inflation and interest rates have fallen, wages are rising and equity markets have been flying. Those elements would tend to favor the incumbent party, but such was not the case this time around.

That is not to say that economic issues didn’t have an important influence on voters—they did. But people’s perceptions of their condition have been darker than the data might suggest. We might propose an amendment to the Carville rule. This year’s theme was: “It’s the vibes, stupid!”

Americans have been discontent about the economy, and it motivated many voting decisions. The rate of inflation has improved tremendously, but the level of prices still feels too high.

Higher immigration offered more reason for worry than hope. The flood of border crossings during the past two years has alleviated some labor shortages, but burdened the ability of the country to process and assimilate.

As we have seen in elections around the world this year, victory went to the candidate representing a change from the status quo. Rightly or wrongly, Kamala Harris was viewed as someone who would continue policies that had become unpopular to many.

Donald Trump will return as president next year, and Republicans have gained control of the Senate. As of the time of writing, control of the House has not been established, but the odds favor a “red sweep.” The margin of victory and the complicity of the Congress will give Trump a wide mandate.

Some measures can be implemented almost immediately after the inauguration. All presidents have used executive orders (EOs) to direct the bureaucracy. Many of the top items in the Republican platform can be implemented through EOs:

- Immigration: Trump will enhance border enforcement and reduce eligibility for the asylum process used heavily in the current immigration wave. Curtailment of new arrivals may be a day one initiative. However, the promise of a deportation operation would be costly and invasive, requiring greater law enforcement resources.

- The risks of losing productive workers and accidentally apprehending legal immigrants may curb enthusiasm for deportation. The legal status of the newest wave of asylees, currently awaiting their adjudication, will be in limbo.

- Trade: Tariffs were the signature policy of the first Trump term, and they remain in force. They were passed through EOs, under existing laws related to national security (metals) and to combat unfair trade practices (China). Most proposed tariffs could be advanced under these or other existing trade policies, often with an interval of months for warning and review. An across-the-board tariff on all imports may not be legal, but the mere threat could compel a new series of trade negotiations.

- Federal land use: When asked about inflation, Trump pledged to make more federal land available for oil extraction. Asked about the short supply of housing, Trump pledged to open federal land to development. Whatever the effect of these policies, restrictions on federal land use are sure to ease.

Other key items will require cooperation from Congress. Before getting to big policy questions, there are some tactical matters requiring attention. The government is currently operating under a spending mandate that ends on December 20; the current legislature will likely extend authorization into January, but something more durable will be needed after that. As well, the debt ceiling returns to force at the start of 2025, and will have to be raised sometime in the new year.

The personal income provisions in the TCJA are set to expire at the end of next year. Trump favors making its provisions permanent, and he has expressed interest in lowering corporate tax rates. The Constitution vests Congress with the power of the purse, and these fiscal measures will require legislation.

Control of the Congress takes outsized importance here. Past showdowns have demonstrated the power of the debt ceiling as a tool for a minority party to force concessions. If Democrats somehow take the House, fiscal negotiations will be intense.

But even under unified Republican control, the party’s more principled fiscal conservatives may balk at unfunded tax cuts and unchecked debt issuance. Further, any fiscal changes will have to be enacted through a reconciliation procedure, which carries some boundaries with it.

Trump’s policies are likely to add to growth. Lower taxes and lighter regulation boosted the economy in Trump’s first term; expanded defense spending will also be accretive. However, the boost will not be permanent. As fiscal support fades and the labor supply dwindles, the risk of an eventual slowdown will rise.

Higher tariffs and fewer workers are an inflationary mix.

The Trump agenda carries inflationary risks. Tariffs are a tax on imports, paid by the importer to the U.S. government. Higher tariffs will be a cost that will cut into margins or be passed along to final prices. The labor market is near full employment and has always relied on immigrants. Halting immigration and potentially deporting workers could bring back labor shortages and ignite wage inflation.

Higher inflation puts upward pressure on rates. The Federal Reserve prefers to remain politically neutral, but it is chartered to maintain stable prices. If fiscal policy proves inflationary, it will affect the path of interest rates. As the election result became more apparent, futures markets made substantial adjustments to the amount of easing expected over the next twelve months.

This will raise the possibility of stress between the White House and the Fed, which was on very public display during the first Trump administration. There are institutional safeguards designed to preserve the Fed’s independence. But over time, new appointments to the Board of Governors will have an important influence over the course of monetary policy. At the press conference following this week’s Fed meeting, Chairman Jerome Powell was grilled about the impact of the election on policy and his own standing; he deflected the inquiries skillfully.

In the near term, the election gives us no reason to change our expectations for the American economy. The soft landing is taking shape. As long as labor markets are stable and disinflation carries on, rate cuts will continue and the U.S. economic outlook remains favorable.

Donald Trump will inherit an economy with little need for intervention, but he will seek to make his mark on it. Changes to policy are coming; changes to “the vibes” are already here.

The Avengers

The law takes a dim view of vigilantes, but they are routinely celebrated in film. Clint Eastwood, Denzel Washington and Keanu Reeves are among the actors who have enjoyed serial box office success playing characters who mete out justice when the system fails to provide it.

Vigilantes don’t just operate on city streets: they can be found in the financial markets, too. Investors sometimes seek to mete out justice when government systems fail to enforce budget discipline. In the wake of the American elections, we may see markets taking matters into their own hands more often.

Concern over the Federal debt is high, but the candidates were mum on how they would address it.

The U.S. national debt has been on a steep upward trajectory. Two crises during this century, two major tax cut efforts, and a series of national investment initiatives have taken the country from surplus into deep deficit. The outlook calls for more of the same, with the country’s aging demographic a driving force.

Concern over rising debt levels is widely held, but it did not register as a major issue during the 2024 election campaign. Both sides proposed policy mixes that promise to exaggerate, not close annual deficits; differences were only in degree. Those hoping for some semblance of restraint were banking on a split government, which would bind the ambitions of the two parties.

As of this writing, control of the U.S. House of Representatives has still not been established. But with the White House and the Senate already in hand, Republicans may have an opportunity to push their agenda through without substantial resistance.

The major issue to be tackled next year is the expiration of preferences established by the Tax Cuts and Jobs Act (TCJA). Under split government, some tax breaks might have been allowed to sunset as a way of preserving revenue and avoiding uncomfortable reductions in Federal spending.

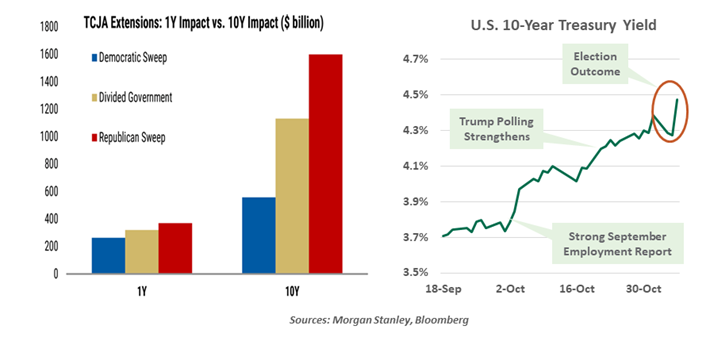

Under unified government, the path to permanence for TCJA provisions widens. Tax cut proponents have often justified their efforts on the basis of supply-side responses that lift growth and broaden the tax base. But the evidence suggests otherwise. Using independent scoring, extending the tax cuts adds to deficits and debt; shortfalls grow more rapidly if the Republican platform is implemented as written.

As prospects for a red sweep began to rise last month, Treasury yields began marching upward. The prospect of ever-increasing bond auctions led yields upward. Long-term U.S. interest rates are almost 80 basis points higher than they were at the beginning of October. This will make carrying the national debt more costly.

By bidding more conservatively for bonds, investors are expressing tacit displeasure at the failure of the Congress to discharge their responsibility for fiscal rectitude. Recent interest rate movements may serve as a warning to legislators not to get too carried away.

Will markets push back against reckless fiscal policy?

The origins of market resistance to fiscal recklessness trace back almost forty years, when the U.S. budget deficit started to grow more steadily. Public officials in that era were fond of saying that “deficits don’t matter,” but the investment community felt otherwise. On several occasions, expansionary fiscal proposals were floated, only to have negative market reaction force a retreat. For instance, in the 1990s, yields across the U.S. Treasury curve rose three percentage points as skeptical investors stepped out, forcing a reduction in fiscal ambitions.

We saw a proximate example of this in the United Kingdom a little over two years ago. Prime Minister Liz Truss proposed a set of steep tax cuts with little apparent offset from spending cuts or other revenue sources. The reaction was swift and severe: the yield on long-term British government bonds jumped by more than 150 basis points over just three days.

Ultimately, the proposals were withdrawn, and Liz Truss earned the distinction as the shortest-serving British Prime Minister in the 223 year history of Parliament. U.S. governments don’t dissolve in the same manner, but the warning should be heeded nonetheless.

Bond vigilantes don’t operate with the drama on display in The Equalizer series. But their impact on an economy can be fierce. If the new Congress fails to do justice to its fiscal responsibility, justice will be enforced from without.

Related Articles

Read Past Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.