- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Global Economic Research

Global Economic Outlook: Somber Summer

The Northern Trust Economics team shares its outlook for key markets in the month ahead.

The global economy is slowing. Elevated energy and food costs, declining real incomes and China’s rolling COVID lockdowns are all taking a toll on activity. Confidence surveys and leading indicators like the purchasing managers indices (PMI) are moderating. Markets are on edge as stubbornly high inflation is forcing central banks to tighten aggressively, despite signs of slowing growth.

One silver lining so far: There are no clear signs of a wage-price spiral in major economies. We are hopeful that inflationary pressures will wane, but the descent will be gradual owing to lasting disruptions in commodity markets.

Against this gloomy backdrop, we have downgraded our growth expectations for western advanced economies. Our outlook does not feature a recession in major markets, but the likelihood of that outcome has risen.

This month’s edition offers a deep dive into the eurozone economy, which faces the biggest risk of stagflation.

Eurozone

- The eurozone is facing a host of challenges that are jolting its economic prospects for this year and next. Be it the Ukraine war, elevated inflation or rolling lockdowns in China, all are weighing on consumer and business sentiment. Given the economic backdrop, we have downgraded our growth expectations for the region. The risks of recession are rising, but we expect growth to persevere; the most salient risk to the outlook is a complete cutoff of Russia’s natural gas supplies to the bloc.

- Inflation continues to rise in the eurozone, reaching a multi-decade high of 8.1% for the twelve months ending in May. Energy prices remain the main driver of higher headline readings, although they have eased slightly due to recent government interventions. Food prices are on the rise, however, which has offset the deceleration of energy costs. Underlying price pressures are also widening across subcomponents, as firms are passing on higher input costs to consumers.

- Stubbornly high inflation has shocked many central banks. At its June meeting, the European Central Bank (ECB) left policy rates unchanged, but previewed 25 basis point hikes in July and September. ECB President Lagarde suggested that the door is open to an increase of 50 basis points at one of those meetings if conditions warrant. The bank also announced the end of its long-running Asset Purchase Program.

- The spread between Italian and German government bonds has widened recently, forcing the ECB to explore a backstop to cap surging borrowing costs in the peripheral economies. This shows the challenge the bank faces in trying to reconcile its inflation mandate with financial stability, and preventing market pressures that could threaten unity within the euro currency area.

- Labor markets are tight in the eurozone. The unemployment rate is at its lowest level since the bloc’s inception, with labor shortages reported in several sectors and member states. While this is contributing to the demand for higher pay, wage pressure has remained muted and well below what is being experienced in the U.S. and the U.K. Union wage settlements, which set benchmarks for the private sector, are resulting in modest increases of only 2.5% to 3%.

The drag on activity from the Ukraine war and the looming slowdown may be taking the edge off wage demands. During uncertain times, workers may prefer to safeguard jobs over seeking higher compensation.

- The incoming data confirms the deteriorating economic conditions across the common currency region. The June PMIs surprised significantly to the downside, dropping to their lowest levels since February 2021. Declines were broad-based across states and industries. Leading indicators such as manufacturing orders and business expectations also fell sharply, pointing to a further slowdown ahead.

- European manufacturers have already been contending with supply-side complications stemming from China’s rolling lockdowns and higher input costs. Shipping from Eastern Europe has been complicated by the war. Gas flows from Moscow to Germany, the region’s growth engine, fell significantly in June, leading to a surge in European gas prices and raising the possibility of rationing.

- Worryingly, Europe’s service economy, which had been underpinning growth, is also starting to lose steam. Most reopening tailwinds have now run their course, which was a key factor behind the service sector’s strong performance. The cost of traveling has skyrocketed, diminishing tourism.

- Government subsidies for energy bills will likely continue to offer some support to European consumers, but won’t be enough to offset the squeeze on real incomes amid rising inflation. Excess household savings have been exhausted, forcing households to pull back. Retail sales have started to show signs of softening in recent months. Consumer confidence has tanked to near an all-time low.

- Economics cannot be separated from politics, especially in France. President Macron failed to gain an absolute majority in the final round of the legislative elections, which could lead to policy paralysis. While it is still possible to strike case-by-case agreements on legislation, the government’s ability to pass unpopular reforms is at risk, including president’s ability to push for greater European integration.

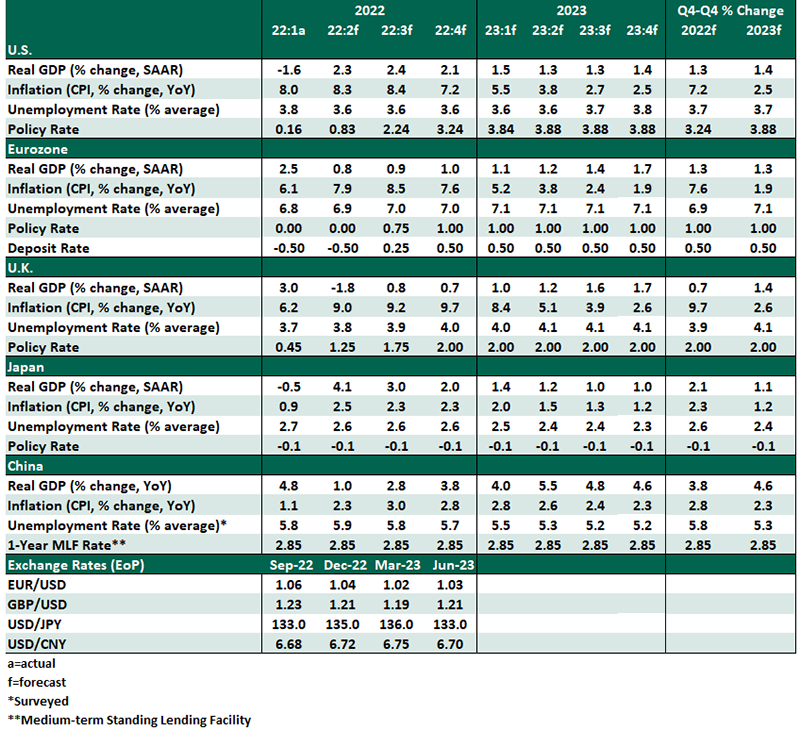

Global Economic Forecast – June 2022

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.