- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

The Election And The Fed

An independent central bank supports better economic and market outcomes.

By Carl Tannenbaum

No one from the Federal Reserve is on the ballot next month. But the outcome of the balloting may have implications for America’s central bank.

The four years since the last Presidential election have been extraordinarily eventful for the Fed. In November of 2020, overnight interest rates were close to zero, inflation was just over 1% and unemployment was 6.7%. An aggressive quantitative easing program had increased the Fed’s balance sheet by $3 trillion during the course of that year. Special programs to guarantee corporate debt had been spun up to help firms recover from COVID-19.

By pulling out all the stops, the Fed helped to end the pandemic recession after only two months. But the magnitude of policy support contributed to a surge in inflation that they spent the latter half of the quadrennial trying to tame. Statistically, the Fed has been successful. Nonetheless, lingering impressions of inflation have been cited by voters as a key concern.

With a soft landing close at hand, monetary policy is rebalancing. Interest rates were reduced in September, and are likely to be reduced again at the next Fed meeting in November (which concludes two days after the election). The Fed attracted some criticism for its inattention through the early stages of 2022, but has earned much higher marks in the two years since.

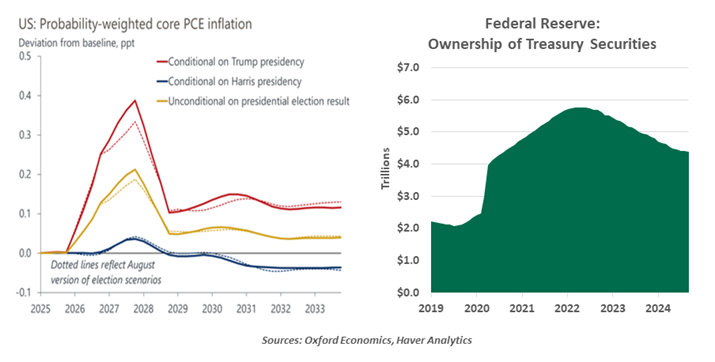

The policies pursued by those elected next month could certainly have an important influence on monetary policy. Heightened tariffs would likely add to inflation, as would the potential deportation of recent immigrants. These factors would take some time to manifest, but the Fed would likely include them in their forecasts at an early stage.

As we wrote last month, neither party is talking much about taming the national debt. The Fed’s balance sheet reductions have made America’s fiscal situation less comfortable; in addition to raising interest rates directly, the Fed’s ownership of government bonds has been rolled back by about $1.5 trillion from its peak. This has forced the Treasury to find other bidders, who are asking for ever-higher levels of compensation to increase their concentrations. Some in Washington would certainly like to see the Fed reduce the pressure on fiscal policy.

Economies with independent central banks perform better.

The Federal Reserve is structured to be independent of the government. Governors of the System are nominated by the president and approved by the U.S. Senate, but they have staggered terms that are designed to head off sudden swings in personnel and philosophy. Further, the regional Federal Reserve Banks hold five votes on the Federal Open Market Committee; their chief executives are approved by local boards, not the Congress.

This architecture has not stopped holders of high office from pressuring the Federal Reserve. The selection of a Fed Chair is the most direct avenue of influence. Current Chair Jerome Powell’s term at the top of the table concludes in May 2026, by which time he will be 73 years old. Observers do not think that he will continue beyond that point.

During his term in office, former President Trump threatened to dismiss Powell on several occasions over his failure to lower interest rates. The legality of such action is certainly not clear. During this year’s campaign, ideas have also been floated that would expose the Fed to more influence from the White House.

The evidence strongly suggests that an independent central bank is associated with better economic and market outcomes. One cautionary tale dates back fifty years: Richard Nixon appointed Arthur Burns, one of his close advisors, to lead the Fed in 1970. The monetary expansion Burns conducted lifted Nixon’s polling numbers but invited the excessive inflation that emerged later in the decade.

Some have characterized the Federal Reserve as an unelected elite. But given the poor track record of our elected officials in managing our national accounts, I’m very happy that I won’t be voting for central bankers next month.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.