- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Navigating Tariff Complexities

We examine the outcome of President Donald J. Trump’s highly awaited press conference on tariffs and what they might mean for markets.

KEY POINTS

What it is

We examine the April 2 tariff announcement from President Trump, outlining key proposals and the potential implications for trade and market sentiment.

Why it matters

While potential market impact remains uncertain, renewed tariff talk adds complexity to the investment landscape.

Where it's going

As the situation evolves, we’re closely watching for policy clarifications and market responses that could reshape investment planning across equities and international exposures

What happened

After U.S. markets closed yesterday, President Trump held a highly awaited press conference where he outlined his strategy for addressing U.S. trade imbalances. This included the details of a broad-based rollout of additional tariffs on U.S. trading partners.

What was delivered

The President announced a tariff of 10% on all imports from all trading partners (“universal” tariff). Around 60 countries representing the bulk of U.S. imports will receive a tariff that is higher than the 10% universal rate (“reciprocal” tariff). These countries will be charged a custom rate that is half what the U.S. Trade Representative estimates they are charging to the U.S. This appears to have been estimated by the size of each country’s trade imbalance with the U.S., and was said to incorporate non-tariff barriers such as currency practices and value-added taxes. Reciprocal tariffs on some of the largest U.S. trading partners include 20% on the European Union, 34% on China, 24% on Japan, 46% on Vietnam, 25% on South Korea, 32% on Taiwan and 26% on India. The full list of countries charged a reciprocal tariff is posted in Annex 1 of the Executive Order. These tariffs will be stacked onto existing tariffs. For example, without exemptions the total average tariff rate on China could rise to 54% (20% preexisting tariff rate plus the 34% reciprocal). The 10% universal tariff will go into effect on April 5, while the country-specific reciprocal rates take effect on April 9.

A second Executive Order also ends the de minimis exemption for China. This allowed China imports valued under $800 to avoid tariffs. Starting May 2, those goods will be tariffed at 30% of their value, or $25 per item, which increases to $50 per item starting June 1.

There are some key exceptions to the additional tariffs. The pre-existing tariff structure on Mexico and Canada will remain as is. This means that USMCA compliant goods will not be tariffed, which represents around half of imports from Mexico and Canada. That proportion is likely increasing as the countries now have strong incentive to ensure goods adhere to USMCA compliance. The additional tariffs will also not apply to the 25% tariff on steel, aluminum and autos tariffs. It will also exclude many key products including copper, pharmaceuticals, semiconductors, lumber articles, certain critical minerals, energy products and all products listed in Annex 2 of the Executive Order. The scale of imported products that are exempt from increased tariffs will be a key area of focus and research in the coming days. Unfortunately, Annex 3 which includes a more comprehensive list of sector has not been released yet but we should assume that products that are of critical importance to the US economy are likely to be exempt and therefore reduce the effective tariff rate.

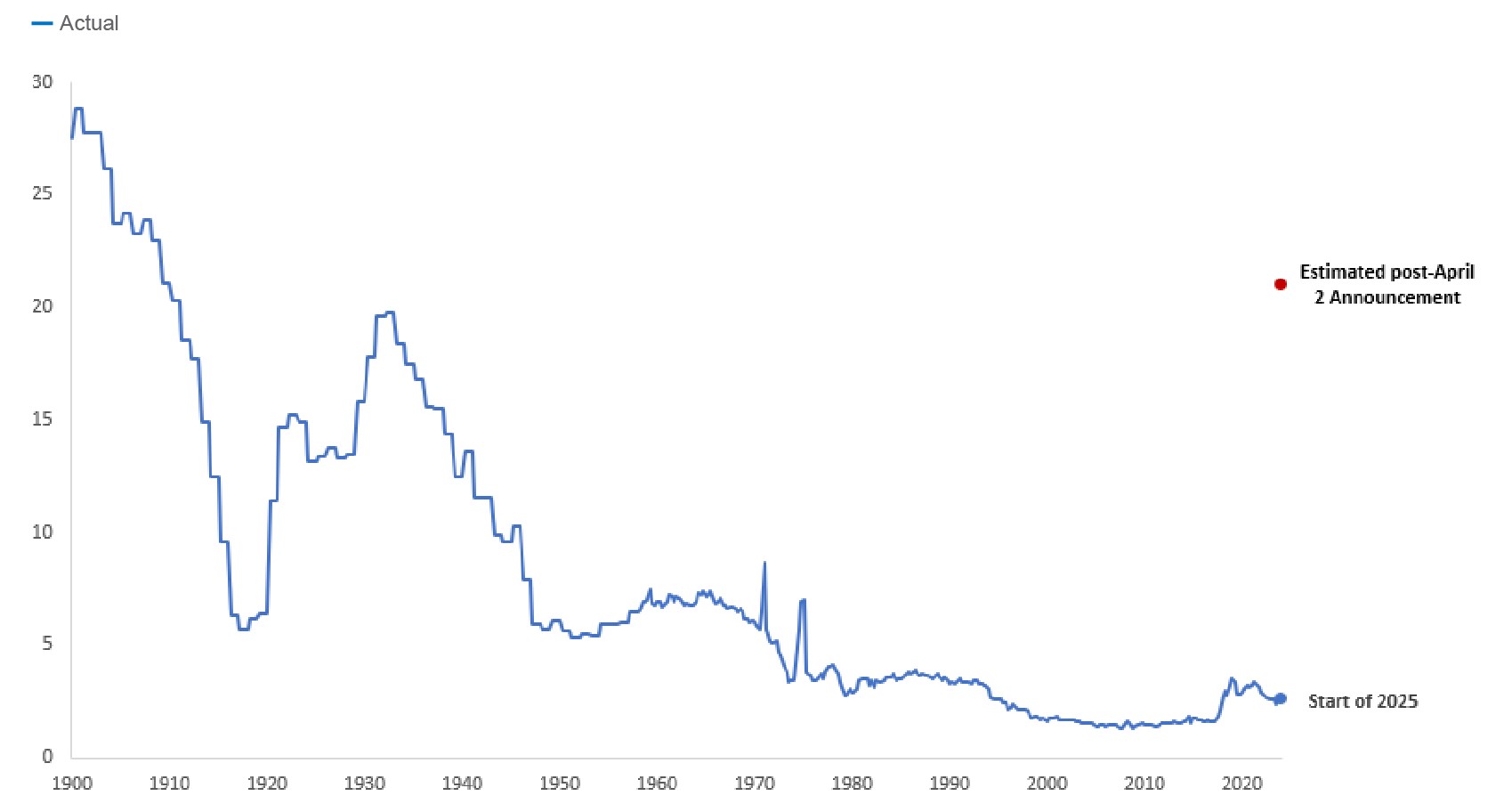

ESTIMATED U.S. WEIGHTED AVERAGE TARIFF RATE ACROSS SCENARIOS (%)

Source: Northern Trust Asset Management, Macrobond, U.S. Bureau of Economic Analysis, Goldman Sachs (GS). GS estimate for post-April 2. Actual tariff rate from 1900 to 2025.

Macro impacts

If upheld, these tariffs could push the U.S. weighted average tariff rate to around 25%, with product exemptions whittling the increase down toward 20%. That would put it at levels last seen around 100 years ago. It also represents a more aggressive approach than we believe consensus expected heading into the press conference.

We expect baseline tariff expectations will move higher, leading to downward revisions to consensus growth forecasts and upward adjustments to inflation projections. And given the unknowns that still remain, we also do not think uncertainty has been significantly reduced.

From a monetary policy perspective, the Federal Reserve’s challenge is to assess the relative impact from higher temporary inflation and the drag on economic growth. If growth fears were to intensify, the Federal Reserve would have ample room to cut interest rates and would prioritize its growth mandate over short-term inflation concerns.

Countries that are most negatively impacted by the hike in US tariffs are also likely to respond with additional fiscal measures. This would be in addition to the already announced boost in fiscal measures in Europe and Asia over the past two months.

Regarding the impact on equity markets, ongoing uncertainty around trade policy is expected to drive further earnings downgrades and exert pressure on valuation multiples. The upcoming earnings season will offer insights into corporate sentiment and specific strategies to mitigate the negative impact from higher import costs.

Net, we believe this increases the odds of our “Supply Restraint” risk scenario in which tariff policy weighs on growth and leads to temporary inflation. This could put downward pressure on equity earnings estimates, with the potential for multiple compression sooner. It also raises the odds of recession cuts from the Federal Reserve.

At the same time, these tariffs may represent the ceiling for tariff rates that could increase the odds of incrementally positive trade news. Information is still highly fluid and the coming days could reveal very important information regarding the outlook. The Investment Policy Committee meets on Wednesday, followed by the Tactical Asset Allocation team’s meeting on Tuesday.

Given the uncertainties, please do not hesitate to reach out with any questions or concerns. We are happy to assist in any way we can.

SMOOTHED Z-SCORE OF DAILY UNCERTAINTY MEASURES

Source: Northern Trust Asset Management, Microbond, Matteo Iacoviello, Economic Policy Uncertainty. One-month smoothed measures of daily data. Data as of 4/2/2025.

CHANGE IN TRADING PARTNER-LEVEL TARIFF RATE BY TARIFF PACKAGE (PP)

Source: Goldman Sachs

IMPORTANT INFORMATION

Northern Trust Asset Management (NTAM) is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited, issued in the European Economic Association (“EEA”) by Northern Trust Fund Managers (Ireland) Limited, issued in Australia by Northern Trust Asset Management (Australia) Limited (ACN 648 476 019) which holds an Australian Financial Services Licence (License Number: 529895) and is regulated by the Australian Securities and Investments Commission (ASIC), and issued in Hong Kong by The Northern Trust Company of Hong Kong Limited which is regulated by the Hong Kong Securities and Futures Commission.

For Asia-Pacific (APAC) and Europe, Middle East and Africa (EMEA) markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. This information may not be edited, altered, revised, paraphrased, or otherwise modified without the prior written permission of NTAM. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. NTAM may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, its accuracy and completeness are not guaranteed, and is subject to change. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on market or other conditions.

All securities investing and trading activities risk the loss of capital. Each portfolio is subject to substantial risks including market risks, strategy risks, advisor risk, and risks with respect to its investment in other structures. There can be no assurance that any portfolio investment objectives will be achieved, or that any investment will achieve profits or avoid incurring substantial losses. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Risk controls and models do not promise any level of performance or guarantee against loss of principal. Any discussion of risk management is intended to describe NTAM’s efforts to monitor and manage risk but does not imply low risk.

Past performance is not a guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by NTAM. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For U.S. NTI prospects or clients, please refer to Part 2a of the Form ADV or consult an NTI representative for additional information on fees.

Hypothetical portfolio information provided does not represent results of an actual investment portfolio but reflects representative historical performance of the strategies, funds or accounts listed herein, which were selected with the benefit of hindsight. Hypothetical performance results do not reflect actual trading. No representation is being made that any portfolio will achieve a performance record similar to that shown. A hypothetical investment does not necessarily take into account the fees, risks, economic or market factors/conditions an investor might experience in actual trading. Hypothetical results may have under- or over-compensation for the impact, if any, of certain market factors such as lack of liquidity, economic or market factors/conditions. The investment returns of other clients may differ materially from the portfolio portrayed. There are numerous other factors related to the markets in general or to the implementation of any specific program that cannot be fully accounted for in the preparation of hypothetical performance results. The information is confidential and may not be duplicated in any form or disseminated without the prior consent of (NTI) or its affiliates.

Forward-looking statements and assumptions are NTAM’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Not FDIC insured | May lose value | No bank guarantee