- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Trend Lightly

Understanding Bear Markets

The type of bear market matters. If you want to navigate this one, you need to assess which type of bear market we are in.

Bear markets come in three varieties. Each one has a different cause, with peak-to-trough price declines and duration varying among them. Understanding these types of market conditions and historical results provides a framework for contextualizing markets today. Awareness of the three bear market varieties--cyclical, event-driven, and structural--along with your assessment of the current one is critical to determining how to navigate it.

Cyclical

A cyclical bear market is associated with declines in economic activity. We typically experience a cyclical bear market when the economy falls into a recession or growth slows meaningfully. This type of bear market is what most investors conjure up in their minds when they think about a bear market (i.e. resulting from recession, 25% price decline, lasting about one year). However, due to the manipulation of economic cycles by the Federal Reserve and Treasury Department, these types of bear markets are actually the least common in modern times. In the last 100 hundred years, the US equity market has only experienced 4 cyclical bear markets, with the last one being the sell-off in 1990-91. Conversely, in the prior 100 years from the 1830’s to the 1920’s, the US equity market experienced 11 cyclical bear markets.

Event-Driven

This type of bear market is caused by a single catalyst: an event, sometimes political and sometimes economic. These bear markets are extremely visible and explainable at their onset. The sell-off during the Covid pandemic is the best example in recent history. Event-driven bear markets are increasingly common in modern times. Markets are more interconnected and respond to headline news events faster than ever, and single events and the fears emanating from them are reflected with speed. Prices move rapidly in both directions in these situations, and (not surprisingly) event-driven sell-offs typically result in the shortest bear markets.

Structural

A structural bear market is the most profound of the three varieties. These sell-offs follow dislocations in price stemming from bubbles, imbalances, or secular shifts. They are sometimes confused with cyclical bear markets: a cyclical bear is simply a recalibration of market prices given lower than expected earnings stemming from an economic slowdown, whereas a structural bear results from impactful longer-term changes or sentiment shifts far beyond that of a simple slowing in economic growth. This distinction is critical as the selling associated with structural bear markets is much deeper and longer lasting. The most painful and widely discussed bear markets in recent history--resulting from the dot-com bubble and the global financial crisis--were structural in nature.

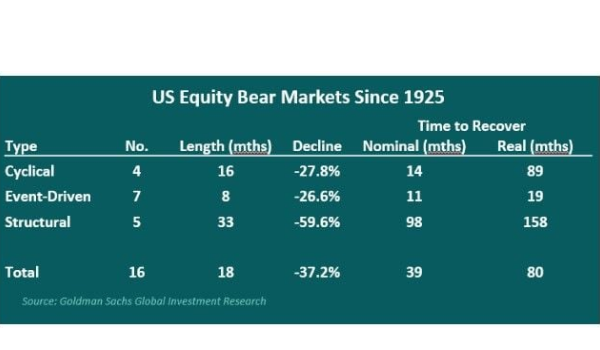

History provides terrific insights as to what to expect from these types of bear markets. Over the past 100 years, the US equity market has experienced 16 different recessions. They can be broken down as follows:

US equity bear markets by type, severity, and duration since 1925

As noted above, cyclical bear markets have only occurred 4 times since the 1920’s versus 11 times in the prior 100 years. The market decline associated with cyclical bear markets is around 28%, with a recover period back to nominal pre-recession highs of just over 1 year. Selling in US equity markets during event-driven bear markets has averaged a similar decline of 27%, but the recovery time to nominal highs is under 1 year. Structural bear markets are the ultimate worry in equity markets. There have been 5 structural bear markets in the US in modern history, and they have seen the biggest price decline (averaging 60%) and longest duration (over three years to previous nominal highs).

Thus far, investors are treating this bear market like an event-driven one, with buying the dips remaining fashionable especially among retail investors. And if this bear market is event-driven, the shortest in nature, then buying dips is sound practice. But could this sell-off really be the beginning of a structural shift, resulting from a new geopolitical structure and shifting economic ties? Could this bear market cut deeper and last longer than many presume?

At this early point in a bear market, one must begin assessing what kind of market we’re currently in. And I believe that the question investors should be asking themselves is if this sell-off is really the beginning of a structural shift.

Meet Your Expert

Grant Johnsey

Grant is responsible for delivering capital market solutions to institutional clients across agency brokerage, transition management, security finance, and foreign exchange.

Northern Trust Securities, Inc.(NTSI), Member FINRA, SIPC and a subsidiary of Northern Trust Corporation. Products and services offered through NTSI are not FDIC insured, not guaranteed by any bank, and are subject to investment risk including loss of principal amount invested. Additional disclosures are included in the link, see http://www.northerntrust.com/ntsidisclosure

Business Continuity Notice- Northern Trust Securities, Inc.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. This material is directed to professional clients (or equivalent) only and is not intended for retail clients and should not be relied upon by any other persons. This information is provided for informational purposes only and does not constitute marketing material. The contents of this communication should not be construed as a recommendation, solicitation or offer to buy, sell or procure any securities or related financial products or to enter into an investment, service or product agreement in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful. This communication does not constitute investment advice, does not constitute a personal recommendation and has been prepared without regard to the individual financial circumstances, needs or objectives of persons who receive it. Moreover, it neither constitutes an offer to enter into an investment, service or product agreement with the recipient of this document nor the invitation to respond to it by making an offer to enter into an investment, service or product agreement. For Asia-Pacific markets, this communication is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author's employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP, Northern Trust Global Services SE UK Branch and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT, are authorised and regulated by the UK’s Financial Conduct Authority. The Northern Trust Company, London Branch and Northern Trust Global Services SE UK Branch are also authorised and regulated by the UK’s Prudential Regulation Authority. Not all of the products and services mentioned within this material are authorised and regulated by the UK’s Financial Conduct Authority or UK’s Prudential Regulation Authority. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 7th floor, Claude Debussylaan 18 A, 1082 MD Amsterdam; Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE Norway Branch, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651) (NTGL)/Northern Trust Fiduciary Services (Guernsey) Limited (29806) (NTFSGL)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) (NTIFASGL) are licensed by the Guernsey Financial Services Commission. Registered Office: NTGL/NTFSGL -Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. NTIFASGL - Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3QL. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386). Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.