The Weekender

Weekly perspectives from Gary Paulin, Head of Global Strategic Solutions, on global market developments and their potential broader implications

September 2, 2023

THE VOLATILITY ILLUSION

The coastline paradox

Did you know New Zealand’s coastline can be measured as longer than the entire coastline of the United States? That is, if the yardstick used is a metre. In fact there is no official way to measure a country’s coastline as the length varies depending on the measuring stick: a kilometre gives a much shorter distance to a metre, a paradox from the field of mathematics called fractal geometry. Now, this same paradox, arguably, exists with investing. The less often you measure an asset, the lower the perceived volatility. Measure your house from the day you buy it to when you sell it, and you’ll think the relationship is linear. The measurement is heavily dependent on the yardstick, whether it’s one decade, one year, one quarter, or one day. If you measure something daily, it may create the illusion of being highly volatile despite there being no fundamental change in business prospect from one day to the next. Why does this matter? Well, things sold as being less volatile can attract more investors. More leverage. And more risk.

The volatility illusion

Most asset classes have a lifecycle. As more money enters, the high returns once offered can erode over time. Sometimes leverage is applied to maintain growth, adding risk for when the downturn, inevitably, occurs. Some argue that’s the case for private equity investing today, but that seems a gross oversimplification. And PE certainly plays a role for asset allocators by providing access to areas that are hard to gain exposure to in public markets, like elite women’s sports (as discussed last week). It pays to be mindful, however, especially at the end of a credit cycle where liquidity can dry up, and with many LPs nearing buy-out or decumulation phases, that funds have sufficient cash-reserves to fulfil any obligation without selling the crown jewels, often at a discount. There’s only one winner in that scenario – the acquiror. (See First Citizens + 80%, UBS +38% and Apollo +33% for clues). There is one point worth highlighting however, and it’s not to criticise the process of PE. Rather it’s to illuminate the benefits of public investing. The idea that privates are less volatile than publics is somewhat illusory. It’s dependent in part on the measure. The yardstick used.

Changing the measure changes the mean

Now, there are a number of perceived benefits of investing in private assets. Having no visible market proxy to cause panic, fear or greed, is one. It enables one to arbitrage time. Be patient and even, at times, benefit from the impatience of others: the closest thing to a free lunch in markets. This perceived stability gives comfort to a lender, who accepts the asset as collateral. You can apply leverage to it, increasing potential returns – assuming you can sell the asset for more than you paid for it, minus the debt. But as time goes on and popularity grows, what happens to this asset class when other investors, perhaps those with less patience, ‘want in’. And what happens when they ‘want out’? Well, we might soon find out. The pressure for PE funds to become more democratic, transparent and liquid has reached the point where regulators across the globe, from the SEC to APRA in Australia, are calling for more frequent valuations – at least quarterly – and in the case of the Aussie Supers where daily dealing is a thing, an appropriate market proxy for all other times. In other words, changing the measure. The yardstick. And if changing the measure changes the perceived volatility and associated debt loading, might it also change the mean? It could pay to watch this carefully: pressure to increase the frequency of measurement could alter traditional ideas of ‘stability’. Less stability could mean less leverage. And less leverage could mean lower returns. There could be unintended consequences that potentially hinder one asset class at the expense of another. Public markets.

Private to Public

Of course, more frequent measurement may not be a bad thing. Valuations can increase. And I’m not sure this is the “ end of an era” as Marc Rowan, chief executive of Apollo Global Management, warned recently. But it might be the beginning of a new area for another asset class, like the one currently being targeted by PE. UK (and Japanese) stocks! According to Bloomberg there have been 16 deals either done or underway this year in the UK, while there has been only one IPO of note. Why? Because it’s ludicrously undervalued making it attractive to buy-outs, but not for new issues. Consider that pay-out ratios at <50% are below average, meaning dividends look sustainable (the FTSE dividend pays as much as 10yr gilts with more inflation protection), and the market is 50% cheaper than the US on a cyclically-adjusted basis. As most of the larger PE firms are US-based, this represents an extraordinary arbitrage opportunity. Even more absurd (or opportunistic) is the idea private equity is on course to invest more money in the asset management industry this year than ever before, according to Ignites Europe. Now, we are talking Europe here, not just the UK, but the point holds: if we don’t buy UK stocks, others, notably in private equity will! Now, you could simply wait and watch PE gorge themselves on the under-valued fruits of our inaction. You may even be enticed by price, and ‘want-in’ paying 2 and 20 for the privilege. Or, you could buy those same stocks and managers today, at a discount to intrinsic value and clip a healthy dividend while you wait.

Only a mother could love?

OK, so being a long-term bull on UK stocks is tough gig. A market only a mother could love? The FTSE’s flatlined all year and if I’m honest, I was underwhelmed by Jeremy Hunt and his Mansion House reforms. Still too few incentives, tax or otherwise, to create a home bias. The best hope of luring growth equity is by an attractive exit multiple, but there’s an absence of focus on public markets, a continually negative drum-beat from the press and former investors, and little to re-inspire the spirit of George Ross Goobey and the ‘ cult of equity’. If anything it’s the opposite, we are de-equitizing (see above). I’ve not seen anything likely to dissuade companies wanting to list in the UK, which according to the Wall Street Journal, requires “expensive marketing and advertising packages worth $50 million" (what Nasdaq paid to entice Arm Holdings). So while easier listing rules, reforming MIFID and increasing analyst coverage (assuming that’s an outcome) might help, it’s probably not enough. But I’m still bullish. (See last week’s missive re: stupidity).

Mean reversion

So why am I still bullish? In a word (well, two): mean reversion, driven by, as mentioned in previous editions of The Weekender, science ( Shue and Hartzmark), storytelling (Conway’s Material World) and incentives (The US Inflation Reduction Act, or IRA). I’ve been surprised how many asset owners have started to push back on the logic of exclusion vs engagement, that brown = bad and green = good, with some now prepared to engage even in those hard-to-abate areas, like oil, keeping exclusion as an ultimate punishment. Their argument: “a zero-carbon portfolio is not a zero-carbon world”. Doing good and looking good are different things. It’s early, of course, but more active engagement in such businesses, the likes of which the UK is full of (on half the value of the US), could drive capital into, not away from these areas, impacting price. This at a time demand fundamentals for things like oil, are going up, not down (see below). More is starting to be made of the fact the scarcity, and therefore value, within Technology is sometimes more acute in material world assets. Yes, you want to own the picks and shovels in a gold rush (i.e. Nvidia) but without the materials to make them, no picks, no shovels. Similarly, there is a reluctant, often painful acceptance emerging that to move forward towards a greener world, we can’t move at all without these materials. And while we don’t have our own IRA, we have the next best thing: we’re deemed a “ domestic source”. And this is where things get interesting, for if my reading of the Atlantic Declaration is correct (i.e. the document that which embodies this special status) to be deemed such, the UK needs to have a free-trade agreement in place. As I have mused before: has Sunak made progress on a US trade deal? Considering UK elections will take place next year, it would be a welcome boost for the government if he has.

The Inflation Reduction Act turns one year old

The IRA celebrated its first birthday on August 16 2022. It’s illustrative of muscular industrial policy and along with a number of other enactments is symptomatic of a more national, less international world we now live in (that is unless you are a special friend). Since being passed, manufacturing construction has surged in the US. CRH told CNBC they expect the US to spend $1.2T on roads over next few years, a 50% increase, calling it “ the golden age of infrastructure". United Rentals is up 80% in a year. Its closest competitor, Ashtead, has talked about unprecedented demand from $2T in fiscal stimulus. Irish building supplier, Kingspan is up 50% YTD having cited an end to destocking and strong ‘ industrial and tech markets’. And US Steel’s CEO is calling it the Manufacturing Renaissance Act, believing we’re on the cusp of a ’once-in-a-generational steel cycle’: “The place we’ve called home for 120-plus years was finally recognising that a strong manufacturing base was vital to its security in a de-globalising age”. For clues what the US can do in the name of national security, consider that during WW2, a single Chrysler factory in Detroit produced more tanks than they entire Third Reich! So, we have old money military Keynesianism, large fiscal deficits at a time of full employment. And yet, you all love 10Y bonds at 4% and loath the FTSE with an earnings yield more than double that. Something doesn’t quite add up there. Even for me.

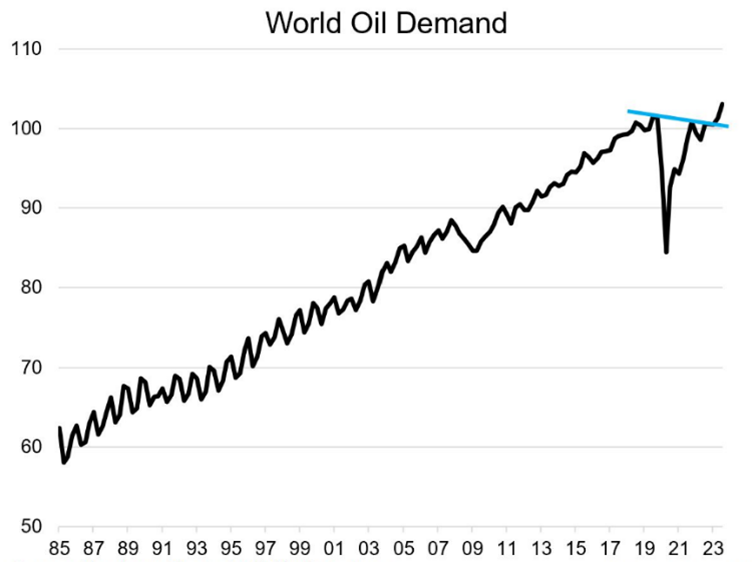

World oil demand breaks out

Given we are talking about the FTSE where oil is its largest weighting, I thought this chart below, from Topdown Charts, was relevant. It shows world oil demand (across all products) is set to return to pre-covid levels, with a breakout to new all-time highs. This despite a stuttering Chinese economy, is evidence, perhaps, that to transition to a greener future, we can’t get there without a lot more salt, sand, silver (great chart), iron, copper. And oil. Take electricity production, where many forecasters agree that electricity demand could increase by 50% by the end of the decade. Even if fossil fuels fall to 50% of total production by then (from about 70% currently) that’s still more than a doubling in oil demand, at a time supply is being constrained. And this only occurs, of course, if we see renewables capacity increase by 150%, which is not without risks. Just this week, Orsted fell -22% on large off-shore wind project delays, and along with other developers are looking to increase contract prices to offset rising costs (= greenflation). As I’ve said prior, I have no dog in this race save the climate (and my pension). But there is little in any of this to give me confidence we can transition to a cleaner future – which we must – without the cost of higher inflation.

Source: Topdown Charts, Refinitiv, Datastream

Greenflation

Finally, while talking about transition costs to a greener world (i.e. greenflation), it will be interesting to see the push-back, if any, on the EU’s proposed Carbon Border Adjustment Mechanism (CBAM) which will be phased in from October. This, ostensibly, is to avoid carbon leakage to countries that don’t impose carbon taxes. Although its aim is to level the playing field between domestic production and imports, some EU producers will see their costs rise immediately and others will see input costs rise. This, just as the world grows more comfortable about the idea that we can get back to target 2% inflation. And stay there.

Thanks for reading.

Gary

P.S. The Weekender may not appear as frequently over the next few weeks as I will be travelling with limited time to write. Including to France for the important matter of the Rugby World Cup.

Receive The Weekender

Register your interest in receiving Gary's commentary direct to your inbox.

Gary Paulin

Head of International Enterprise Client Solutions

NEITHER THE INFORMATION NOR ANY VIEWS EXPRESSED CONSTITUTES INVESTMENT ADVICE AND IT DOES NOT TAKE INTO ACCOUNT THE SPECIFIC INVESTMENT OBJECTIVES, FINANCIAL SITUATION AND THE PARTICULAR NEEDS OF ANY SPECIFIC PERSON WHO MAY VIEW THIS MATERIAL.

These are my own personal views, not those of my employer. This report is not intended for retail customers. Any further disclosure, use, distribution, dissemination or copying of this report or any of the information herein is strictly prohibited. The information in this report has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Any opinions expressed herein are subject to change at any time without notice. Any person relying upon information in this report shall be solely responsible for the consequences of such reliance. This report is provided for informational purposes only and does not constitute legal, tax or other advice nor does it constitute an offer or solicitation to purchase or sell any security, commodity, currency or other product. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining advice from their own advisors. Internet communications are susceptible to alteration and Northern Trust shall not be liable for the message if it has been altered, changed or falsified.

Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.