The Weekender

Weekly perspectives from Gary Paulin, Head of Global Strategic Solutions, on global market developments and their potential broader implications

September 30, 2023

ANTICIPATE THE ANTICIPATION OF OTHERS

It was John Maynard Keynes who said, “successful investing is anticipating the anticipation of others.” Or, as I like to think of it, “guess what all the guessers are going to guess before they guess it.” It’s the same in sport. Wayne Gretzky would say, “skate to where the puck is going, not where it’s been.” Richie McCaw had a similar quote about a rugby ball. Business imitates sport (Said nobody. Ever.) So where is the puck going from here? What are the market guessers likely to guess next? My picks remain regions like the UK (cheap with cults and catalysts), Japan (see UK) and emerging markets like Mexico and Brazil (re-coupling and material scarcity.) It’s not however, long duration OECD bonds. Why own expensive credit at the end of a credit cycle when you can buy cheap equity (including some with credit-like characteristics) at the beginning of an equity cult, like here in the UK and/or Japan?

Hope

Small aside: I’ve been travelling around Europe recently speaking to fund managers and something struck me. Countries that have lost wars tend to have an investment culture orientated around fixed returns. Neutral countries and those that have won wars tend to have more of an equity culture focused future (rather than fixed) returns. The one glaring exception, of course, is the UK. But it wasn’t always so and my bet is it won’t always be.

Buy before the Brits do

Brits may soon be buying their own share market if Jeremy Hunt’s plan to reform the Individual Savings Accounts (ISA) regime, is adopted. This is exactly what I’ve been pushing for. Tax breaks are powerful incentives, especially when combined with thoughtful marketing and education.

Remember that equities are the best asset class for protecting wealth during periods of inflation volatility. Further, recall that in similar periods to now – such as the 1970’s – UK equities outperformed US ones. And if it’s income you want some UK stocks pay enormous dividends, higher even than what you’ll find in Gilts or in the £1.5T in deposit accounts. The idea that UK stocks have missed the future because they remain tied to “yesterday’s industry” is changing. This is thanks to new narratives (our friend Ed Conway again) that highlight the critical role such industries play in creating the ethereal world of technology, and indeed the greener world of tomorrow. And if the numbers follow the narrative and really does value transfer from the ethereal to the material world assets (think Apple vs FTSE) the re-rating could be substantial. Mean reversion is, after-all, one of the most powerful forces in mathematics. Another is the Observer Effect, where the mere observation of value can affect the actual value. Value that’s been identified by PE (ref 16 current deals) and Ontario Teachers, who recently bought 7IM, a UK Wealth Manager (ahem). And should UK investors, who once held more than 50% of their own market (but now hold closer to 10%) observe these changes then my guess is they will all guess that their market is going up. Now could be the time to buy before they (the Brits) do. The CEO of Ontario Teachers is a Brit….so maybe it’s already begun. Maybe.

…and the Japanese

Japan continues its steady yet remarkably silent march higher. Such trepidation is not the anatomy one typically finds at a top. And with multiple catalysts still to come I would expect this march to continue for a while. In terms of catalysts, look no further than what we discussed re the UK above. Japan too has an Individual Savings Account regime known as the Nippon ISA, or NISA. It was hatched 20 or so years ago under the banner “ Savings to Investments” but given more than 50% of domestic savings are still in deposits, it may not have been that successful. That could soon change. Come next year the government plans to increase tax breaks and double the number and size of NISA accounts. This plan is supported by a concerted marketing campaign championed by none other than the Prime Minister himself, who’s calling it his “asset income doubling plan.” Should he succeed and help flip the fear of loss (which had inhibited adoption) into the fear of something else (namely, missing out) then Japanese stocks should continue to attract the interest of other guessers to guess it’s going up. Don’t wait. Anticipate.

Promoting privates

Dear Jeremy, if you want to promote a start-up culture and prevent our IP form leaving off-shore, I would fade the pension reform measures and focus more effort on public markets. Why? Because the best incentive for private markets is a vibrant, liquid, and expensive public market (see USA for clues.) It not only provides the visible market proxy privates use to value against, but also an exit channel for early investors. It’s why I consider your ISA reforms more favourably than what we’ve seen thus far, from listing, MiFID or pension reforms. Incentives are everything. And Tax incentives to buy assets like those described above could be the very thing you need to revive the cult of equity and the spirit of George Ross Goobey.

Inflation signals

One of my favourite (young) UK investors has a great saying that it’s not sufficient to invest with a margin of safety, but with safety in margins as well. He was the one calling out the logic, inconvenient for some, that if we avoid recession a price response was highly likely in commodities like oil. Elsewhere, since very little capacity has been added, CAPU rates are already high at a time procurement offices flip from destocking to restocking once they’re told to now position for recovery instead of recession. In Washington we have a Treasury that’s happy to run deficits despite near full employment, a situation unlikely to be helped by immigration (at least, not in an election year.) Workers are sensing their opportunity and striking. The number of work days lost to strikes has reached levels not seen in a quarter of a century, 4.1 million days of work. And here’s the rub: the longer inflation stays higher, the more power unions have. And the more power unions have, the longer inflation stays higher. As Arnott suggested, returning to 3% inflation is very hard from +8% and usually takes 10 years on average. We’ve only done one. Still love those bonds?

Tail risk

Expanding on the idea of pre-mortems from Learning without Failing, I’ve spent the last week or so chatting to clients about tail risk. One risk a number of them face is further weakness in bonds and stronger equities, for many tilted their portfolios to prepare for ‘recession’, the dominant narrative earlier this year (more on this below). The even greater risk however, is an oil price spike back to $150 per barrel. According to Karen Ward, Chief Market Strategist at JPM, 4.1% of the 5.9% fall we’ve seen in CPI inflation has been due to energy. A price spike could therefore de-anchor inflation expectations and upset the apple cart (see 2022 for playbook). Of course, there is an easy way to hedge against this risk: buy energy and/or energy stocks. But for some that isn’t possible due to either mandate or morality. Instead, alternatives are being sought in the form of derivatives, with defined risk, duration, and payoffs. While some have the capabilities internally, others are going to external managers despite the lack of alignment. And a few others I met in Amsterdam are using third-party advisers to structure things on their own balance sheet, which solves the alignment issue and keeps costs down. Happy to discuss more, if interested.

Oil

If Putin was ever thinking of weaponizing energy, it probably makes sense to do so in winter – a period of peak (and essential) demand. To this end, did you notice he recently banned exports of petrol and diesel, ostensibly to stabilise the domestic market? What if this is the start of something more strategic? It seems China got the memo however, for their strategic reserves hit a record in July. In contrast, Biden’s withdrawn more than half of his reserves. Do they know something we don’t? Who knows, but clearly there is a risk to an oil spike. One worth hedging against.

If you have to fail, fail fast

According to Georg Tacke in Monetizing Innovation nearly three quarters of new products fail to hit their revenue goals, some sinking the ship entirely because they were developed in a vacuum, they were pushed by personality (thus lacking internal consensus,) or they failed to put the client’s willingness to pay at the core of product design. Often, the original proponent leaves by the time the idea has been jettisoned, leaving others holding the bag. Now, while success is the goal of any strategy, the next best outcome is failing fast. Failing slow, conversely, should be avoided at all costs. It consumes resources, destroys capital, creates opportunity cost, brings about decision fatigue, and it can erode trust in leadership. And what’s true in business is also true of government. Take Rishi Sunak’s decision to scrap part of the UK high speed rail plan. He’s saying he would rather stop things here than risk further project delays and cost-overruns. He would rather fail fast than let this run, sucking up more resource, and then leaving the issue for someone else to solve. He’s taking responsibility. Politics aside, that’s what leaders do.

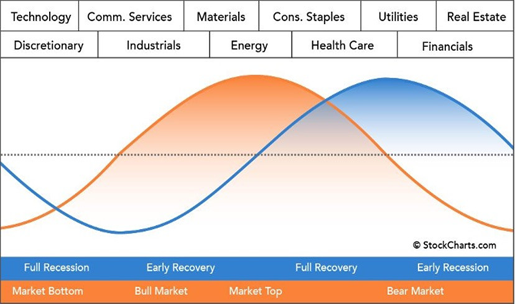

The risk of higher equities. What?

As mentioned, another area of concern for many allocators is they find themselves underweight equities. This is in part because so many had tactically positioned themselves for recession as they entered 2023. As markets have rallied (in a fairly typical fashion) that underweighting becomes increasingly uncomfortable. Should asset owners seek to rebalance and chase performance the market may remain well bid for a while longer. When looking at the market structure, we’ve seen a fairly classic recovery lead by technology, consumer discretionary, communication services, and industrial sectors. Then over the summer leadership shifted towards energy, materials, and healthcare. It is only when consumer staples and utilities start to outperform that we need to worry. See below from StockCharts.com.

ACHIEVING GREATER TOGETHER

Northern Trust Charity Trading Day

OCTOBER 12, 2023

Every year Northern Trust holds its global month of service, Achieving Greater Together (AGT), to engage our global staff in a unified effort to support the communities where we live and work. As part of AGT I’m excited that Northern Trust will be holding its second Charity Trading Day on October 12. This year Northern Trust is targeting to contribute up to US$1M based upon the day’s trading revenues in our Capital Markets business to four global charities: Global Red Cross and Red Crescent Network, Ronald McDonald House Charities, War Child, and World Central Kitchen. Click the link below to learn more about Northern Trust Asset Servicing’s support for the company’s long-term community investment strategy.

Never settle

Love this quote from Mia Hamm, “Take your victories, whatever they may be, cherish them, use them, but don’t settle for them.”

That said, if you gave me four more All Blacks victories, I probably would settle for that. Well, for four years at least.

Receive The Weekender

Register your interest in receiving Gary's commentary direct to your inbox.

Gary Paulin

Head of International Enterprise Client Solutions

NEITHER THE INFORMATION NOR ANY VIEWS EXPRESSED CONSTITUTES INVESTMENT ADVICE AND IT DOES NOT TAKE INTO ACCOUNT THE SPECIFIC INVESTMENT OBJECTIVES, FINANCIAL SITUATION AND THE PARTICULAR NEEDS OF ANY SPECIFIC PERSON WHO MAY VIEW THIS MATERIAL.

These are my own personal views, not those of my employer. This report is not intended for retail customers. Any further disclosure, use, distribution, dissemination or copying of this report or any of the information herein is strictly prohibited. The information in this report has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Any opinions expressed herein are subject to change at any time without notice. Any person relying upon information in this report shall be solely responsible for the consequences of such reliance. This report is provided for informational purposes only and does not constitute legal, tax or other advice nor does it constitute an offer or solicitation to purchase or sell any security, commodity, currency or other product. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining advice from their own advisors. Internet communications are susceptible to alteration and Northern Trust shall not be liable for the message if it has been altered, changed or falsified.

Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.