- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Will 2025's U.S. Stock Market Live Up to the Hype

Why Earnings Growth Matters More than Ever

With earnings season kicking off this week, it is an opportune time to highlight the significance of earnings growth in 2025. Earnings trends are a critical ingredient of stock returns and earnings growth has been very strong in the U.S., driving the S&P 500 Index to fresh highs. Valuation is also a critically important component of stock returns and over the past two years, a key driver of strong returns has been the increase in price-to-earnings multiples, reflecting the higher prices investors are willing to pay for earnings. As a consequence, we begin the year with historically high U.S. stock valuations along with above average earnings growth expectations. This combination of elevated P/E multiples and optimistic growth expectations suggests that this year’s equity returns will likely hinge on earnings more than normal, absent some unanticipated geopolitical impact.

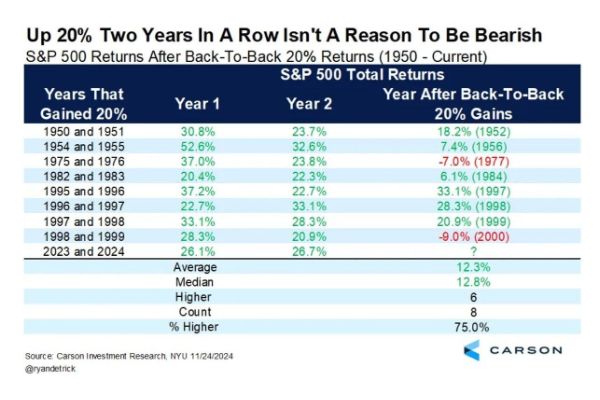

To understand why earnings growth is more critical today, we need to zoom out a little and consider recent market activity for context. The U.S. equity market is coming off two years of very strong performance. For only the 9th time in the past 75 years, returns from the S&P 500 Index exceeded 20% for two consecutive years. While the fear may be that the market is due for some sort of correction after a strong consecutive year, a historical study of market returns suggests that a third year of positive equity returns is entirely possible. As the below graphic demonstrates, a third year of positive S&P 500 Index returns followed consecutive 20%+ returns more often than not.

Graphic 1: Back-to-Back 20% Gainers

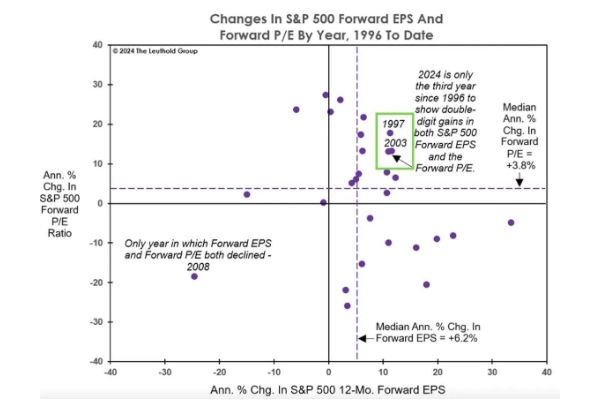

These strong recent returns were achieved through earnings growth, particularly among the Mag 7 stocks that have driven much of the top-heavy returns in the U.S. equity market, as well as increasingly higher valuations that investors are willing to pay to own equities. In 2024, the pace of earnings and valuation growth both exceeded 10%. This confluence of sharply increasing earnings and valuation growth is relatively rare. The only other recent years when this happened were 1997 and 2003. Combined with moderating inflation and continued economic expansion, this “goldilocks” investment environment set 2024 apart and can explain the strong performance of equities in the U.S.

Graphic 2: P/E and EPS By Year

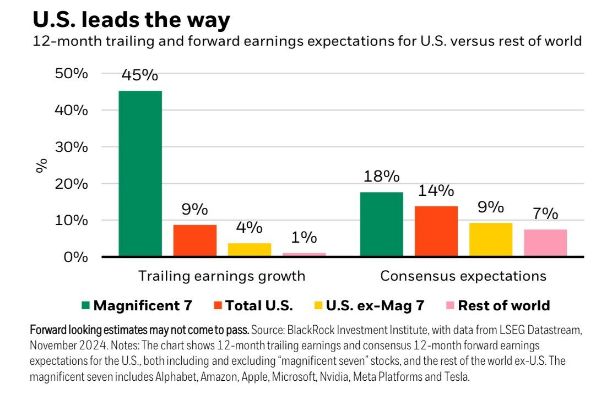

Over the past year, earnings growth has been concentrated among the mega-cap stocks, which have been the primary focus of investors the past 18 months. As illustrated in the graphic below from BlackRock, trailing earnings growth for the Mag 7 stocks is a whopping 45%. While analysts anticipate the Mag 7 names to sustain strong earnings growth into 2025, the pace of growth is anticipated to moderate to 18%. Looking forward, analysts anticipate growth to pick up more broadly, especially among small cap and emerging market stocks.

Graphic 3: Earnings Growth and Forward Expectations

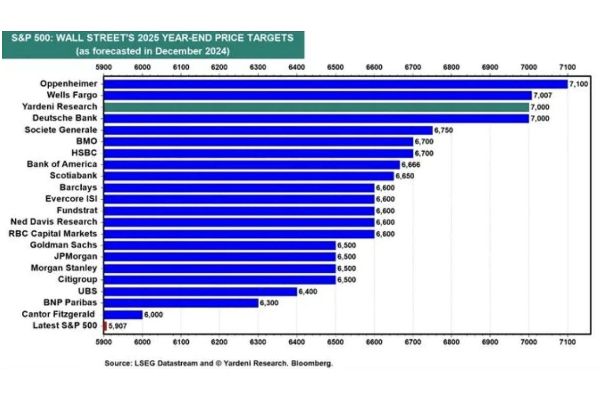

With these forecasted earnings in mind along with receding recession fears among economists, year-end 2025 price targets for the S&P 500 Index are rosy. Nearly every major investment bank and research provider expects 10% or higher returns for U.S. large caps. If we are focused on earnings, these bullish price targets seem logical. After all, 14% forward growth projection for U.S. equities as noted in the above graphic from BlackRock is well above historical trend lines and--absent a decline in valuations--bullish.

Graphic 4: Forecasts for 2025 Stocks

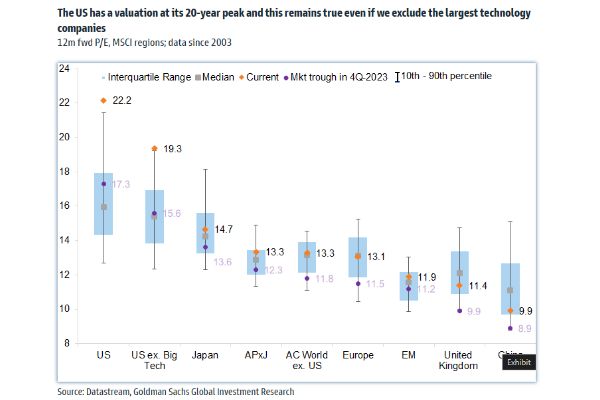

Yet valuation cannot be ignored. When valuations are high on a relative and historical basis, everything must go just right to achieve this year’s end targets. We begin the year in this situation. The U.S. stock market is valued by investors at levels seldom seen. The forward P/E for the U.S. stock market is above its 90th percentile range, as the graphic from Goldman Sachs illustrates. Even stripping out the mega cap technology companies, valuations are historically high in the U.S.. No other equity market in the world is trading at similar earnings multiples.

Graphic 5: Valuations 4Q24

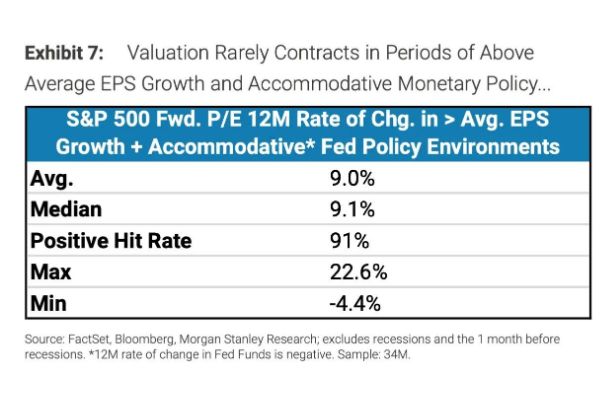

The impact of growing earnings can be easily undermined when valuations fall. If there is a growth scare, real or perceived, investors may not be willing to own U.S. equities at these rich valuations. The solace is that above average earnings growth, especially in a period of accommodative Fed policy, encourages multiples to increase as we have recently witnessed. Periods of strong earnings growth rarely coincide with declining valuations. In fact, in a historical analysis by Morgan Stanley, S&P 500 Index valuation remains the same or rises 91% of the time when earnings growth is above average (6%+) and the FOMC is cutting rates. Thus a logical conclusion is that as long as earnings growth proceeds as well as analysts predict, high valuations will remain intact.

Graphic 6: Earnings Growth Impact on Multiples

The secret to happiness, many have argued, is lowered expectations. High expectations, such as those at the start of 2025 in the U.S. stock market, can be a recipe for a letdown. If valuations were lower, the U.S. stock market would have more of a buffer to absorb disappointment. Yet they are not, and therefore sustained earnings growth will be more essential than ever in 2025.

Therefore risks headed into the year appear to be asymmetrical: a growth surprise to the downside will likely have a more substantive impact on stock prices than a surprise to the upside. Beware of growth scares and the resulting impact on valuations.

Northern Trust Securities, Inc.(NTSI), Member FINRA, SIPC and a subsidiary of Northern Trust Corporation. Products and services offered through NTSI are not FDIC insured, not guaranteed by any bank, and are subject to investment risk including loss of principal amount invested. Additional disclosures are included in the link, see http://www.northerntrust.com/ntsidisclosure

Business Continuity Notice- Northern Trust Securities, Inc.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. This material is directed to professional clients (or equivalent) only and is not intended for retail clients and should not be relied upon by any other persons. This information is provided for informational purposes only and does not constitute marketing material. The contents of this communication should not be construed as a recommendation, solicitation or offer to buy, sell or procure any securities or related financial products or to enter into an investment, service or product agreement in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful. This communication does not constitute investment advice, does not constitute a personal recommendation and has been prepared without regard to the individual financial circumstances, needs or objectives of persons who receive it. Moreover, it neither constitutes an offer to enter into an investment, service or product agreement with the recipient of this document nor the invitation to respond to it by making an offer to enter into an investment, service or product agreement. For Asia-Pacific markets, this communication is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author's employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP, Northern Trust Global Services SE UK Branch and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT, are authorised and regulated by the UK’s Financial Conduct Authority. The Northern Trust Company, London Branch and Northern Trust Global Services SE UK Branch are also authorised and regulated by the UK’s Prudential Regulation Authority. Not all of the products and services mentioned within this material are authorised and regulated by the UK’s Financial Conduct Authority or UK’s Prudential Regulation Authority. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 7th floor, Claude Debussylaan 18 A, 1082 MD Amsterdam; Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE Norway Branch, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651) (NTGL)/Northern Trust Fiduciary Services (Guernsey) Limited (29806) (NTFSGL)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) (NTIFASGL) are licensed by the Guernsey Financial Services Commission. Registered Office: NTGL/NTFSGL -Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. NTIFASGL - Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3QL. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386). Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.