'%3e%3cpath%20d='M14.5584%2010.5857L23.6652%200H21.5072L13.5999%209.19156L7.2843%200H0L9.55034%2013.8992L0%2025H2.1582L10.5087%2015.2935L17.1783%2025H24.4626L14.5582%2010.5857H14.5588H14.5584ZM11.6025%2014.0215L10.6348%2012.6375L2.9357%201.62451H6.25036L12.4638%2010.5123L13.4315%2011.8963L21.5082%2023.4491H18.1935L11.6027%2014.0219V14.0213L11.6025%2014.0215Z'%20fill='%23808182'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_20_84'%3e%3crect%20width='24.4624'%20height='25'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

%20is%20a%20leading%20provider%20of%20wealth%20management,%20asset%20servicing,%20asset%20management%20and%20banking%20to%20corporations,%20institutions,%20affluent%20families%20and%20individuals.%20Founded%20in%20Chicago%20in%201889,%20Northern%20Trust%20has%20offices%20in%20the%20United%20States%20in%2019%20states%20and%20Washington,%20D.C.,%20and%2020%20international%20locations%20in%20Canada,%20Europe,%20the%20Middle%20East%20and%20the%20Asia-Pacific%20region.%20%3c/desc%3e%3cpath%20fill='%233d4042'%20d='M21,21H17V14.25C17,13.19%2015.81,12.31%2014.75,12.31C13.69,12.31%2013,13.19%2013,14.25V21H9V9H13V11C13.66,9.93%2015.36,9.24%2016.5,9.24C19,9.24%2021,11.28%2021,13.75V21M7,21H3V9H7V21M5,3A2,2%200%200,1%207,5A2,2%200%200,1%205,7A2,2%200%200,1%203,5A2,2%200%200,1%205,3Z'%3e%3c/path%3e%3c/svg%3e)

%20-%20https://sketch.com%20--%3e%3ctitle%3eEmail%3c/title%3e%3cdesc%3eShare%20article%20via%20email%3c/desc%3e%3cg%20id='Article'%20stroke='none'%20stroke-width='1'%20fill='none'%20fill-rule='evenodd'%3e%3cg%20id='article-desktop'%20transform='translate(-291.000000,%20-905.000000)'%20fill='%233d4042'%20fill-rule='nonzero'%3e%3cg%20id='Group-3'%20transform='translate(280.000000,%20700.000000)'%3e%3cpath%20d='M12.5859376,205%20L25.5,216.098563%20L38.4140625,205%20L12.5859376,205%20Z%20M11,206.352162%20L11,221.582916%20L19.5446429,213.697123%20L11,206.352162%20Z%20M40,206.352162%20L31.4553572,213.697123%20L40,221.582916%20L40,206.352162%20L40,206.352162%20Z%20M21.1197917,215.049268%20L12.5212054,223%20L38.4787946,223%20L29.8802084,215.049268%20L26.1688988,218.240388%20C25.7827601,218.567837%2025.21724,218.567837%2024.8311012,218.240388%20L21.1197917,215.049268%20L21.1197917,215.049268%20Z'%20id='Shape'%3e%3c/path%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

'%20fill='%233d4042'%20fill-rule='nonzero'%3e%3cpath%20d='M317.048444,961%20C318.677807,961.001791%20319.998224,962.333083%20320,963.975866%20L320,963.975866%20L320,972.789759%20C320,973.478748%20319.446027,974.037283%20318.762667,974.037283%20L318.762667,974.037283%20L313.420222,974.037283%20L313.420222,980.619276%20C313.466211,981.335082%20312.928257,981.953082%20312.218333,982%20L312.218333,982%20L298.781667,982%20C298.071743,981.953082%20297.533789,981.335082%20297.579778,980.619276%20L297.579778,980.619276%20L297.579778,974.037283%20L292.237333,974.037283%20C291.553973,974.037283%20291,973.478748%20291,972.789759%20L291,972.789759%20L291,963.975866%20C291.001776,962.333083%20292.322193,961.001791%20293.951556,961%20L293.951556,961%20Z%20M311.486889,970.525371%20L299.513111,970.525371%20L299.513111,980.050743%20L311.486889,980.050743%20L311.486889,970.525371%20Z%20M314.395276,962.742345%20C313.970645,962.65481%20313.549254,962.905694%20313.420222,963.322865%20C313.394809,963.404999%20313.380715,963.490265%20313.378333,963.576269%20C313.380722,963.661209%20313.394821,963.7454%20313.420222,963.826423%20C313.529012,964.18316%20313.855609,964.426832%20314.225778,964.427444%20C314.659193,964.427644%20315.022348,964.096906%20315.066078,963.66215%20C315.109809,963.227395%20314.819907,962.829881%20314.395276,962.742345%20Z%20M317.130097,962.784571%20C316.813535,962.651298%20316.448506,962.723595%20316.20547,962.967701%20C315.962434,963.211807%20315.889338,963.579564%20316.020315,963.899239%20C316.151293,964.218915%20316.460504,964.427444%20316.803556,964.427444%20L316.803556,964.427444%20C317.274992,964.425655%20317.651006,964.045094%20317.651006,963.576269%20C317.652304,963.230394%20317.44666,962.917844%20317.130097,962.784571%20Z%20M311.783656,955%20C312.500482,955.040538%20313.043667,955.574507%20312.997231,956.192982%20L312.997231,956.192982%20L312.997231,959%20L297.002769,959%20L297.002769,956.192982%20C296.956333,955.574507%20297.499518,955.040538%20298.216344,955%20L298.216344,955%20Z'%20id='icon-print'%3e%3c/path%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

Tax News You Can Use | For Professional Advisors

Jane G. Ditelberg

Director of Tax Planning, The Northern Trust Institute

February 24, 2025

One of the tax benefits of being married is the availability of the “split gift election.” Making the election allows couples who are citizens or residents of the United States to treat gifts to third parties by either of them as having been made one-half by each of them. This can be helpful for spouses who are both making gifts, but it also can allow a wealthier spouse making gifts to use the less-wealthy spouse’s exclusions and exemption. If taxpayers make the election for a tax year, it applies to all eligible gifts made by either spouse during that year. A gift to the other spouse, or a trust in which the other spouse has a present interest, is generally not eligible for split gift treatment. However, with respect to transfers to trusts benefiting the consenting spouse and third parties, the portion transferred to the third parties cannot be split unless such interest is ascertainable at the time of the transfer and severable from the interest transferred to the consenting spouse.

How Does a Taxpayer Make the Split Gift Election?

The section of the Internal Revenue Code governing this election, section 2503, has not changed. However, for gifts made in 2024 and reportable on a return due on April 15, 2025 (or October 15, 2025 if extended), the IRS has changed the forms and the process. Taxpayers, tax preparers and those who advise them should familiarize themselves with the new requirements for making an effective election. The new form is available here (2024 Form 709) and the instructions are here (Instructions for Form 709 (2024) | Internal Revenue Service).

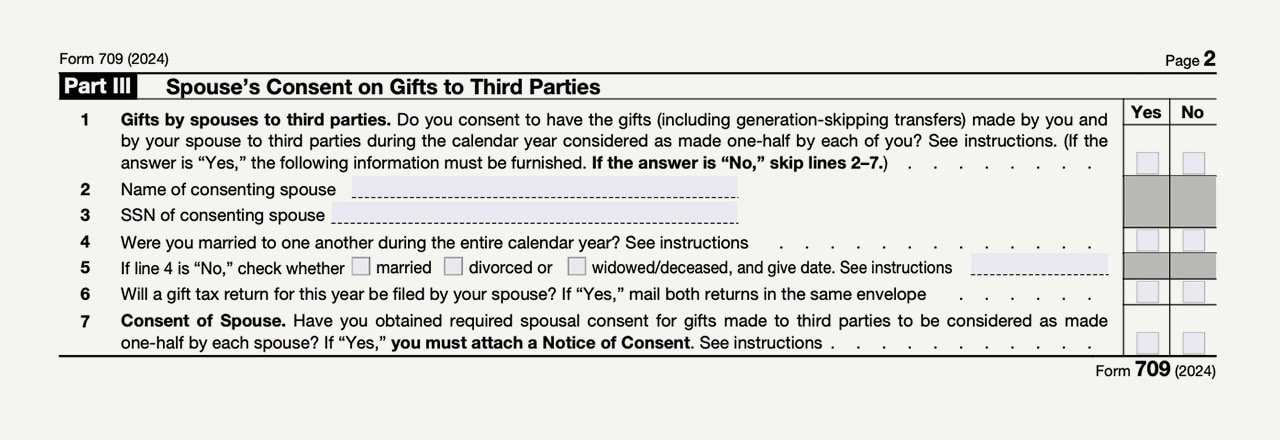

Under the new rules, the spouse who made the gift (the “donor spouse”) reports the gift on their own tax return and completes Part III, which the IRS has added to the form for 2024 returns.

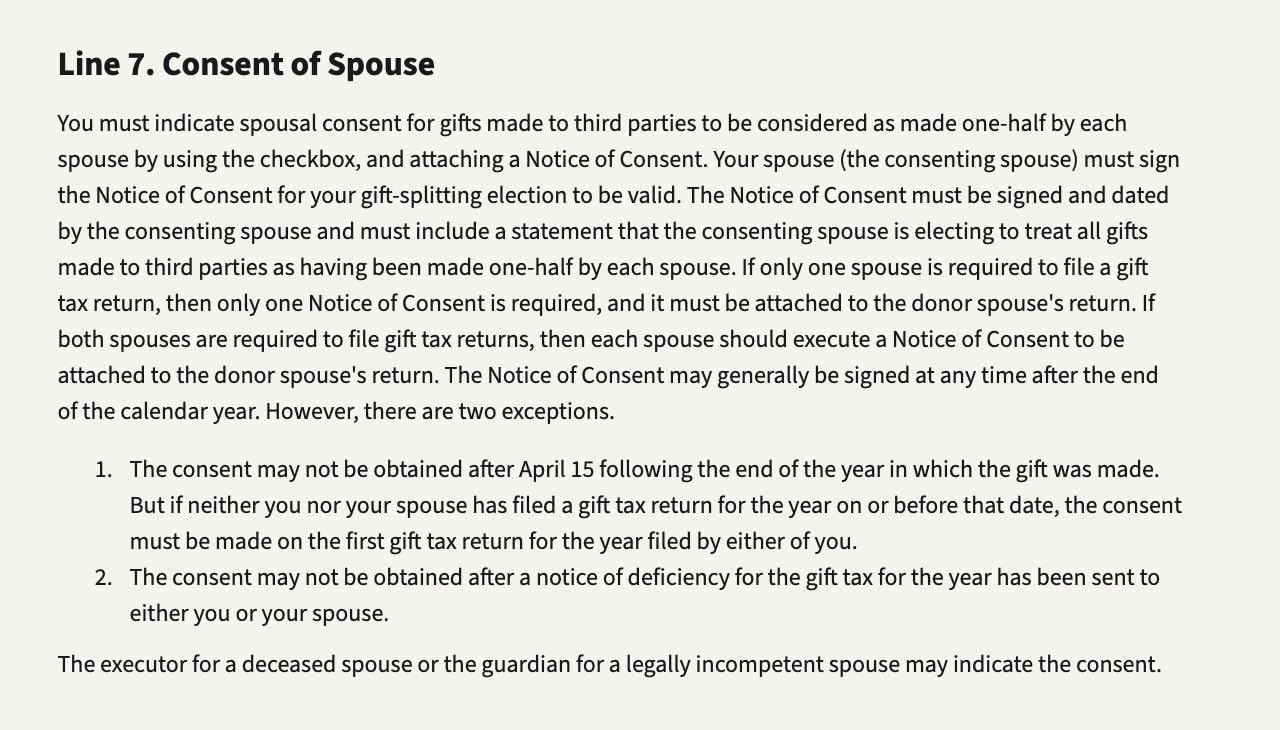

Rather than have the other spouse (the “consenting spouse”) consent by signing a line on the donor spouse’s return, the consenting spouse must instead file a separate notice of consent. According to the instructions for form 709, the notice of consent must be signed and dated by the consenting spouse and must include a statement that the consenting spouse is electing to treat all gifts made to third parties as having been made one-half by each spouse.

In addition, if both spouses are filing returns, the instructions indicate that they should transmit the returns together in the same envelope.

How to Report Gifts Subject to the Split Gift Election

Taxpayers report gifts subject only to gift tax on Part 1 of Schedule A and gifts subject to both generation-skipping transfer tax (GST) and gift tax on Parts 2 and 3 of Schedule A. In each case, there are separate sections for gifts the donor spouse made and the share of gifts made by the consenting spouse that are subject to the split gift election. The split gift election treats each gift as made one-half by each spouse for GST purposes as well as gift tax purposes, and taxpayers can claim the GST annual exclusion and allocate GST exemption on Schedule D. The form has separate sections for the donor’s own reported gifts and the donor’s share of the consenting spouse’s gifts (if the consenting spouse made gifts of their own to third parties, which will also be subject to the split gift election).

When is the Election Made?

Taxpayers must make the election on the first gift tax return for the year filed by either spouse. This can be a trap for the unwary. Couples need to make the decision whether to elect split gift treatment as early as possible in the filing process. Early action is key to avoiding any missed opportunity to make the election. This is particularly important when one spouse makes gifts to a trust that are not eligible for split gift treatment. Gifts ineligible for split gift treatment include transfers to trusts that benefit the donor’s spouse and other beneficiaries, such as an irrevocable life insurance trust or a spousal lifetime access trust, where the portion transferred to the third parties is not ascertainable and cannot be severed from the interest transferred to the consenting spouse at the time of the transfer.

Must Both Spouses File a Return?

Typically, both spouses need to file a gift tax return in a year when they elect to split gifts. There are two exceptions to this rule. The first is when only one spouse has made gifts during the year, all those gifts qualify as present interests (so they are qualified for the gift tax annual exclusion) and no gift exceeds double the annual exclusion amount ($36,000 for 2024, $38,000 for 2025). In this case, the donor spouse files a return with the consenting spouse’s consent to the split gift election contained in a Notice of Consent attached to the return.

The second exception is where one spouse made no gifts in excess of double the annual exclusion (and at least one in excess of the annual exclusion amount of $18,000 for 2024, $19,000 for 2025), and the other spouse made no gifts to the same donees and only made gifts of not more than the annual exclusion amount. In this situation, only the donor spouse needs to file a gift tax return. As before, the return will require the consenting spouse’s consent to the split gift election to be contained in a Notice of Consent attached to the return.

Examples:

- In 2024, Ashton made gifts of $30,000 to each of his six siblings. Ashton’s spouse, Blair, made one gift of $10,000 to her mother. If Ashton and Blair file a split gift election, each will be treated as making six gifts of $15,000 to each of Ashton’s siblings and one gift of $5,000 to Blair’s mother. On these facts, Ashton must file a form 709 gift tax return to make the split gift election and include with it Blair’s signed consent. Blair does not need to file a gift tax return. All the gifts, if made outright, qualify for the gift tax annual exclusion.

- In 2025, Blair makes a gift of $1 million to a spousal lifetime access trust (SLAT) for Ashton, which includes a right of withdrawal that qualifies the first $5,000 of contributions as a present interest gift to Ashton. Ashton makes one gift of $10,000 to a friend. In this case, Blair cannot elect split gift treatment for her gift because Ashton is the sole beneficiary, and spouses cannot split gifts made to themselves. Ashton does not need to file a return. Blair files a return reporting a $5,000 gift to Ashton, and a $995,000 gift to the trust.

- In 2025, Ashton makes gifts of $50,000 to each of his six siblings. Blair makes gifts of $100,000 to her mother and $50,000 to her niece. Aston and Blair can make a split gift election that would treat each of those eight gifts as made one-half by Ashton and one-half by Blair. To do this, they would each file a gift tax return and attach the other spouse’s consent. By doing this, Ashton would get to use Blair’s annual exclusions for part of each of his six gifts, and Blair would get to use Ashton’s annual exclusions for her two gifts. Without a split gift election, Ashton would have made taxable gifts for the year of $186,000, and Blair would have made $112,000. With the split gift election, which doubles the available annual exclusion, Ashton needs to report only $72,000 in taxable gifts, and Blair reports $74,000.

Key Takeaways:

- The IRS has issued a new form 709 to use for 2024 gifts that changes the steps for a married couple to make a “split gift” election.

- The donor spouse must file a return and attach the consenting spouse’s written consent to make the split gift election (previously, the consenting spouse signed the donor spouse’s return to make the election).

- The instructions direct taxpayers to file both returns together in the same envelope.

- The election must be made on the first return filed for either party for the tax year in question.

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)