- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Treasury Auctions Are Becoming Hard Sales

Demand for Treasuries has its limits.

By Carl Tannenbaum

I will never forget the first auction I witnessed. It took place during one of the many summers that I spent on a farm. The auctioneer talked exceedingly quickly, but those in the crowd seemed to understand everything he said. They indicated interest with a nod or a wink; my host cautioned me not to scratch my nose, for fear that I would end up owning a 900-pound steer.

Auctions of Treasury debt are much different affairs. There is no formal gathering; everything is done electronically. Bids are submitted in advance, and bonds are quietly allocated to those willing to pay the most. But despite the relatively low-key format, Treasury auctions are attracting increasing attention.

Markets are struggling a bit to digest new Treasury debt.

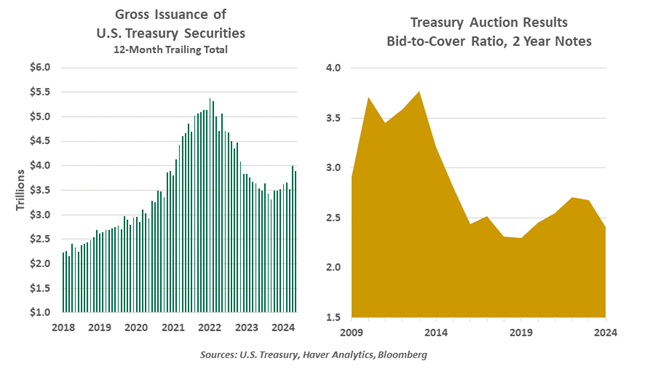

The United States has been adding to its national debt at a rapid rate. We’ve written recently about how this happened, and noted that rising interest costs are creating fiscal and political discomfort. Sustaining order requires securing investors for the tens of billions of dollars in debt which are sold every week.

This effort has gotten more challenging over the past two years, as the Federal Reserve has reduced its holdings of government bonds. Finding replacement buyers hasn’t been too problematic, but there are increasing signs of strain. The implied “term premium” that the Treasury pays to borrow has been increasing, contributing to higher yields.

Recent auctions of debt have occasionally disappointed. The appetite of investors for newly-issued government securities is gauged by several measures. The “bid-to-cover” ratio compares offers to buy with the amount on offer; a lower number indicates weaker demand. This metric has slipped in several recent cases.

In order to ensure that debt auctions are fully subscribed, the U.S. Treasury works with a series of primary dealers. These banks step in to purchase bonds when bids from private investors aren’t sufficient; that support has been drawn on more heavily in recent months.

Given the poor state of the American fiscal situation, auctions will likely remain large for the foreseeable future. The risk that markets will push back is rising. No amount of fast talk from politicians will hide the fact that we may be selling a lot of bull.

Related Articles

Read Past Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.