- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Value-Added Taxes

Differing sales tax regimes can appear unfair.

By Ryan Boyle

International travelers encounter the challenge of planning for electric accessories. Different countries use different voltages, frequencies and connectors. Adaptation is a chore.

Variations in tax regimes can also cause headaches. The U.S. stands out among advanced economies for its lack of a value-added tax (VAT). And when U.S. firms do business with VAT nations, wires get crossed.

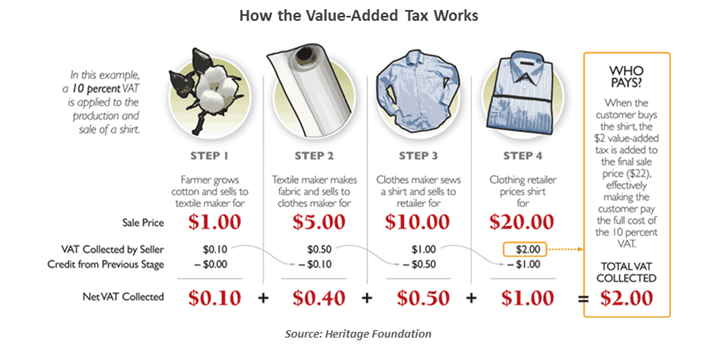

In the U.S., buyers pay a sales tax on final purchases; the wholesale transactions required to build a product and deliver it to the retailer are not taxed. Under a VAT, sales tax is owed at every stage in a value chain. In intermediate steps, the seller collects tax on the sale but deducts the taxes paid previously on the input goods. By netting out prior taxes, the levy is only applied to the gross margin at each link in the chain—that is to say, its value added.

VATs are finding their way into tariff discussions.

VAT incrementally builds sales tax into an item’s price. The final buyer is not eligible to receive a refund, thereby absorbing the full value of the tax. VAT’s proponents tout that it discourages evasion. Parties at each stage of production are motivated to collect the tax, so as to earn the rebate on those taxes when items move to the next point in the process. A disadvantage of the system is that record-keeping adds more transaction costs at each step.

The incremental payment of sales taxes under VAT systems obscures their true costs. VAT rates average 21% in Europe and 15% worldwide. By contrast, final sales taxes in the U.S. are typically below 10%. A VAT-style tax has been floated as a federal revenue measure for the U.S., but has never found widespread support.

When applied to imports, a VAT can appear unfair. VAT is a consumption tax, collected where a good or service is used. When a finished product is imported, the buyer must pay the full VAT. To some observers, the VAT functions much like a tariff in this instance.

The perceived unfairness of VATs has brought them to the White House’s attention, including them in a memo calling for investigation into uneven trade policies. Policies aimed at leveling the playing field could include VATs in the calculation of reciprocal tariffs. Adding VATs in this manner casts a wide net, as over 160 nations have some form of VAT system. Using them as a basis for tariffs would be quite a shock to those countries; adapting would be very difficult.

Related Articles

Read Past Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.