- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Washington Gets To Work On A Budget

Tax and spending cuts will face Congressional roadblocks.

By Ryan Boyle

Donald Trump’s inauguration led this week’s news. Following the ceremony, he marked his first days in office with wide-ranging executive orders and pronouncements focused on immigration, energy, trade and social issues. Trump will act unilaterally where possible, but many of the president’s priorities will require legislation. Among the latter is the establishment of a fiscal plan.

The U.S. Constitution grants Congress the power of the national purse. The imperative of meeting budget deadlines can conflict with the slow, deliberative nature of the legislative branch. To prevent a complete standstill, the Senate has a special procedure called reconciliation to allow budget bills (typically one per fiscal year) to pass with a simple majority. However, reconciliation bills are constrained. They can only contain provisions related to the nation’s finances and must be deficit-neutral over a ten-year span.

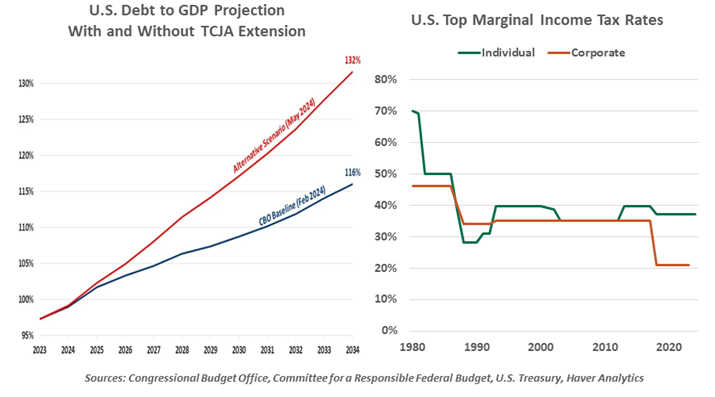

The fiscal effort awaiting our leaders is substantial. At very minimum, the debt limit needs to be raised, and a budget for the current fiscal year must be passed. The work will certainly not stop there. Under the bill used to pass Trump’s first-term tax cuts (the Tax Cuts and Jobs Act, or TCJA), tax rates will increase at the end of the year if not extended by legislation. This is an outcome that both Congress and the White House want to avoid.

Beyond extending the term of the TCJA, campaign promises in need of Congressional support include new tax cuts, expansion of border security, immigration reform, an expanded child tax credit, easier energy permitting processes, more stringent rules on trade with China and an across-the-board tariff. Some of these have tenuous links to fiscal obligations, which may halt their progress. And the longer the list gets, the greater the challenge of achieving deficit neutrality.

The math around projected deficits will be complicated for a bill of any size. Reconciliation must not add to the deficit, relative to a baseline of the nation’s present fiscal outlook. The Congressional Budget Office (CBO) currently forecasts the annual deficit to grow from $1.9 trillion this year to $2.7 trillion in 2035—and that is under current laws, which include the scheduled return to higher tax rates next year. A full extension of TCJA could add $5 trillion of additional deficits over ten years. The need for neutrality may limit the duration of any extension of current tax rates, setting up another fiscal debate before the end of this decade.

Spending cuts are a popular idea, but difficult to enact.

The Trump agenda also includes tariffs. Threats on this front began before the inauguration and have continued this week. Trade investigations are underway, but actual tariff measures have not yet been proposed. New tariffs are likely to be executive actions, as they were in the first Trump term. Since they are not the result of legislative action, any new revenue that tariffs raise will not count as an offset to extending tax cuts.

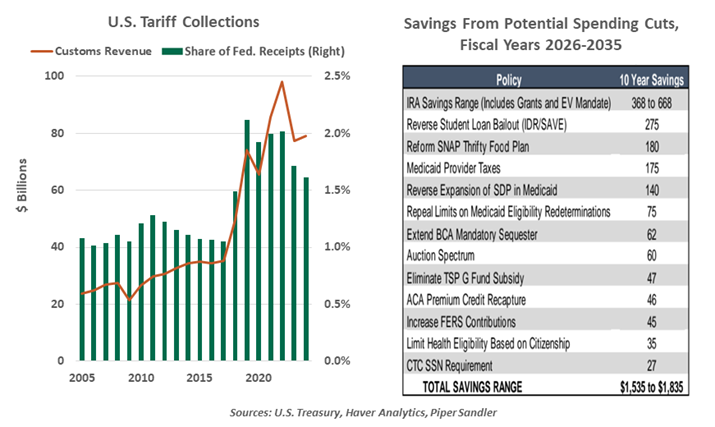

Further, tariffs have not been a major source of income for the U.S. Treasury. A review of customs revenue over time shows the effect of Trump’s trade duties starting in 2018. But at their peak of $98 billion in 2022, revenue from this source amounted to less than 3% of government receipts. Further tariff increases could raise revenue, but it will most likely come out of the pockets of American consumers. This will slow growth and income tax collections. And retaliation by trading counterparts could further depress activity and government revenue.

These myriad issues must be negotiated among a narrow Republican majority in the House, a caucus that is not moving in lockstep on all issues. A vocal faction within the party truly believes in fiscal balance, calling for $2.5 trillion of spending reductions as a requirement for their support.

Cuts are a focus of the new administration, with the Department of Government Efficiency (DOGE) tasked with finding opportunities to save costs and simplify processes. But even before the DOGE has started work, House Republicans are circulating a menu of over 200 fiscal measures with trillions of potential savings. The highest-value proposals include rescinding green energy subsidies and unwinding components of Medicaid. Certainly not all measures will find support, but the length of the list suggests many programs are on the table.

Getting everything together into one fiscal package will be a tall order. This Congress is allowed two reconciliation bills due to a lack of a reconciliation last year, but it is unclear if that helps or only complicates negotiations. Congress would prefer to finish all the work at once and remove the risk of the second bill failing; Trump has expressed openness to either path.

For legislators, one fraught negotiation is preferable to two.

Ultimately, something will need to pass. Big numbers and belligerent goals shared today are opening gambits for months of haggling ahead. Bills are sure to come together, but the negotiations will be long and tense. Some provisions could be broken into less ambitious forms with bipartisan support, though common ground

is limited. No one will get everything they want in a successful negotiation.Trump’s second inauguration was moved indoors on short notice due to dangerously cold temperatures in the nation’s capital on January 20. From here on, we expect the activity and negotiations to generate plenty of heat.

Related Articles

Read Past Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.