- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Trade Policy: More Sticks Than Carrots

Tougher stances on trade are a point of bipartisan agreement.

By Vaibhav Tandon

Rewards and punishments are the alternatives for promoting cooperation. I applied both approaches to train my pet, and discovered that positive methods build a better bond and are more effective at reducing unwanted behavior.

This kind of “carrot or stick” dichotomy also applies to international trade negotiations. Over time, the U.S. has employed both tactics, alternatively leveraging incentives and threats to steer commerce with other nations. For almost a decade, however, sticks have dominated. And regardless of the election outcome, the U.S. is unlikely to be offering carrots to other countries anytime soon.

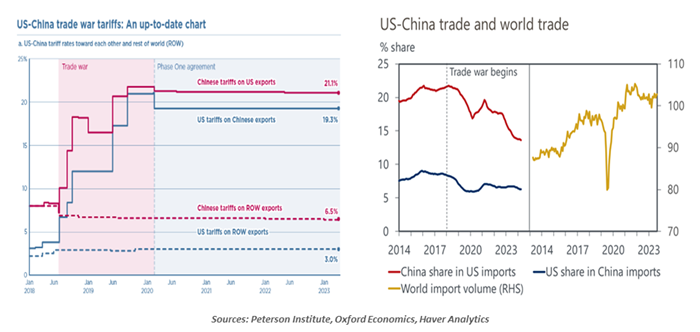

Trade policy is a focal point in the 2024 U.S. election. Tariffs currently in place affect an estimated $350 billion, or about 18% of the total, in imports from China. China’s retaliatory duties cover about $100 billion, or about 11%, of goods arriving from the U.S. The result has been a significant reallocation of trade. China’s share of total imports to the U.S. has fallen 8 percentage points since 2018 to about 14%. Countries like Mexico, Canada, Vietnam and Taiwan have filled the void left by Chinese goods.

China is feeling the pain of tariffs, but the U.S. hasn’t escaped unhurt.

Chinese exporters have managed to circumvent tariffs and trade barriers to an extent by

rerouting goods via countries like Vietnam and Mexico. The growing presence of Mainland companies in Mexico, and the widening U.S.-Mexico trade deficit, have become a fresh flashpoint. The Biden administration recently responded with tariffs on Chinese metals routed through Mexico.

The gap between Democrats and Republicans on issues ranging from immigration to fiscal policy are wider than ever. But their differences are much more narrow on matters related to global trade. Job losses in the manufacturing space, along with shifting geopolitics, are informing both platforms. Both presidential candidates are focused on making U.S. manufacturing and supply chains more resilient, but they differ in their means of getting there.

Vice President Harris seeks to continue the strategy of offering carrots to domestic producers and sticks to foreign providers. She would carry on the current commitment to industrial policy by boosting investment in infrastructure and offering incentives to domestic firms to deepen their supply chains within the U.S. Sticks are also a factor, as Harris would likely maintain tariffs that are currently in force.

On the other side, former President Trump promises to use sticks more extensively by deploying new tariffs and additional protectionist measures to support domestic industries. If reelected, he has vowed to impose levies of 20% on all imports, 60% to 100% on all goods arriving from China and even more punitive rates on firms that offshore their production.

These moves would almost certainly lead to retaliation by other countries and would likely generate pushback domestically. As we discussed earlier this year, the truth about tariffs is that they are borne by households, and increasing them would act like a tax increase. However, the executive branch has broad discretion to implement these penalties.

A Harris administration will look to prioritize the US-Mexico-Canada Agreement’s (USMCA) renewal and leverage the deal to fulfill its industrial policy and supply-chain security objectives. By contrast, the former President has already threatened to hit Mexican-made goods with 100% tariffs, and potentially insist on modifications to the USMCA when it comes up for review in 2026. At a time when trade within North America is poised to expand importantly, the uncertainty surrounding its terms is hindering investment.

China stands to be the biggest loser from an increase in trade barriers. According to Oxford Economics, U.S. levies on dutiable Chinese goods in combination with China's retaliation would bring China's share of American imports down to just 4%. Various studies have pegged losses of up to 2.5 percentage points to China’s gross domestic product (GDP).

That doesn’t mean the United States will come out unscathed. Tariffs are a tax on imports, a cost that either reduces margins or is passed on to final prices. With capital and intermediate goods accounting for more than half of U.S. imports, higher levies would lead to increased prices and disruptions across the value chain. Electronics and computer equipment, apparel, metals and furniture will be among the most impacted sectors.

Escalating trade battles have left no one better off.

Private and governmental studies have concluded that the U.S.’ tariffs have been associated with increased prices, reduced output and lower levels of employment.

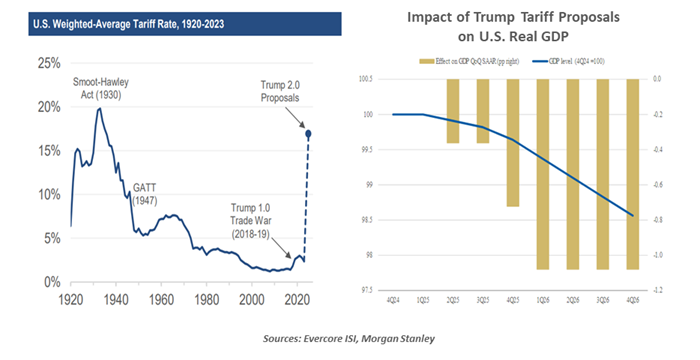

According to Morgan Stanley, a 60% tariff on China and a 10% blanket levy on imports from all other parts of the world would add almost a full percentage point to U.S. inflation, lower consumption and business investment by about 3% each and decelerate real GDP growth in the U.S. by 1.4 percentage points over the next two years. Higher inflation could also complicate the Federal Reserve’s conduct of monetary policy.

The Tax Policy Center estimates that new Trump tariffs will generate considerable gross revenues. But the boost to net federal revenues will be far lower over the next decade, as those levies would reduce other activity and tax receipts. And the cost to households would be substantial.

There was a time when U.S. trade policy was quite simple: America, with a large consumer market and competitive private sector, favored trade liberalization as it provided more market access for the U.S and others. This helped keep prices low and improve ties around the globe.

Today, however, there is concern that trade practices in China and elsewhere have limited access for U.S. companies and placed America at a disadvantage. Negotiations have not produced tangible progress, and so penalties have been assessed.

Sticks alone will not bring countries to heel. Eventually, we need to get some carrots back onto the bargaining table if we want better cooperation.

Related Articles

Read Past Articles

Meet Our Team

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)

Carl R. Tannenbaum

Chief Economist

Ryan James Boyle

Chief U.S. Economist

Vaibhav Tandon

Chief International Economist

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.